Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

Real assets are physical, tangible investments like real estate and commodities, while financial assets are intangible contracts like stocks and bonds. Real assets derive value from their physical properties, while financial assets get value from contractual claims or ownership rights.

Real assets versus financial assets represent the fundamental classification system in portfolio construction. Real assets provide inflation protection and diversification benefits, while financial assets offer liquidity and efficient market access.

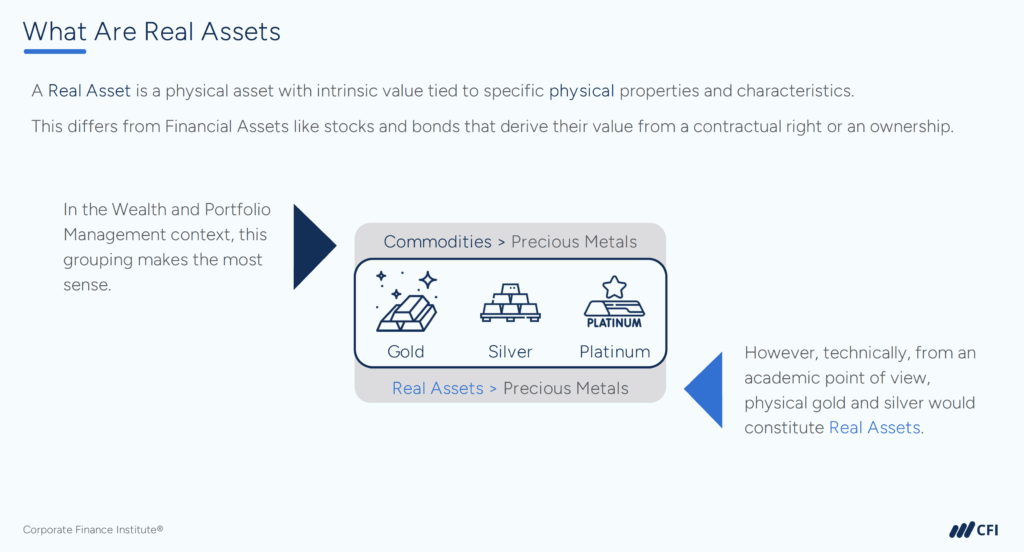

Real assets are tangible assets with intrinsic value derived from their physical properties and substance. Real assets provide utility independent of financial market conditions and offer direct exposure to economic fundamentals.

Key characteristics of real assets:

Real assets fall into four primary categories: real estate, infrastructure, natural resources, and productive land. Each type offers different risk-return profiles and portfolio benefits.

The complexity of investing in real assets requires professional management, thorough client suitability assessments, specialized due diligence, and longer investment horizons.

Financial assets are essentially paper or digital claims to value, such as money held in a bank account or stocks and bonds. Financial assets don’t have physical qualities you can use or consume. Instead, financial assets are valuable because they represent an agreement or ownership.

For example, a stock certificate or brokerage account entry represents part ownership of a company, and a bond note represents someone’s promise to repay you with interest. Many financial assets entitle investors to cash flows, such as dividends on stocks or interest payments on bonds.

Key characteristics of financial assets:

Financial assets include four primary categories: equity securities, fixed income securities, cash equivalents, and investment funds. Each category serves different portfolio objectives and risk tolerances.

Real assets and financial assets differ in three key ways: how their value is determined, liquidity characteristics, and risk profiles. Real assets require specialized valuation and offer lower liquidity, while financial assets provide transparent pricing and immediate market access.

| Form | Physical, tangible investments | Intangible contracts and ownership claims |

| Source of Value | Intrinsic value, or assets that can be used or consumed directly | Extrinsic value, or a claim on assets for future financial returns or cash flows |

| Liquidity | Low liquidity, or assets take longer to convert into cash in closed markets, pricing more subjective. | High liquidity - assets easily converted to cash through open markets, such as exchanges, with transparent pricing. |

| Income and Use | Provides income and consistent cash flow (though this varies by asset type) through long-term contracts and leases and direct use or consumption. | Predictable income through regular payments, like interest on a bond or dividends on a stock but offer no direct use. |

| Sensitivity to Market Factors | Varies by asset type but tend to have lower correlation with stock markets and often hold value or appreciate when interest rates or inflation rises. | Can lose purchasing power in inflationary periods unless instruments have inflation-linked features |

| Examples | Real estate, infrastructure, commodities, timberland | Stocks, bonds, cash equivalents, derivatives, futures contracts |

Inflation hedging is a strategy investors and companies use to protect the value of their money or assets from being eroded by rising prices. When inflation increases, the purchasing power of cash declines. An inflation hedge aims to offset or outpace that decline.

Real assets serve as effective inflation hedges because their values typically adjust with rising price levels. Fixed-rate financial assets often lose purchasing power during inflationary periods, making allocations to real assets essential for long-term portfolio protection.

Many real assets are scarce. Land, oil, and precious metals can’t be printed or manufactured at will, so when inflation picks up, the demand for these assets often pushes their prices higher. This scarcity makes them effective stores of value.

Some real assets also generate income that can adjust upward with inflation. For example:

Imagine you own a 20-unit apartment building. Each unit currently rents for $1,000 per month.

The total annual rental income is $240,000 (20 × $1,000 × 12). Operating costs (maintenance, property taxes, utilities, staff, etc.) are $100,000 per year for a net operating income (NOI) of $140,000.

In this scenario:

This is how real estate acts as an inflation hedge. Net income and the underlying asset value generally move in step with inflation, preventing erosion of investor wealth.

Portfolio diversification is an investment strategy where you spread your money across a variety of assets instead of putting it all into one type of investment. The goal is to reduce risk while aiming for steady returns over time.

Real assets can play an important role in portfolio diversification because they behave differently from traditional financial assets like stocks and bonds.

Suppose a portfolio has 70% stocks and 30% bonds. It might perform well in stable, low-inflation periods but become vulnerable if inflation rises and bond prices fall. By adding 10–15% real estate or commodities, the portfolio holds assets that may appreciate during inflationary periods, reducing overall volatility.

Real assets are tangible items like real estate, commodities, and infrastructure, whose value comes from their physical properties and role in the economy. Financial assets, such as stocks and bonds, are intangible and their value depends on the performance of the issuing entity, such as a company’s financial performance.

Real assets hold value on their own, while financial assets rely on the success and stability of whoever issued them.

Real assets are tangible investments like property and commodities whose physical properties hold value. Financial assets are contracts like stocks and bonds that derive value from claims on other entities.

Real assets provide inflation protection, portfolio diversification through low correlation with traditional securities, and steady income streams that help investors meet long-term obligations.

Real assets have different risk profiles because this asset class is less liquid and potentially more complex. However, real assets can provide better inflation protection and lower correlation with market volatility than financial assets.

Ready to further your journey in finance? Explore CFI’s comprehensive course catalog and certification programs to build the skills you need for your chosen path. Whether you’re interested in financial modeling, corporate finance, or investment banking, CFI’s structured learning paths can help you achieve your finance career goals.

Intrinsic Value vs. Market Value