Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Private equity firms look for companies that can support a leveraged structure and still deliver strong returns. At the heart of a good LBO candidate are two things: reliable cash generation and room for value creation.

A good candidate typically shows strength at both the company and industry levels. Strong company fundamentals make it possible to take on debt without adding excessive risk, while supportive industry conditions improve the odds of stable performance over the holding period.

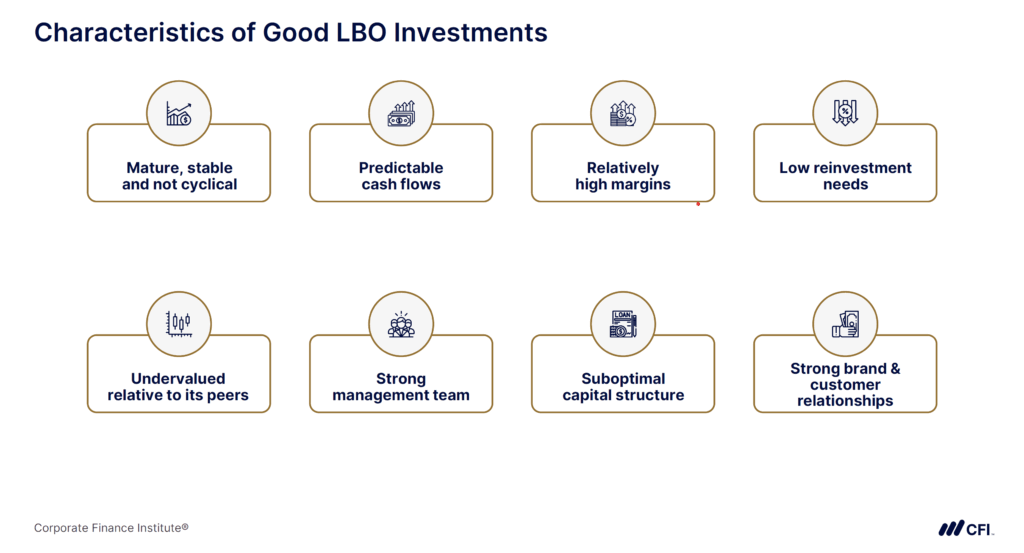

Companies are attractive buyout targets when their financial and operational profile makes it possible to add leverage safely and still create value. Common characteristics include:

The attraction of companies from certain industries comes down to how well their business models line up with the mechanics of a leveraged buyout. Since most of the purchase is financed with debt, private equity firms need confidence that the company can service debt, maintain value, and offer upside at exit.

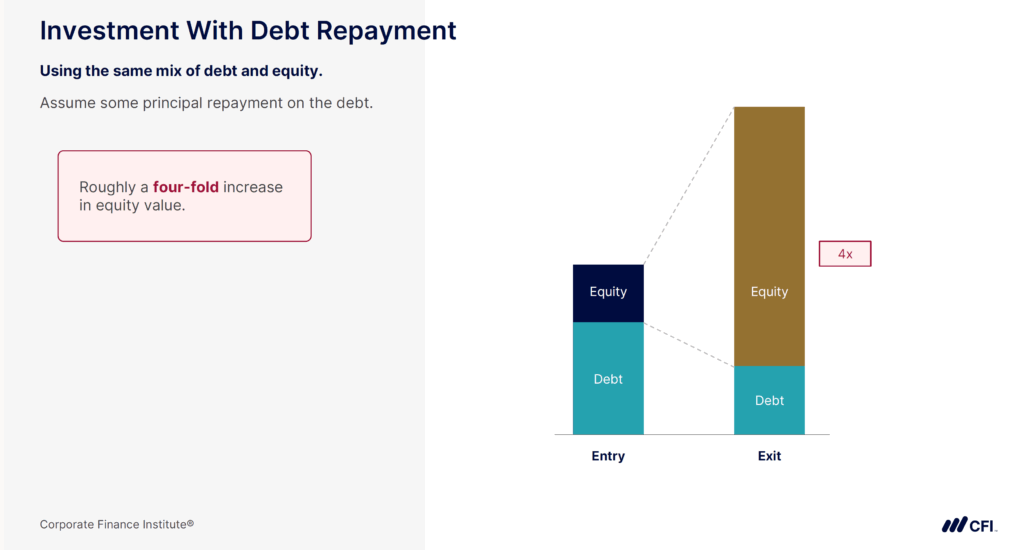

Leveraged buyouts generate returns by reducing the amount of equity investors put in, paying down debt with company cash flows, and ultimately selling the business at a higher value.

To see how these drivers work in practice, consider a private equity firm acquiring a company with an enterprise value (EV) of $100 million. The example below shows how private equity firms use leverage, debt repayment, and operational improvements to generate equity returns in an LBO.

| 1. Leverage (Debt Amplifies Equity Returns) | The PE firm invests a small portion of equity and finances the rest with debt. Debt repayment and any increase in enterprise value can boost equity returns. | Deal Capital Structure EV = $100M Equity = $20M Debt = $80M |

| 2. Debt Paydown (Deleveraging Effect) | Over time, company cash flows are used to reduce debt. As debt shrinks, equity makes up a larger share of the EV than debt. | Annual cash flow = $8M Debt repaid over 5 years = $40M Remaining debt = $40M |

| 3. Operational Improvements | The company implements disciplined cost controls, adjusts product pricing, and expands into new markets, raising its EBITDA. | Increased EBITDA raises enterprise value higher than the original $100M. |

| 3. Exit and Investor Return | At exit, the PE firm sells the company, repays remaining debt, and keeps the equity proceeds. The return depends on the growth in equity value compared with the initial investment. | Sale price (EV) = $120M Less debt = $40M Original equity = $20M Return = 4x |

By financing most of the purchase price with debt, the private equity firm only commits a small portion of equity. Instead of paying the full $100 million upfront, the firm invests $20 million of equity and borrows $80 million of debt. This small equity slice means any increase in company value has a magnified impact on the equity return. If the business grows, the debt portion stays fixed, while equity scales disproportionately.

By financing most of the purchase price with debt, the firm invests a small portion of equity, so any increase in EV disproportionately boosts equity returns.

Over time, the company’s own cash flow is used to reduce debt. As debt shrinks, the equity portion of the company automatically becomes larger, even if the enterprise value stays the same. In this example, the company generates $8 million in annual cash flow, which is used to repay debt. After five years, $40 million of the debt has been repaid, leaving $40 million outstanding.

Private equity firms also look for opportunities to improve the company’s performance during the holding period. This can include cost controls, streamlining operations, adjusting pricing, or expanding into new markets. These changes can increase EBITDA (Earnings Before Interest, Tax, Depreciation and Amortization), which can directly increase enterprise value. In the example, the leadership team makes operational improvements that enhance business performance during the holding period, supporting growth beyond the original $100 million purchase price.

Another way LBOs generate returns is through valuation multiples. If the company is sold at a higher multiple of EBITDA than it was acquired for, the exit value rises disproportionately. This shift can happen because the company is performing better, industry conditions have improved, or a strategic buyer is willing to pay more. By year five, our example company is valued at $120 million, reflecting both operational improvements and stronger market conditions.

At the end of the holding period, the PE firm sells the company and realizes the gain. In this case, the company is sold for $120 million. The remaining $40 million of debt is paid off first, leaving $80 million in equity value. Compared with the original $20 million equity investment, this represents a 4x return on equity.

Private equity firms rely on multiple deal-sourcing strategies to identify companies that could make strong leveraged buyout candidates. These approaches range from proactive outreach to participating in competitive sales processes.

Many firms build deep industry expertise and approach attractive companies directly. This often involves reaching out to founders, CEOs, or family-owned businesses that may be open to selling. Proprietary deals are highly valued because they avoid competitive auctions and can secure better terms.

Large LBOs often come through investment banks running formal sale processes. In these auctions, PE firms receive information memorandums, conduct due diligence, and submit bids alongside other buyers. While competitive, these processes provide access to sizable and established companies.

PE firms cultivate networks of executives, consultants, and lenders who surface opportunities. Some use executives-in-residence — experienced leaders who help identify and evaluate companies in their sector of expertise.

Once a PE firm acquires a “platform” company in a fragmented industry, it looks for smaller add-on acquisitions. Rolling up similar businesses allows the firm to expand scale, reduce costs, and strengthen its market position.

Large corporations often sell non-core divisions to streamline operations. Private equity firms watch for these equity carve-outs, which can be attractive LBO candidates because they often have stable cash flows but lack focus or investment under corporate ownership.

In some cases, companies or their advisors approach private equity firms directly when seeking a buyer. Well-known firms with a strong track record in certain industries are more likely to receive these inbound opportunities.

A good LBO candidate is a financially resilient business in a stable industry with clear pathways to growth and value creation. Such companies have strong company fundamentals such as stable cash flows, low existing debt, valuable assets, and opportunities for operational improvement. They also operate in industries with non-cyclical demand, recurring revenues, and room for consolidation.

Private equity firms source these opportunities through direct outreach, investment-bank-led sales processes, industry networks, add-on acquisitions, and corporate divestitures. Once acquired, returns are generated through a mix of leverage, debt paydown, operational improvements, and multiple expansion.

A good LBO candidate is a business with stable cash flows, low existing debt, valuable assets, and opportunities for operational improvement. It also operates in an industry with predictable demand and room for consolidation.

Industries with steady demand and recurring revenues often make strong LBO candidates. Examples include business services, healthcare, consumer staples, enterprise SaaS, logistics, and telecom.

Companies with little or no existing debt leave more capacity to add new leverage. This reduces financing risk and makes it easier for the company to meet debt obligations after the buyout.

Companies in non-cyclical, stable industries are better LBO candidates because their cash flows are less vulnerable to economic downturns. Cyclical sectors like airlines or commodities are riskier because volatility makes debt repayment harder.

Looking to develop your expertise in LBOs? Explore CFI’s LBO Modeling course for expert instruction in the practical skills you need to effectively model and analyze LBOs.

Demystifying Leveraged Buyout Returns