Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A form of direct money lending to individuals or businesses without an official financial intermediary

Peer-to-peer lending is a form of direct lending of money to individuals or businesses without an official financial institution participating as an intermediary in the deal. P2P lending is generally done through online platforms that match lenders with the potential borrowers.

P2P lending offers both secured and unsecured loans. However, most of the loans in P2P lending are unsecured personal loans. Secured loans are rare for the industry and are usually backed by luxury goods. Due to some unique characteristics, peer-to-peer lending is considered as an alternative source of financing.

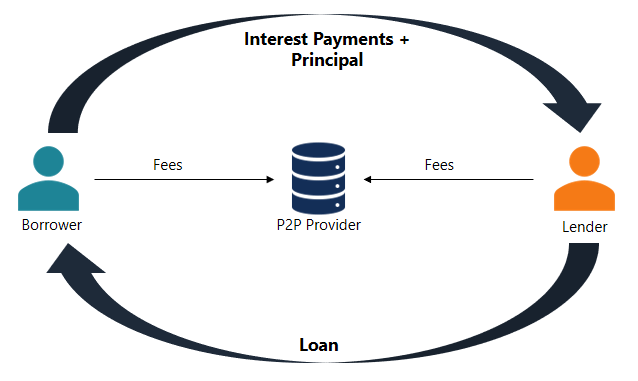

Peer-to-peer lending is a fairly straightforward process. All the transactions are carried out through a specialized online platform. The steps below describe the general P2P lending process:

The company that maintains the online platform charges a fee for both borrowers and investors for the provided services.

Peer-to-peer lending provides some significant advantages to both borrowers and lenders:

Nevertheless, peer-to-peer lending comes with a few disadvantages:

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To learn more about related topics, check out the following free CFI resources: