Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A key metric used to value oil and gas companies in the energy sector

The EV/2P ratio is a ratio (also known as a multiple) that is particularly used to value oil and gas companies in the energy sector. It is calculated by dividing a company’s enterprise value (EV) by its proven and probable (2P) reserves.

Analysts can understand how a company’s reserve resources support its growth and operation based on the EV/2P ratio. By comparing the EV/2P ratios of a group of peers, analysts can also tell whether a company is overvalued or undervalued by the market.

The EV/2P ratio is one of the many types of valuation ratios that shows the relationship between the market value of a company and its fundamental financial performance. The metric allows analysts to understand whether the market values a company or a stock more expensive (overvalued) or cheaper (undervalued) compared to its peers.

The EV/EBITDA ratio, P/E (Price-to-Earnings) ratio, and P/B (Price-to-Book) ratio are some of the generally used valuation ratios applied in different industries. The EV/2P ratio performs a similar function to the commonly used ratios, but it is particularly used in valuing oil and gas companies.

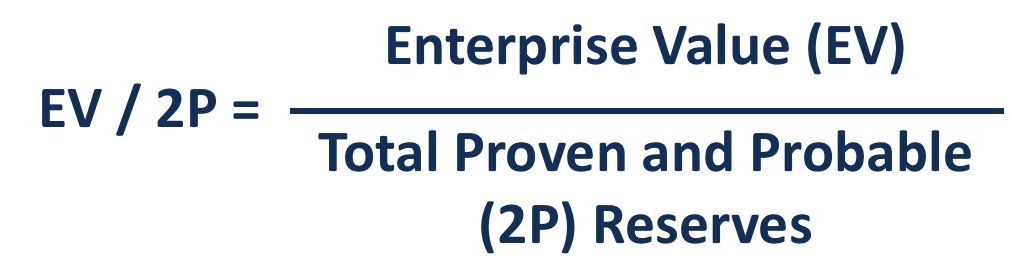

The numerator enterprise value measures the total market value of a firm claimed by both shareholders and bondholders, which is net of cash. The denominator 2P is a sum of proven and probable reserves.

Reserves are a significant indicator to value the production and growth potential of an oil and gas company, which can be classified into three categories based on the quality. Proven reserves (P1) are the best-quality reserves with a 90% possibility or above of being produced and are also known as P90.

Probable reserves (also known as P50) have at least a 50% likelihood of being extracted, with a lower quality than proven reserves. Proven and probable reserves together are known as 2P.

Possible reserves have the lowest quality and possibility of extraction, which is only between 10% and 50%. Due to the low possibility of being successfully extracted and recovered, possible reserves are not considered in the valuation.

The EV/2P ratio is calculated by dividing the enterprise value (EV) of a company by the sum of its proven and probable (2P) reserves.

Where:

Here is an example to better understand the EV/2P ratio. Let us assume an oil company reports a market capitalization of $800m and a net debt of $400m. The company also holds $60m of proven reserves, $40m of probable reserves, and $80m of possible reserves.

Thus, the enterprise value of the company is $1,200m ($800m + $400m), and the value of 2P reserves is $100m ($60m + $40m), which leads to a EV/2P ratio of 12.0x ($1,200m / $100m). It means the company is valued to be $12 for each dollar value of its 2P reserves by the market.

As a measure of relative valuation, the EV/2P ratio of a company is typically compared with the industry average or median. If a company shows a higher EV/2P ratio than its peers, it is valued more than the others for the same amount of 2P reserves. It means its shares are sold more expensive than the others in the stock market, vice versa. Investors typically prefer to purchase undervalued stocks, which can offer greater capital appreciation headroom.

Sometimes, a company’s higher valuation can be justified, especially when the company demonstrates a stronger financial or operational performance or a better prospect due to other reasons than its peers. Therefore, analysts need to pair quantitative comparisons with qualitative analysis to get a whole picture.

One of the major concerns of using the EV/2P ratio is debt impact. Due to the capital-intensive nature of the industry, oil companies are typically highly levered, as large amounts of debt are financed for exploration, oil rigs, and equipment. Since enterprise value captures both equity and debt values, analysts should take a step further to consider the capital structure while comparing the companies.

CFI is the official provider of the Financial Modeling & Valuation Analyst (FMVA)® certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: