Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The most important concepts to know in business valuation modeling

This business valuation glossary covers the most important concepts to know in valuing a company. This guide is part of CFI’s Business Valuation Modeling Course.

See Firm-Specific Risk for the definition of Alpha.

The Beta (β) of a stock or portfolio is a number describing the correlated volatility of an asset in relation to the volatility of the benchmark that the asset is being compared to. This benchmark typically represents the overall financial market and is often estimated using representative indices, such as the S&P 500.

The Capital Asset Pricing (CAPM) Model is the most widely used risk/return model used to calculate the equity cost of capital.

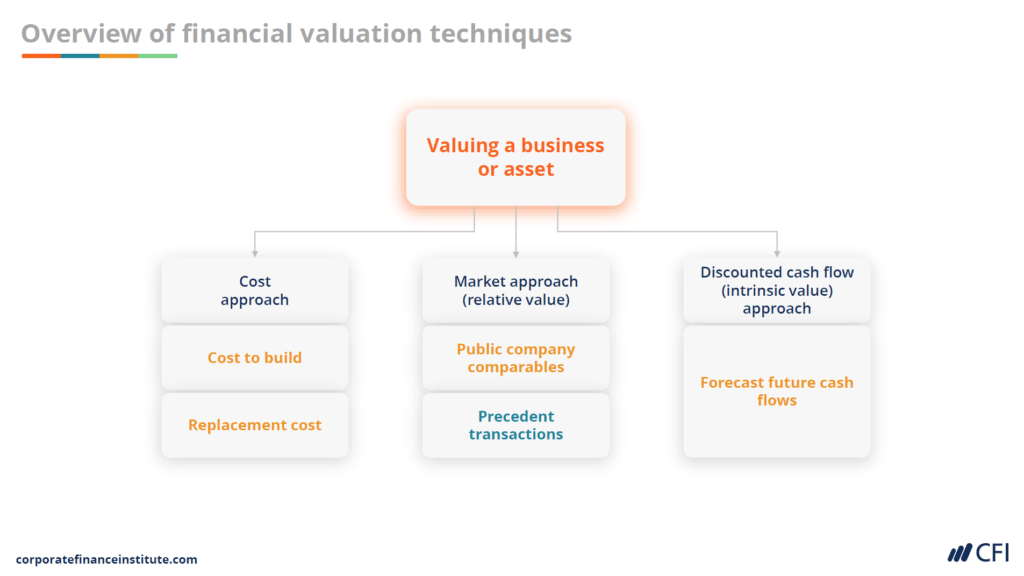

Comps or Comparable Company Analysis involves identifying valuation multiples from comparable listed companies and applying these to the financials of the company to be valued.

The ability of an asset to generate earnings, which are then reinvested in order to generate its own earnings. In other words, compounding refers to generating earnings from previous earnings.

See Comparable Company Analysis.

A constant stream of identical cash flows without end.

A statistical measure of the variance of two random variables that are observed or measured in the same mean time period.

The promises made by the borrowing company in a loan agreement to adhere to specific operational limits.

Raising money for a business through loans or by issuing bonds. A shareholder loan is a debt owed by the company to one of its shareholders, rather than an outside lender.

The discount rate is the percentage rate required to calculate the present value of a future cash flow.

Discounted Cash Flow (DCF) valuation is a method of valuing a company using the concept of the time value of money. All future cash flows are estimated and discounted to give their present values. The sum of all future cash flows, both incoming and outgoing, is the net present value (NPV), which is taken as the value or price of the cash flows in question.

The process of determining the present value of a payment or a stream of payments that is to be received.

See firm-specific risk.

A share of a company’s net profits distributed by the company to a class of its shareholders.

Earnings Before Interest and Tax. Sometimes referred to as operating profit.

Earnings Before Interest, Taxation, Depreciation, and Amortization.

Enterprise Value (EV), also known as Total Enterprise Value (TEV), Entity Value, or Firm Value (FV), is a measure reflecting the market value of a whole business. It is the sum of claims of all security holders, including debt holders, preferred shareholders, minority interests, common equity holders, and others.

A ratio used to determine the value of a company. The enterprise value multiple looks at a company as a potential acquirer would because it takes debt into account – an item which other multiples like the P/E ratio do not include. An example of an enterprise value multiple is EV/EBITDA.

See Enterprise Value.

Total assets less total liabilities. Also referred to as total shareholders’ equity or net worth.

The money acquired from the business owners themselves or from other investors.

A ratio used to determine the value of a company’s equity. An example of an equity multiple is price to earnings.

See Risk Premium for the definition of Equity Risk Premium.

Equity Value is the value of a company available to shareholders. It is the enterprise value plus all cash and cash equivalents, short and long-term investments, and less all short-term debt, long-term debt, and minority interests.

The EV to capital employed multiple is defined as the enterprise value divided by capital employed, where capital employed is the book value of all funding (e.g. debt and equity).

The EV to EBIT multiple is defined as the enterprise value divided by earnings before interest and tax.

The EV to EBITDA multiple is defined as the enterprise value divided by earnings before interest, tax, depreciation, and amortization.

The EV to Free Cash Flows multiple is defined as the enterprise value divided by free cash flows to the firm.

The EV to Sales multiple is defined as the enterprise value divided by sales (also called revenue or turnover).

See Enterprise Value.

Firm-specific risk is sometimes called unsystematic risk, specific risk, diversifiable risk, or alpha. The category includes risks associated with a firm’s management team, operations, projects, products, profits, and so on.

Free Cash Flows to Equity is the cash flow available for distribution to equity holders. If net borrowings remain unchanged, the formula is free cash flows to the firm – Interest Expense x (1 – Tax Rate).

This is the cash flow available for distribution among all the securities holders of an organization (i.e., debt holders, equity holders, etc.). The standard definition is EBIT x (1 – Tax Rate) + Depreciation & Amortization +/- Changes in Working Capital – Capital Expenditure. This can also be referred to as unlevered free cash flow.

All interest-bearing debt (both current and long-term).

A constant stream of cash flows without end that is expected to rise indefinitely.

Market Capitalization is the share price times the number of shares outstanding for a publicly traded company.

Market Risk is often referred to as systematic risk, non-specific risk, non-diversifiable risk, or beta. This category includes risks such as interest rates, the economic cycle, inflation, legislation, and socio-economic developments.

The Multiples Valuation Approach is a valuation theory based on the idea that similar assets sell at similar prices. It assumes that a ratio comparing value to some firm-specific variable (operating margins, cash flow, etc.) is the same across similar firms.

Net debt is all interest-bearing debt (often referred to as gross debt) less cash, cash equivalents, and marketable securities. Net debt assumes that cash and marketable securities are “surplus” or “redundant” and can be used to pay down debt. In practice, It is important to assess whether all cash, cash equivalents, and marketable securities truly are “redundant” or readily disposable.

Net Operating Profit After Tax (NOPAT) is a company’s after-tax operating profit for all investors, including shareholders and debt holders.

NOPAT is typically defined as EBIT x (1 – effective tax rate).

Net Present Value is the sum of the present values of a time series of future cash flows.

See market risk.

See Market Risk.

Earnings adjusted for non-recurring items, over/under depreciation, profit/loss on the sale of assets, etc., so that earnings reflect the ongoing performance of the company.

Precedents or Precedent Transaction Analysis involves identifying recent acquisitions in the same sector and applying the multiples from these transactions to the financials of the company to be valued.

The price to book multiple is defined as the market capitalization (or equity value of common shares) divided by the book value of equity which is total common shareholders’ equity excluding preference shares and minority interest.

The price to cash flow multiple is defined as the market capitalization (or equity value of common shares) divided by free cash flows to equity. Free cash flows to equity is typically defined as cash flows from operations less capital expenditures.

The Price to Earnings Multiple is defined as the market capitalization (or equity value of common shares) divided by the earnings belonging to common shareholders.

Most analysts use the yield on government bonds to determine the risk-free rate even though they are not entirely risk free. This is because it is virtually impossible to get a truly risk-free rate.

Risk Premium is the excess return that the overall stock market provides over the risk-free rate.

A DCF valuation technique that solely uses a DCF perpetuity formula to value a company. It should only be used for companies with stable cash flows that are expected to grow in a predictable manner.

See firm-specific risk.

A measure of the dispersion of a set of data from its mean. The more spread apart the data, the higher the deviation. Standard deviation is calculated as the square root of variance.

See market risk.

Total shareholder return (TSR) is the total return of a stock to an investor including both dividends and capital gains.

A DCF valuation technique that is made up of a finite forecast period and a post-forecast period. The post-forecast period is commonly referred to as the continuing value, terminal value, or TV.

See firm-specific risk.

Variance is a measure of the dispersion of a set of data points around their mean value. Variance is a mathematical expectation of the average squared deviations from the mean.

The Weighted Average Cost of Capital (WACC) incorporates the individual costs of capital for each provider of finance (e.g., debt and equity), weighted by the relative size of their contribution to the overall pool of finance.

CFI’s business valuation glossary covered key concepts from the Business Valuation Modeling Course. To continue learning and advancing your career, these resources will be helpful: