Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

A bridge loan is a short-term form of financing that is used to meet current obligations before securing permanent financing. It provides immediate cash flow when funding is needed but is not yet available.

A bridge loan comes with relatively high interest rates and must be backed by some form of collateral such as business inventory or real estate property. The loan can be accessed by either individuals and companies to meet certain obligations.

Bridge loans are usually arranged within a short time and with little documentation. For example, if there is a lag between the purchase of a real estate property and the disposal of another property, the buyer may take a bridge loan to facilitate the purchase.

In this case, the original property becomes the collateral for the loan. Once long-term financing is available, it is used to pay back the bridge loan and also meet other capitalization needs. Bridge loans are mainly used in real estate to retrieve property from foreclosure or to close on a property quickly.

There are four types of bridge loans, namely: open bridging loan, closed bridging loan, first charge bridging loan, and second charge bridging loan.

A closed bridging loan is available for a predetermined timeframe already been agreed upon by both parties. It is more likely to be accepted by lenders because it gives them a greater degree of certainty about the loan repayment. It attracts lower interest rates than an open bridging loan.

The repayment method for an open bridge loan is undetermined at the initial inquiry, and there is no fixed payoff date. In a bid to ensure the security of their funds, most bridging companies deduct the loan interest from the loan advance.

An open bridging loan is preferred by borrowers who are uncertain about when their expected finance will be available. Due to the uncertainty on loan repayment, lenders charge a higher interest rate for this type of bridging loan.

A first charge bridging loan gives the lender a first charge over the property. If there is a default, the first charge bridge loan lender will receive its money first before other lenders. The loan attracts lower interest rates than the second charge bridging loans due to the low level of underwriting risk.

For a second charge bridging loan, the lender takes the second charge after the existing first charge lender. These loans are only for a small period, typically less than 12 months. They carry a higher risk of default and, therefore, attract a higher interest rate.

A second charge loan lender will only start recouping payment from the client after all liabilities accrued to the first charge bridging loan lender have been paid. However, the bridging lender for a second charge loan has the same repossession rights as the first charge lender.

A bridge loan is used in the real estate industry to make a down payment for a new home. As a homeowner looking to buy a new house, you have two options.

The first option is to include a contingency in the contract for the house you intend to buy. The contingency would state that you will only buy the house after the sale of your old house is complete. However, some sellers might reject this option if other ready buyers are willing to purchase the house instantly.

The second option is to get a loan to pay a down payment for the house before the sale of the first house goes through. You can take a bridge loan and use your old house as collateral for the loan.

The proceeds can then be used to pay a down payment for the new house and cover the costs of the loan. In most cases, the lender will offer a bridge loan worth approximately 80% of the combined value of both houses.

Business owners and companies can also take bridge loans to finance working capital and cover expenses as they await long-term financing. They can use the bridge loan to cover expenses such as utility bills, payroll, rent, and inventory costs.

Distressed businesses can also take up bridge loans to ensure the smooth running of the business, while they search for a large investor or acquirer.

One of the advantages of bridge loans is that it allows you to secure opportunities that you would otherwise miss. A homeowner looking to buy a new house may put a contingency in the contract stating that he/she will only buy the house after selling their old house.

However, some sellers may not be comfortable with such an agreement and might end up selling the property to other ready buyers. With a bridge loan, you can pay a down payment for the house as you wait for the sale of the other house to finalize.

Also, qualifying and getting approved for a bridge loan takes less time than a traditional loan. The speedy processing of a bridge loan gives you the convenience of buying a new home while waiting for the best offer for the old house.

The long waiting time for traditional loans may force you to rent an apartment, and this may affect your budget. Also, bridge loans allow for flexible payment terms depending on the loan agreements. You can choose to start paying off the loan before or after securing long-term financing or selling the old property.

Taking a bridge loan will leave you with the burden of paying two mortgages and a bridge loan while you wait for the sale of your old house to go through or for long-term financing to close.

If you default on your loan obligations, the bridge loan lender could foreclose on the house and leave you in even more financial distress than you were prior to taking the bridge loan. Plus, the foreclosure might leave you with no home.

As a short-term form of financing, bridge loans are costly, due to the high interest rates and associated fees like valuation payments, front-end charges, and lender legal fees. Also, some lenders insist that you must take a mortgage with them, limiting your ability to compare mortgage rates across different firms.

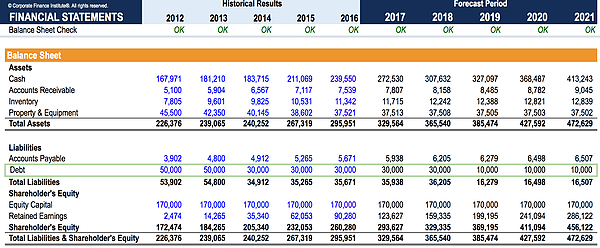

In financial modeling, it may be necessary to build in the functionality for the model to have a bridge loan that kicks in if the company runs out of cash.

In many types of financial models, there will be a revolver built it, but a more substantial piece of short-term debt may be required if the company looks like it will have a negative cash balance. In this case, the analyst will add a short-term debt tranche to the debt schedule as well as on the balance sheet under short-term debt.

To learn more, launch our financial modeling courses!

Bridge loans provide fast, short-term financing to cover immediate obligations while waiting for permanent funding or property sales. They’re most useful when timing matters, whether purchasing real estate quickly or maintaining business operations during transitions.

However, the speed and convenience provided by bridge loans can come at a cost: higher interest rates, additional fees, and the risk of managing multiple debt obligations simultaneously.

To increase your knowledge and advance your career, see the following free CFI resources: