Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

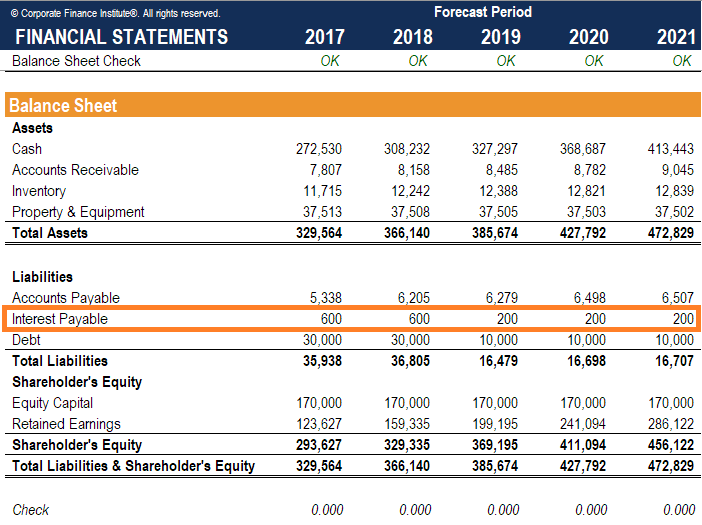

Interest accrued, but not paid

Interest Payable is a liability account, shown on a company’s balance sheet, which represents the amount of interest expense that has accrued to date but has not been paid as of the date on the balance sheet. In short, it represents the amount of interest currently owed to lenders.

For example, if interest of $1,000 on a note payable has been incurred but is not due to be paid until the next fiscal year, for the current year ended December 31, the company would record the following journal entry:

DR Interest Expense 1,000

CR Interest Payable 1,000

Interest payable amounts are usually current liabilities and may also be referred to as accrued interest. The interest accounts can be seen in multiple scenarios, such as for bond instruments, lease agreements between two parties, or any note payable liabilities.

Interest payable accounts are commonly seen in bond instruments because a company’s fiscal year end may not coincide with the payment dates. For example, XYZ Company issued 12% bonds on January 1, 2017 for $860,652 with a maturity value of $800,000. The yield is 10%, the bond matures on January 1, 2022, and interest is paid on January 1 of each year.

On January 1, 2017:

DR Cash 860,653

CR Bond Payable 860,653

The issuance of the bond is recorded in the bonds payable account. The 860,653 value means that this is a premium bond and the premium will be amortized over its life.

On December 31, 2017:

DR Interest Expense 83,869

DR Bond Payable 12,131 (60,653/5yrs)

CR Interest Payable 96,000

The interest expense is the bond payable account multiplied by the interest rate. The payable is a temporary account that will be used because payments are due on January 1 of each year. And finally, there is a decrease in the bond payable account that represents the amortization of the premium.

Therefore, on the balance sheet, the accounts would look like:

Bond Payable 848,522

Interest Payable 96,000

On January 1, 2018:

DR Interest Payable 96,000

CR Cash 96,000

Finally, the payable account is removed because cash is paid out. This payment represents the coupon payment that is part of the bond.

Interest payable accounts also play a role in note payable situations. For example, XYZ Company purchased a computer on January 1, 2016, paying $30,000 upfront in cash and with a $75,000 note due on January 1, 2019. The current interest rate is 10%.

On January 1, 2016:

DR Equipment 86,459

CR Cash 30,000

CR Note Payable 56,349

The note payable is $56,349, which is equal to the present value of the $75,000 due on December 31, 2019. The present value can be calculated using MS Excel or a financial calculator.

On December 31, 2016:

DR Interest Expense 5,635

CR Note Payable 5,635

The interest for 2016 has been accrued and added to the Note Payable balance.

On December 31, 2017:

DR Interest expense 6,198

CR Note Payable 6,198

On December 31, 2018:

DR Interest expense 6,812

CR Note Payable 6,812

On January 1, 2019:

DR Note Payable 75,000

CR Cash 75,000

The Note Payable account is then reduced to zero and paid out in cash.

Thank you for reading CFI’s guide to Interest Payable. To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: