Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Unique items include proved reserves, unproved reserves, asset retirement obligation, and derivative fair value

The oil and gas industry is vast and contributes to a significant portion of the world’s energy consumption. Like many other industries, oil and gas companies own specific line items unique to them. Here, we look at unique line items on oil and gas company balance sheets.

For oil companies doing exploration and production, the line items include proved reserves, probable reserves, and possible reserves. There is also an asset retirement obligation line item, which refers to the cost of shutting down or retiring the operation. Lastly, the derivative fair value item is a reference to the company’s hedged position against fluctuating commodity prices. These unique balance sheet items can be important to financial analysts assessing oil and gas companies.

Proved reserves, probable reserves, and possible reserves refer to the potential crude oil that can be extracted by an oil and gas company. The quantity of the oil that can be extracted from an oil reserve always involves some uncertainty in the estimate. It is based on the amount of geological and engineering information available regarding the oil reserve in question.

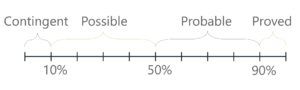

The levels of uncertainty when estimating the amount of oil in the reserves vary, and that is why reserves are separated into two broad categories: proved and unproved. Within the category of unproved, oil reserves fall under the sub-categories of probable and possible.

Proved reserves are oil reserves with the highest certainty. The oil that can be extracted from such reserves must show at least a 90% probability of recovery to be classified as such. It is based on geological and engineering data and must also take into account operating methods, economic conditions, and government regulations.

The unproved reserves category encapsulates the probable and possible categories. Unproved reserves come with greater uncertainty when it comes to either technical, economic, or regulatory factors. It leads to a less than 90% probability of recovery.

An oil reserve with a recovery probability of less than 90% but at least 50% falls under the probable category. Here, there is a reasonable likelihood of recovery; however, circumstances such as the lack of sufficient geological data or the inability to institute proper underground controls prevent a higher level of certainty.

The last commonly used category falls under possible. The probability of possible oil reserves is highly uncertain and falls between the 10% and 50% threshold for recovery. Often, reserves that are known are categorized here when the ability to produce at commercial rates comes into question.

Oil reserves with extreme uncertainty can fall within the category of contingent reserves. The probability of certainty regarding such reserves is less than 10%. The contingent reserves line item is seldom seen on oil and gas balance sheets.

The following summarizes the categories of oil reserves:

The three line items above are classified as a long-term asset and show up on the balance sheet under property, plant, and equipment. Although the line items are not required, often companies will invest the time and research into adding them. It is especially true of smaller companies looking to prove their commercial viability in the hopes of merging or being acquired.

The asset retirement obligation is a legal obligation to clean up, shut down, or retire a long-lived asset. It can exist in any industry; however, it is especially important in oil and gas. Since all oil reserves are finite, the production facilities used in extraction will be retired at the end of its life. The activities commonly referenced in the asset retirement obligation include:

The asset retirement obligation will be recorded in the period in which it is incurred if a reasonable approximation of the fair value can be made. It can be at the time of an acquisition or during construction. If a reasonable approximation cannot be made, the asset retirement obligation will be made when it can be approximated. As more production equipment and well sites are constructed, the asset retirement obligation will increase to reflect the higher future retirement cost. The item shows up in the balance sheet under long-term liabilities.

The derivative fair value item is not specifically unique to only oil and gas companies. It is, however, a very commonly seen item on oil and gas company balance sheets. Within the industry, the prices of commodities, such as oil, are set by the market. To deal with constantly fluctuating prices, oil and gas companies can hedge their position using derivatives. The derivatives include forwards, futures, and options.

For example, a company may engage in a forward contract to sell a set amount of oil at $50 a barrel. The line item, as its name suggests, is recognized at its fair value. The derivative fair value line can be either an asset or a liability. If a company has hedged its position and has entered into a derivative contract to sell at a set price, the derivative fair value item will show up as an asset. If a company has hedged its position and entered into a contract to buy at a set price, the derivative fair value item will show up as a liability.

The line items mentioned above are important in understanding companies within the oil and gas industry. Since such companies are very dependent on the finite resource they are extracting, assessing the availability and probability it can be extracted at can help give a proxy to the company valuation. For example, when screening companies, one may look at how many proved reserves they own. Reserves can also be made into valuation multiples to compare different companies.

Understanding the asset retirement obligation is also very important in assessing an oil and gas company. The asset retirement obligation line item can be monitored over time to determine the costs of retiring the facilities that are constructed over the period of extraction. If a known number of facilities or equipment will be used for future extraction, understanding the line item can help forecast the future costs of the company.

Finally, identifying and assessing the derivative fair value items that may be present on the company balance sheets can give an idea as to how hedged the company’s position may be. It can be a component that factors into the risk profile of a company. It can also be an indicator of how prices are capped at a company, i.e., in situations where oil prices increase dramatically.

CFI offers the Financial Modeling & Valuation Analyst (FMVA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover: