Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The entire principal is due at the end of the loan term

A bullet loan is a type of loan in which the principal that is borrowed is paid back at the end of the loan term. In some cases, the interest expense is added to the principal (accrued) and it is all paid back at the end of the loan. This type of loan provides flexibility to the borrower but it is also risky. In a debt schedule, periodic expenses would only consist of interest expense and no principal payment, as this is consolidated at maturity.

All of these terms essentially mean that a borrower is going to be making a large payment only at the end of the repayment term. With a bullet loan, borrowers can sometimes get access to loans they would not be able to afford as a regular, long-term loan with a monthly payment schedule.

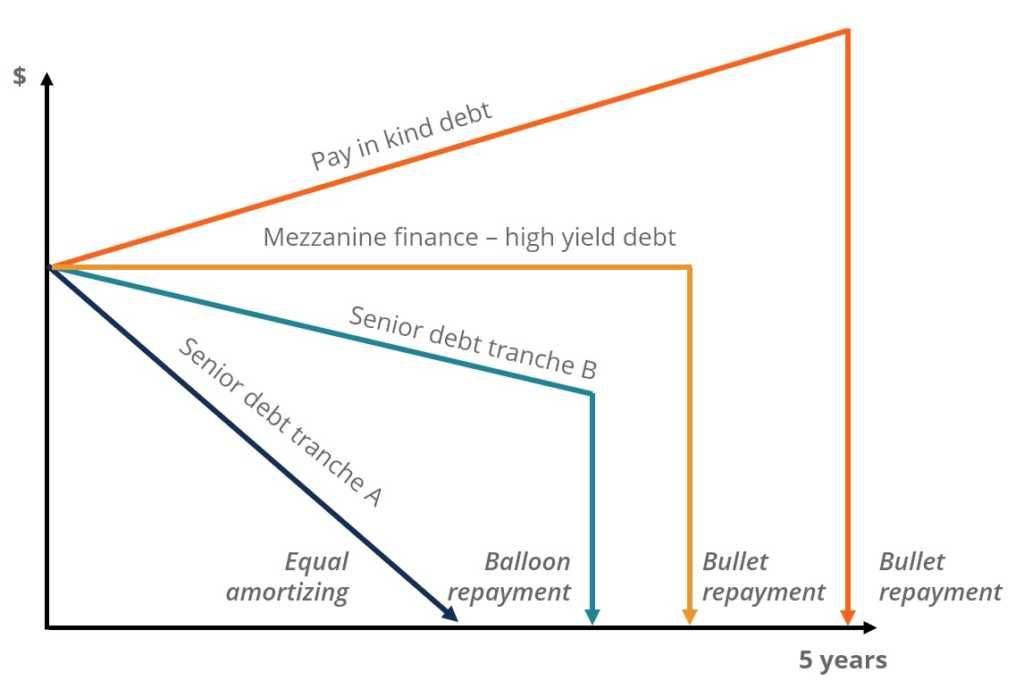

Below is an example of principal repayment profiles for various different types of loans.

Source: CFI’s Free Corporate Finance Course.

One of the primary advantages of this type of loan is that it provides flexibility to the borrower. When an individual is trying to shop for a loan, he or she might find that the loan payments are too high to afford. By getting a bullet loan, the individual can significantly reduce the amount of money that will be due on each payment. In many cases, the borrower is only going to have to pay for the interest that is accruing during each period.

A bullet loan will sometimes also include the interest that is accruing in the amount that is due at the end of the loan. When this happens, the borrower is not going to have to make any payments until the end of the loan. This type of loan is less common, but it can be used in some circumstances. It is most appropriate when the borrower does not want to be burdened with high monthly loan payments now but has a reasonable expectation of receiving the necessary cash flow to repay the loan by the end of the loan term.

Even though a bullet loan can be beneficial, it is also extremely risky. Many borrowers have faced issues with this type of loan after getting involved with one. One of the biggest problems is that many borrowers do not make the proper arrangements to be able to make the balloon payment at the end of the loan term.

The balloon payment comes due and the borrower does not have the money to pay it. In that case, the lender will foreclose on any property that is securing the loan.

Bullet loans are also refinanced quite frequently. Borrowers often use the loan to get quick access to the money they need. They then take advantage of the small monthly payments associated with the bullet loan. When the balloon payment comes due, they will refinance into another loan.

Thank you for reading the CFI guide to bullet loans and their pros/cons. CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level.

To keep learning and advancing your career, the following resources will be helpful:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: