Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A practice where the issuing entity and the underwriter negotiate the terms of a planned sale

A negotiated sale is a sale of bonds that is an alternative to the competitive bidding process in which multiple interested parties place their bid terms with the aim of beating other bidders and emerging the winner. It is sometimes preferred over competitive bidding due to its speed, flexibility, efficiency, and level of confidentiality between the issuer and the underwriter.

A negotiated sale may be initiated from the underwriters’ side when they present unsolicited offers for consideration by the issuer. Alternatively, the sale process may be initiated by investment bankers who have a close relationship with buyers that may be a perfect match for the issuing entity. A negotiated sale may have several interested buyers, but the most common feature is having one buyer with a high probability of closing the deal.

The primary points of negotiation in a negotiated sale include the purchase price, interest rate, and call features. The issuer is interested in getting the highest purchase price for the bonds, and the two parties must achieve a common understanding regarding the three main points.

The issuing entity must select an underwriter to purchase the bonds before the sale date. In turn, the underwriter sells the bonds to its investor customers based on their demands, as well as on the interests of the issuer. The underwriter may do a pre-sale to ascertain customers’ interest in the sale before offering a final price.

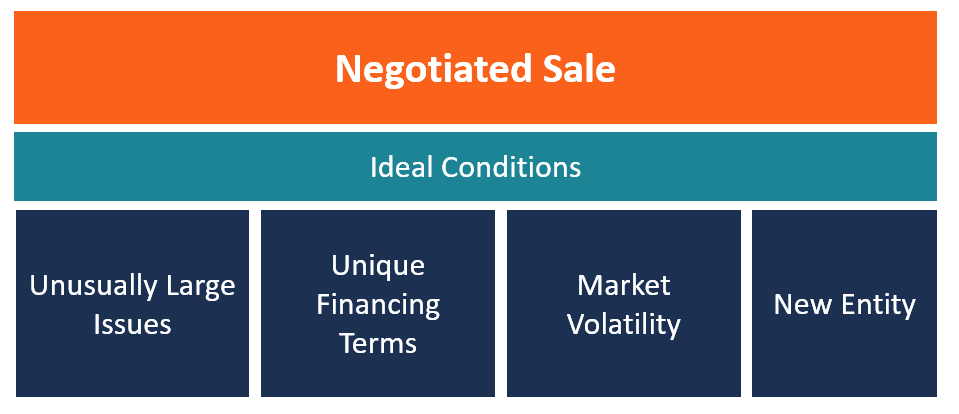

For unusually large issues, some underwriters may choose to stay away because the large number of issues may overwhelm them. Such large issues require large amounts of capital to push them in the market, and an underwriter may be incapable of raising such large amounts of money.

Some underwriters may form bidding syndicates by pooling resources to eliminate competition. In such circumstances, an issuer may prefer working with a team of underwriters who have pooled their resources and guarantee the success of the bond issue.

An issuer may prefer a negotiated sale over competitive bidding if the bond issue is targeting specific classes of underwriters. For example, if the issuer has designed the bond issue to appeal to women-owned underwriting firms, the terms of the issue may limit eligibility for the underwriting service to a specific category of underwriters who meet the requirements.

The issuer’s goal is to get an underwriter who can sell the bonds competitively, but at a reduced cost, and getting an underwriter who meets the set requirements can help the issuer achieve these targets.

In a market where the interest rates for bonds change within a short timeframe, most underwriters may bid conservatively to avert incurring any losses. The issuer may decide to enter into a negotiated sale with an interested party and time the sale date in accordance with market conditions. The issuer may also negotiate the terms of the bond issue with an underwriter who has recorded success with other bond issues in volatile markets.

A new entity will often face difficulties attracting underwriters to show interest on its bond issue. New entities may not have the credit history that underwriters require, and this may affect the bond issue. However, a negotiated sale may include a pre-sale that can serve to stimulate investors’ interest before the actual bond issue is floated on the market.

One of the advantages of negotiated sales is that the issuer may get an offer that meets their price expectations and terms, without getting involved in the laborious process of competitive bidding. Some issuers go into competitive bidding to get the best offer from a list of interested purchasers. However, if the issuer receives unsolicited offers from logical buyers, it simplifies the process, and the two parties can close the transaction within a short period.

Negotiated sales also allow trust and a strong business relationship with the potential underwriter. They allow the underwriter to find the best possible price for the bond that is convenient to both the issuer and the investors.

When the issuing entity negotiates a transaction with one single potential buyer only, it may get an offer that falls below the fair market value. The lack of other competitors may limit the issuer’s potential to get the best possible terms.

Another limitation of a negotiated sale is that the issuer will have less negotiating power after closing the transaction with a single seller. The issuer may be comfortable with the initial offer presented by the buyer, but the offer may be watered down during the negotiations. The buyer knows that the issuer has no alternatives and may be tempted to offer a lower price than what they had presented earlier to the issuing entity.

Apart from a negotiated sale, underwriters may also use the competitive bidding process to purchase bonds from an issuing entity. A competitive sale starts with the bonds being advertised for sale to the public by a notice of sale that indicates the terms of the sale and bond issue.

Interested bidders like brokers and investment banks then show their interest in the bond by sending their bid quotes to the issuer, indicating their purchase price, interest rate, and other terms of the issue. The bid must be submitted before the time and date provided by the issuer. After the close of the bidding period, the issuer awards the bonds to the bidder with the best price and lowest interest cost.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: