Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

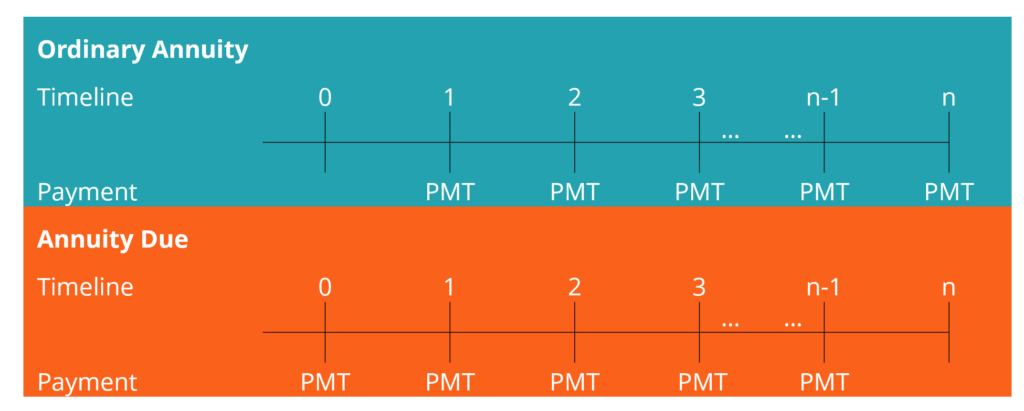

A series of equal payments made at the same interval at the start of each period

Annuity due refers to a series of equal payments made at the same interval at the beginning of each period. Periods can be monthly, quarterly, semi-annually, annually, or any other defined period. Examples of annuity due payments include rentals, leases, and insurance payments, which are made to cover services provided in the period following the payment.

The annuity due can be illustrated as follows:

The first payment is received at the start of the first period, and thereafter, at the beginning of each subsequent period. The payment for the last period, i.e., period n, is received at the beginning of period n to complete the total payments due.

The present value of an annuity due uses the basic present value concept for annuities, except we should discount cash flow to time zero.

The formula for the present value of an annuity due is as follows:

Alternatively,

Where:

The second formula is intuitive, as the first payment (PMT on the right side of the equation) is made at the start of the first period, i.e., at time zero; hence it comes without a discounting effect.

Example

An individual makes rental payments of $1,200 per month and wants to know the present value of their annual rentals over a 12-month period. The payments are made at the start of each month. The current interest rate is 8% per annum.

Using the formula above:

FV of the Investment = $1,200 x 11.57

FV of the Investment = $13,886.90

The future value of an annuity due uses the same basic future value concept for annuities with a slight tweak, as in the present value formula above.

To calculate the future value of an ordinary annuity:

Where:

Example

A company wants to invest $3,500 every six months for four years to purchase a delivery truck. The investment will be compounded at an annual interest rate of 12% per annum. The initial investment will be made now, and thereafter, at the beginning of every six months. What is the future value of the cash flow payments?

Using the formula above:

FV of the Investment = $3,500 x 10.49

FV of the Investment = $36,719.61

The calculations for PV and FV can also be done via Excel functions or by using a scientific calculator.

The major difference between annuity due and the more popular ordinary annuity is that payments for an ordinary annuity are made at the end of the period, as opposed to annuity due payments made at the start of each period/interval. Ordinary annuity payments include loan repayments, mortgage payments, bond interest payments, and dividend payments.

Another difference is that the present value of an annuity due is higher than one for an ordinary annuity. It is a result of the time value of money principle, as annuity due payments are received earlier.

Hence, if you are set to make ordinary annuity payments, you will benefit from getting an ordinary annuity by holding onto your money longer (for the interval). Conversely, if you are set to receive annuity due payments, you will benefit, as you will be able to receive your money (value) sooner. In any annuity due, each payment is discounted one less period in contrast to a similar ordinary annuity.

The relationship in equation terms can be illustrated as below:

PV of an Annuity Due = PV of Ordinary Annuity * (1+i)

Multiplying the PV of an ordinary annuity with (1+i) shifts the cash flows one period back towards time zero.

The last difference is on future value. An annuity due’s future value is also higher than that of an ordinary annuity by a factor of one plus the periodic interest rate. Each cash flow is compounded for one additional period compared to an ordinary annuity.

The formula can be expressed as follows:

FV of an Annuity Due = FV of Ordinary Annuity * (1+i)

Thank you for reading CFI’s guide to Annuity Due. To keep learning and developing your knowledge base, please explore the additional relevant resources below: