Step Costs

Costs that do not change in direct proportion to increasing levels of activity

What are Step Costs?

Step costs, also called stair-step costs, are costs that do not change in direct proportion to increasing levels of activity. In other words, step costs are constant at a certain activity level but increase or decrease when an activity threshold is met.

Understanding Step Costs

Step costs are extremely important to consider when a company is about to reach a new activity level. If neglected, they can cause a business to miss out on profits.

John operates a company that produces pens. A machine costing $15,000 is capable of producing up to 1,000 pens. Assume that there are no additional costs related to producing pens (no raw materials, labor, etc.). As such, the cost of machinery is an example of a step cost. The information is illustrated below:

As shown in the illustration, the cost of machinery closely resembles steps. At a production of 500 or 750 pens, only one machine is required. The total cost is, therefore, $15,000. However, at the production of 1,500, the company must purchase an additional machine to expand its production capacity. At a production of 1,500 pens, the total cost is $30,000 ($15,000 x 2 machines). Therefore, it is an example of a step cost: costs that are constant at a certain level of activity and rise or decrease when a certain activity threshold is met.

Importance of Step Costs

Step costs are extremely important to consider when a company is about to reach a new activity level. If neglected, they can cause a business to lose unnecessary profits.

Continuing with the example above. Assume that John initially forecasted that the demand for pens would be 1,050 next year. Additionally, assume that each pen can be sold for $20.

To an individual who does not understand step costs, they may recommend purchasing two machines to meet the demand for 1,050 pens. The revenues generated from 1,050 pens are $21,000 (1,050 x $20). However, total costs (two machines) are $30,000. The purchase of the second machine that would only generate revenue for the sale of 50 additional pens would make the company much less profitable.

To an individual who understands step costs, they would recommend purchasing one machine and producing 1,000 pens and not 1,050. The revenues generated from 1,000 pens are $20,000 (1,000 x $20) and the total costs (one machine) are $15,000. The company would be generating $5,000 in profits at the given production level.

As shown above, investing in an additional machine would cause the company to lose profits! Therefore, it is key to consider whether incurring a step cost would be accretive to profits or not. In the example above, an additional 50 pens (revenues of $100) would be generated through a second machine costing $15,000. In such a scenario, it would not be worthwhile for the company to incur the additional cost to produce an additional 50 pens.

Example

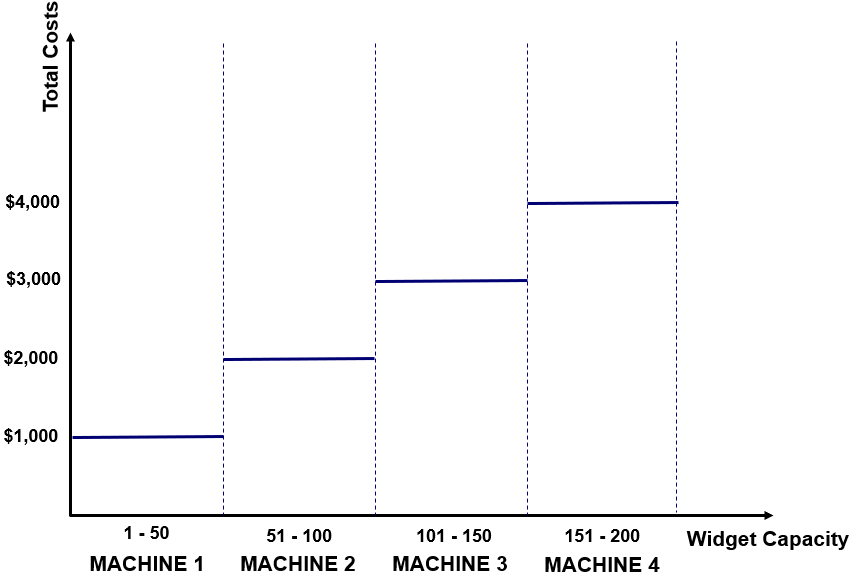

Consider a company with a cost structure in the production of widgets as follows:

Assuming that the sale price of widgets is $30 and the company currently utilizes three machines and sells 125 widgets. Would you recommend the company to continue utilizing three machines or to cut down to two and only sell 100 widgets (the production capacity for two machines)?

Three machines with sales of 125 widgets

The total costs for the three machines are $3,000. The sales generated from 125 widgets are $3,750 (125 x $30). Therefore, the profit is $750.

Two machines with sales of 100 widgets

The total costs for the two machines are $2,000. The sales generated from 100 widgets are $3,000 (100 x $30). Therefore, the profit is $1,000.

Therefore, the company should only operate two machines and produce 100 widgets.

Step Costs in the News

Step costs are common – the cost of a new production facility, the cost of a new machine, supervision costs, marketing costs, etc., are all step costs.

For example, on July 17, 2019, FortisBC announced the completion of a $400-million expansion project that increased the company’s capacity from 35,000 a ton to 250,000 a ton. As such, the facility expansion project by FortisBC is a step cost.

Related Readings

CFI offers the Financial Modeling & Valuation Analyst (FMVA)® certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following CFI resources will be helpful:

Analyst Certification FMVA® Program

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

Additional Questions & Answers

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

- What is Financial Modeling?

- How Do You Build a DCF Model?

- What is Sensitivity Analysis?

- How Do You Value a Business?

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.