Get In-Demand Finance Certifications

Earnings Per Share after adjusting the number of shares outstanding for dilutive securities

The Diluted EPS formula is equal to net income less preferred dividends, divided by the total number of diluted shares outstanding (basic shares outstanding plus the exercise of in-the-money options, warrants, and other dilutive securities).

Diluted EPS Formula:

Diluted EPS = (net income – preferred dividends) / (weighted average number of shares outstanding + the conversion of any in-the-money options, warrants, and other dilutive securities)

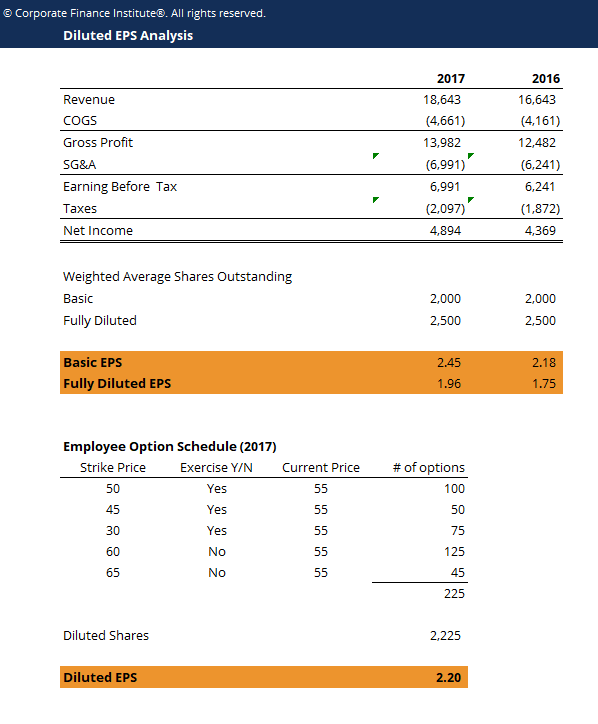

Below is a simple example of how to calculate diluted EPS for a company without any preferred shares.

Download the free Excel template now to advance your finance knowledge!

As you will notice in the analysis that was performed, the number of diluted shares outstanding was derived by adding up the number of in-the-money options and assuming they were added to the basic number of shares outstanding in the period.

By doing a full analysis (as shown) we see that in 2017 Basic EPS is $2.45, Diluted EPS is $2.20, and Fully Diluted EPS is $1.96.

The diluted EPS figure of $2.20 paints the most accurate picture for an investor, while the fully diluted EPS figure of $1.96 presents the most conservative (or worst case) scenario.

The reason that analysts and investors calculate diluted EPS is that basic EPS may overstate the actual amount of earnings per share that a common shareholder is entitled to.

Companies frequently have dilutive securities outstanding like options and warrants that will increase the total number of shares outstanding when converted.

Since the conversion of options into shares won’t add any additional net income to the business, the increased share count makes the conversion dilutive.

Options may have been granted to employees, for example, that are in-the-money (strike price is below the current market price) but have not been converted yet. If options are in-the-money, they should be accounted for in a diluted EPS calculation.

To learn more, launch the CFI financial analysis courses now!

The numerator of the EPS formula is Net Income – Preferred Dividends. Preferred dividends need to be deducted from net income, since that portion of earnings will not be available to common shareholders, and we are calculating the Earnings Per Share (EPS) for common shareholders.

The standard calculation for Earnings Per Share is net income divided by shares outstanding. In the case of a company that pays a preferred dividend, the EPS for common shareholders is Net Income less Preferred Dividends (since those get paid out first) divided by shares outstanding.

To learn more, launch our financial analysis courses now!

The denominator of the EPS formula is Weighted Average Basic Shares Outstanding + Options + Warrants + Other dilutive securities that are in-the-money.

The weighted average basic shares outstanding is the average number of shares that were outstanding over the time period. If for example, the time period was one year and no shares were issued or repurchased during the year, then the beginning number of shares, ending number of shares, and weighted average number of shares are all equal to each other.

By looking at the notes in a company’s financial statements, you will find a schedule with a list of all the issued options and warrants, along with their strike or conversion prices and maturity dates.

This is where most of the effort is required. A good financial analyst will recreate a table in Excel with all the details, then compare the strike/conversion prices to the current share price (or average share price over the period) and determine which securities are in-the-money.

The next step is to assume those securities are converted, the company receives the cash, and the number of shares outstanding goes up.

It should be noted that you can take the fully diluted number of shares outstanding as the denominator if you want to be the most conservative. It could be overly conservative though, as some of the options may be far out-of-the-money and never convert into shares. For this reason, it’s better to do take the steps

Below is a short video tutorial that explains how the diluted EPS formula is structured with an example.

Download the Diluted EPS Formula Excel Template from the Example at the top of this article. The best way to understand how this works is to take the template, audit all the calculations, and try building it again with your own numbers.

Practice makes perfect when it comes to financial modeling, and other ad hoc pieces of financial analysis, such as this diluted EPS calculator.

To learn analysis, launch the CFI financial analysis courses now!

Thank you for reading CFI’s guide to Diluted EPS Formula and Calculation. To keep learning and developing your skills, please see our most relevant additional resources below:

Below is a break down of subject weightings in the FMVA® financial analyst program. As you can see there is a heavy focus on financial modeling, finance, Excel, business valuation, budgeting/forecasting, PowerPoint presentations, accounting and business strategy.

A well rounded financial analyst possesses all of the above skills!

CFI is the global institution behind the financial modeling and valuation analyst FMVA® Designation. CFI is on a mission to enable anyone to be a great financial analyst and have a great career path. In order to help you advance your career, CFI has compiled many resources to assist you along the path.

In order to become a great financial analyst, here are some more questions and answers for you to discover:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.