Annuity Table

Calculates the present value and future value of the annuity, considering the value and the time period of the investment

What is an Annuity Table?

An annuity table is a method that helps in understanding the worth of an annuity. It calculates the present value and future value of the annuity, considering the value and the time period of the investment. The table helps an investor in making informed decisions while planning for investments.

Annuities are either lump-sum payments or multiple payments made at regular intervals. The deposits made to savings accounts, monthly rent payments, and retirement pensions are considered annuities. The payments received from an annuity are reported as income, and the amount of tax to be paid depends on the product.

Summary

- An annuity table aids in finding out the present and future values of a sequence of payments made or received at regular intervals.

- It helps an investor to make informed decisions regarding investment planning.

- An annuity table cannot be used for non-discrete interest rates and time periods.

Annuity Table and the Worth of an Annuity

The annuity table consists of a factor specific to the series of payments an investor is expecting to receive at regular intervals and a particular interest rate. The number of payments is on the y-axis, and the rate of interest, or the discount rate, is on the x-axis. The intersection of the number of payments and the discount rate presents a factor that is multiplied by the value of payments, providing the present value of the annuity.

One can also determine the future value of a series of investments using the respective annuity table. For example, the annuity table can be used to determine the present value of the annuity that is expected to make eight payments of $15,000 at a 6% interest rate, as well as the value of the payments on of a future date.

Present Value of Annuity, Future Value of Annuity, and the Annuity Table

The annuity table provides a quick way to find out the present and final values of annuities. However, the table works for discrete values only. However, in the real world, interest rates and time periods are not always discrete. Therefore, there are certain formulas to compute the present value and future value of annuities.

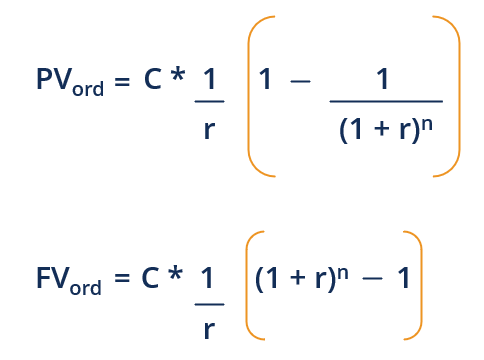

1. Regular annuity

A regular annuity is where the regular payments are required or made at the end of a period for a specific length of time. The present and future values of an annuity can be calculated as:

Where:

- PVord – Present value of ordinary annuity

- FVord – Future value of ordinary annuity

- C – Cash flows, which are annuity payments in this case

- r – Interest rate

- n – Number of periods for which payments are to be made or required

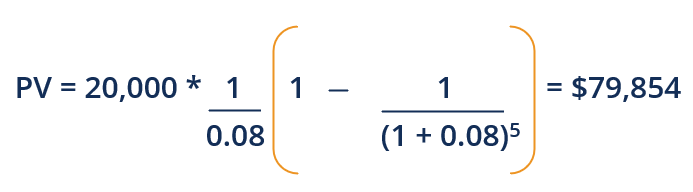

Assume that you are offered an annuity that pays $20,000 at the end of each year for five years at an 8% interest rate, or you can receive a lump-sum amount of $75,000 today. Which option is better?

To compare both options, let’s find out the present value of the annuity.

Here, the annuity value is higher; hence, it would be reasonable to choose the annuity over the lump-sum amount.

2. Annuity due

If regular payments are made or required at the beginning of each period for a certain length of time, the annuity is called an annuity due. The present and future values of an annuity due can be computed as follows:

Where:

- PVdue – Present value of annuity due

- FVdue – Future value of annuity due

Assume that in the example above, the annuity payment is to be received at the beginning of each year. Then, the present value of the annuity will be:

PVdue = PVord (1 + r)

PVdue = 79,854 (1 + 0.08)

PVdue = $86,242

The annuity due value is greater; hence, you should choose the annuity due over the lump-sum payment. In case you are given an option to choose between the two types of annuities, you should choose annuity due, as its value is more than the ordinary annuity.

More Resources

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful:

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.