Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A revenue recognition method in which revenue is recorded before the delivery of goods

A bill-and-hold arrangement is a revenue recognition method in which revenue is recorded before the delivery of goods. It involves the recognition of revenue prior to the shipment of goods to the buyer. As such, a bill-and-hold arrangement is considered a controversial revenue recognition method due to the ease of manipulating earnings.

A bill-and-hold arrangement is considered an aggressive method of revenue recognition, and its use is generally frowned upon by the Securities and Exchange Commission (SEC).

According to the Journal of Accountancy, bill-and-hold arrangements are often associated with financial fraud.

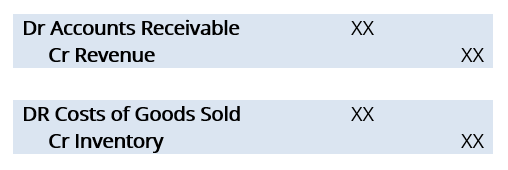

Consider the journal entries of a hypothetical bill and hold transaction:

The issue lies in the first set of journal entries, which debit accounts receivable and credit revenue. These two journal entries convey that the seller recognized revenue without receiving payment (i.e., cash).

As such, there is a motive for the seller to collude with the buyer by advising the buyer to purchase under a bill-and-hold arrangement and then cancel the order once payment is due.

In effect, this artificially inflates earnings for that reporting period but adversely affects earnings in later periods, a phenomenon called channel stuffing. Due to the ease of conducting financial fraud with a bill-and-hold arrangement, the SEC laid out the following criteria to recognize a bill-and-hold arrangement:

1. Ownership risks should be passed on to the buyer

2. The buyer must have a commitment (preferably in writing) to buy the goods.

3. The buyer must request the bill-and-hold arrangement and have a substantive reason to do so

4. There must be a fixed and reasonable schedule for the delivery of goods to the buyer.

5. There must be no more obligations on the seller’s end.

6. The goods must be segregated from the seller’s inventory and not be used to fill other orders.

7. The goods must be ready to ship.

The SEC has outlined that the above is not intended to be used as a checklist – in some circumstances, an arrangement may meet all the criteria above and not be approved for revenue recognition.

1. The expected payment date and the extent to which the seller is modifying its normal sales terms for the bill-and-hold arrangement

2. The seller’s history with bill-and-hold arrangements

3. The extent of losses faced by the buyer if the market value of the goods decline

4. The extent to which holding risks faced by the seller can be insured

5. Whether the goods can create a contingent sale that the buyer could reject

According to the IFRS 15 (Revenue from Contracts with Customers), the following conditions must be met for a seller to recognize revenue under a bill-and-hold arrangement:

1. The reason should be substantive.

2. The goods must be separately identified as belonging to the buyer

3. The goods must be ready for delivery to the buyer

4. The seller should not transfer the goods to another customer or for other uses.

Consider the following background information:

Question: Under the guidance of IFRS 15, how many widgets should Company A recognize as revenue?

Answer: Company A should recognize the 100 widgets as revenue.

The reason for the bill and hold arrangement is substantive, as Retailer A does not have any shelf space for the widgets.

A pervasive fraud associated with bill-and-hold arrangements involved Sunbeam Corporation in the late 1990s. At that time, CEO Al Dunlap (nicknamed “Chainsaw Al”), who was known as a turnaround management specialist, encouraged customers to place large orders at significant discounts.

It resulted in customers placing a significant number of orders for barbeques during the middle of winter – months before the goods were required. To sweeten the deal, Sunbeam agreed to hold the goods at a warehouse until they were ready to be requested and shelved by the retailers.

As a result, Sunbeam booked significant sales, boosting the company’s share price. When questioned by auditors, Sunbeam eventually reversed a significant portion of the revenue recognized from such bill-and-hold arrangements, indicating that they were recognizing revenue too quickly and attempting to shift sales earlier onto their books.

In 2001, Sunbeam filed for bankruptcy and was found to have committed massive accounting fraud.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

To keep advancing your career, the additional resources below will be useful: