Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

A measure of financial soundness for banks

Bank rating is a measure of financial soundness for banks. Just like credit agencies such as Standard & Poor’s (S&P), Moody’s, and Fitch that give credit ratings to individual consumers and corporations, the Federal Deposit Insurance Corporation (FDIC) assigns credit ratings to banks and other financial institutions.

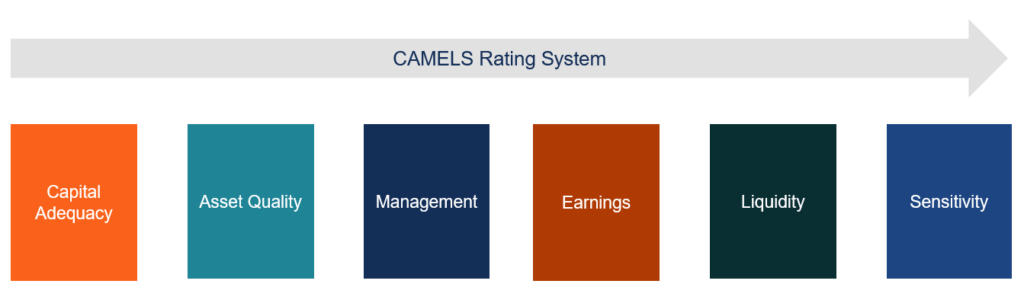

Bank ratings are generally between 1 and 5 – with 1 being the best and 5 being the worst. Bank ratings are computed using the CAMELS rating system, a globally recognized rating system that measures the financial soundness of financial institutions based on six factors.

Capital adequacy measures cash reserves of banks and financial institutions relative to the minimum capital requirements set by regulatory authorities.

To get a high rating on capital adequacy, financial institutions must be well within the minimum capital requirements set by the regulators. Institutions must also meet all other requirements set by regulatory agencies, including guidelines and regulatory policies related to interest and dividends.

Asset quality measures the quality of a bank’s loans and other assets based on both credit and market risk. It involves identifying and rating potential risk factors relative to the capital earnings generated. Credit risk is measured by assessing the quality of loans and credit worthiness of borrowers.

Investments in government bonds and loans to corporations with high credit ratings are considered safe, while corporate loans to companies with low credit ratings are considered low-quality loans. The Federal Deposit Insurance Corporation (FDIC) emphasizes measuring the quality of loans as these provide the main source of income for banks.

The asset quality rating also measures market risk by evaluating how a bank’s market value of investments will change under different economic environments. It involves stress testing the market value of securities to changes in key economic indicators, such as interest rates and inflation.

Management measures the management’s ability to run the day-to-day operations, execute key functions, and adapt to changing market conditions to manage investment risk factors. It also involves an internal review of management policies to ensure that they comply with regulatory guidelines.

Earnings measures a bank’s ability to consistently generate stable earnings on a risk-adjusted basis. A bank generates earnings by capturing the difference in the spread between the rate at which it lends and the rate at which it pays on deposits.

The ability of a bank to consistently grow its earnings and deposits is a key determinant of its future viability and prospects. Regulators measure the quality of earnings by assessing the bank’s growth in deposits, balance sheet stability, quality of loans, and interest rate spread.

Liquidity measures a bank’s ability to meet its short-term obligations, including withdrawal of deposits. It involves identifying assets that can be easily converted into cash.

Regulators assess liquidity by evaluating the amount and quality of liquid assets relative to the short-term obligations of the institution. The liquidity coverage ratio is used to assess whether the bank holds enough liquid assets. Generally, only high-quality liquid assets are considered for this analysis.

Sensitivity measures how sensitive a bank’s earnings are to particular risk factors. Regulators use the sensitivity information to understand how the exposure of the institution is distributed among specific industries. The information is then used to assess how lending capital to specific industries can impact the bank’s income and credit risk.

The sensitivity rating also assesses income sensitivity based on exposure to volatility in foreign exchange, commodities, equities, and derivative markets.

The FDIC assigns a bank rating between 1 and 5 based on the CAMELS assessment framework. A rating of 1 or 2 is assigned to financial institutions that are strong on all six aspects of the CAMELS framework. The institutions are generally considered to be in a sound financial position.

A rating of 3 is considered satisfactory and indicates that no major issues are facing the bank in question. Banks that are assigned ratings of 4 or 5 are generally considered to be in danger. Such banks need to take immediate action and require careful monitoring.

Finally, financial institutions that are assigned a rating of 5 demonstrate a high probability of declaring bankruptcy in the next 12-24 months.

CFI is the official provider of the global Financial Modeling & Valuation Analyst (FMVA)™ certification program, designed to help anyone become a world-class financial analyst. To keep learning and advancing your career, the additional CFI resources below will be useful: