Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

The increment in the value of a bond after purchasing it at a discount

Accretion is a finance term that refers to the increment in the value of a bond after purchasing it at a discount and holding it until the maturity date. A bond is said to be purchased at a discount price when the purchase price falls below its par value. As the redemption date approaches, the value of the bond will grow until it converges with its par or face value at maturity. The acceleration in the value of the bond over time is known as the accretion discount.

A bond that is purchased at a higher price than its face value is said to be purchased at a premium. As the bond nears maturity, it declines in value until it reaches its par value on the maturity date. The decline in value of the bond over time is known as the amortization of premiums.

In acquisitions, accretion refers to the growth in earnings and assets after a particular transaction, such as a merger or acquisition. The transaction is considered earnings accretive when the acquirer’s price-earnings ratio is greater than the P/E of the target company. The acquirer is interested in acquiring a target company with a low price-earnings ratio as a way of boosting the post-acquisition earnings per share (EPS) of the combined company and increasing the price of its shares.

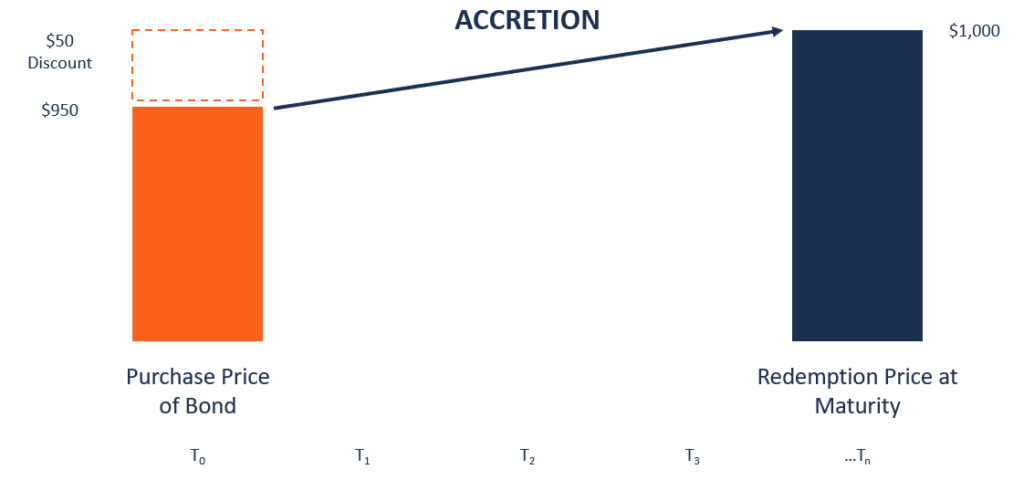

Bond accretion is the growth in the value of the bond as time lapses. As it approaches the maturity date, the value of the bond increases until it converges with its par value, which is the amount paid to the bondholder. For example, assume that the par value of a bond is $1,000, but it is offered at a discounted price of $950. It means that the present value of the bond is $950, and the discount is $50 ($1,000 – $950). The value of the bond will increase until it reaches a face value of $1,000.

There are two main methods of accounting for bond accretion, i.e., the straight-line method and the constant yield method.

When using the straight-line method, the increase in the value of the bond is spread evenly throughout the term of the bond. For example, if the term of the bond is 5 years and the company reports its financials every quarter, it means that there are 20 financial periods up to maturity.

The discount of $500 is divided across the 20 periods, which equals $25 per quarter. It means that there will be an accretion of $25 in each period until maturity. It will raise the bond liability balance by $25 in each period until the redemption date.

When using the constant yield method, the increase in the value of the bond is heaviest closest to the maturity date. Unlike the straight-line method, the increment is not even and some periods tend to show bigger gains than other periods. The gains are concentrated in the last phase of the bond’s life.

When using the constant yield method, the first step is determining the Yield to Maturity (YTM). YTM is what the bond will earn until the maturity date. When calculating the yield using a spreadsheet or calculator, you will need the par value of the bond, price, years to maturity, and the bond interest rate as inputs.

One of the objectives of acquiring another business and merging into the current business is to increase synergies. The new combined business enjoys greater value than the sum of the two separate entities. The combined company enjoys reduced costs, greater economies of scale, and higher earnings.

The acquirer generates an acquisition accretion by adding the EBITDA/Earnings ratio of the smaller business into the larger business’ EBITDA/Earnings ratio. Acquisition accretion is a good thing for companies, as it increases the shareholders’ value.

Assume that Company ABC wants to acquire Company XYZ as a way of increasing its EPS. Company ABC reported $200,000 in net income in the past year, and it owns 1,000,000 in outstanding shares. On the other hand, Company XYZ reported a net income of $100,000 in the past year, and 200,000 new shares were sold to raise cash to purchase the number of outstanding shares. We can use the given information to determine the acquisition accretion of the combined company.

EPS of the acquirer:

EPS = 200,000/1,000,000 = $0.20

EPS of the combined company:

= (200,000+100,000)/(1,000,000+200,000) = 300,000/1,200,000 = $0.25

The EPS of the combined company ($0.25) is $0.05 higher than the original EPS of ABC company ($0.20). It means that the acquisition accretion for the transaction is $0.05.

CFI offers the Capital Markets & Securities Analyst (CMSA®) certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.