Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

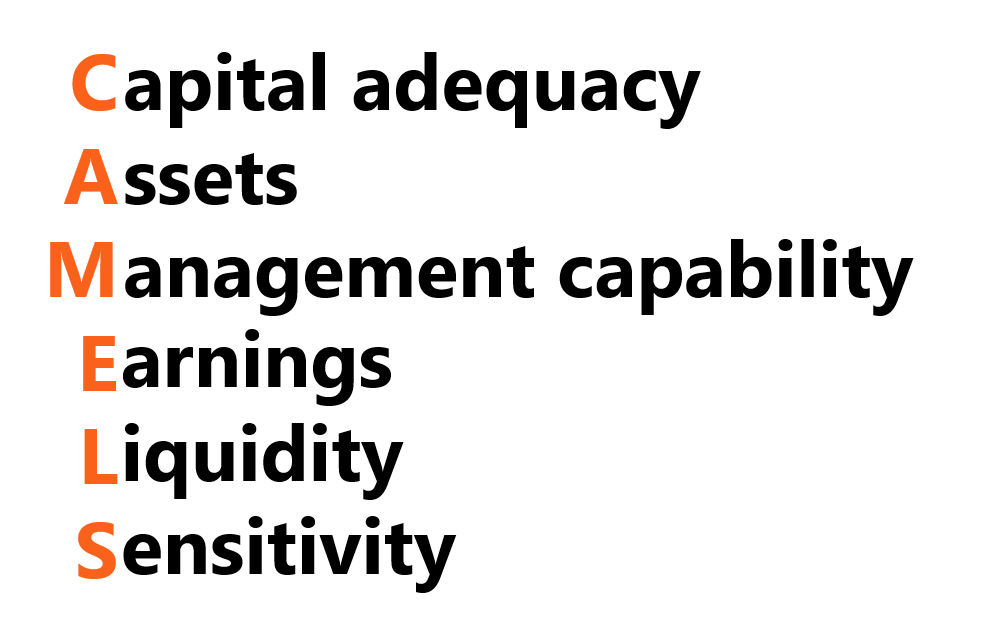

A rating system to assess a bank's overall condition

The CAMELS Rating System was developed in the United States as a supervisory rating system to assess a bank’s overall condition. CAMELS is an acronym that represents the six factors that are considered for the rating. Unlike other regulatory ratios or ratings, the CAMELS rating is not released to the public. It is only used by top management to understand and regulate possible risks.

Supervisory authorities use scores on a scale of 1 to 5 to rate each bank. The strength of the CAMEL lies in its ability to identify financial institutions that will survive and those that will fail. The concept was initially adopted in 1979 by the Federal Financial Institutions Examination Council (FFIEC) under the name Uniform Financial Institutions Rating System (UFIRS). CAMELS was later modified to add a sixth component – sensitivity – to the acronym.

The components of CAMELS are:

Capital adequacy assesses an institution’s compliance with regulations on the minimum capital reserve amount. Regulators establish the rating by assessing the financial institution’s capital position currently and over several years.

Future capital position is predicted based on the institution’s plans for the future, such as whether they are planning to give out dividends or acquire another company. The CAMELS examiner would also look at trend analysis, the composition of capital, and liquidity of the capital.

This category assesses the quality of a bank’s assets. Asset quality is important, as the value of assets can decrease rapidly if they are high risk. For example, loans are a type of asset that can become impaired if money is lent to a high-risk individual.

The examiner looks at the bank’s investment policies and loan practices, along with credit risks such as interest rate risk and liquidity risk. The quality and trends of major assets are considered. If a financial institution has a trend of major assets losing value due to credit risk, then they would receive a lower rating.

Management capability measures the ability of an institution’s management team to identify and then react to financial stress. The category depends on the quality of a bank’s business strategy, financial performance, and internal controls. In the business strategy and financial performance area, the CAMELS examiner looks at the institution’s plans for the next few years. It includes the capital accumulation rate, growth rate, and identification of the major risks.

For internal controls, the exam tests the institution’s ability to track and identify potential risks. Areas within internal controls include information systems, audit programs, and recordkeeping. Information systems ensure the integrity of computer systems to protect customer’s personal information. Audit programs check if the company’s policies are being followed. Lastly, record keeping should follow sound accounting principles and include documentation for ease of audits.

Earnings help to evaluate an institution’s long term viability. A bank needs an appropriate return to be able to grow its operations and maintain its competitiveness. The examiner specifically looks at the stability of earnings, return on assets (ROA), net interest margin (NIM), and future earning prospects under harsh economic conditions. While assessing earnings, the core earnings are the most important. The core earnings are the long term and stable earnings of an institution that is affected by the expense of one-time items.

For banks, liquidity is especially important, as the lack of liquid capital can lead to a bank run. This category of CAMELS examines the interest rate risk and liquidity risk. Interest rates affect the earnings from a bank’s capital markets business segment. If the exposure to interest rate risk is large, then the institution’s investment and loan portfolio value will be volatile. Liquidity risk is defined as the risk of not being able to meet present or future cash flow needs without affecting day-to-day operations.

Sensitivity is the last category and measures an institution’s sensitivity to market risks. For example, assessment can be made on energy sector lending, medical lending, and agricultural lending. Sensitivity reflects the degree to which earnings are affected by interest rates, exchange rates, and commodity prices, all of which can be expressed by Beta.

For each category, a score is assigned from 1 to 5. One is the best score and indicates strong performance and risk management practices within the institution. On the other hand, five is the poorest rating. It indicates a high probability of bank failure and the need for immediate action to rectify the situation. If an institution’s current financial condition falls between 1 and 5, it is called a composite rating.

A higher rating will impede a bank’s ability to expand through investment, mergers, or adding more branches. Also, the institution with a poor rating will be required to pay more in insurance premiums.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s article on the CAMELS rating system. To keep learning and advancing your career, these additional CFI resources will be helpful: