Get In-Demand Finance Certifications

A paper LBO (leveraged buyout) is a simplified version of a full LBO model that is used to quickly estimate the potential returns of a leveraged buyout transaction. While a full LBO model involves detailed financial modeling, a paper LBO focuses on key assumptions and simplified calculations. A paper LBO is done without Excel or a financial calculator, with only a pen and paper, hence the name.

A paper LBO is often used as a tool to screen prospective candidates for a role in private equity. The paper LBO requires quick decision making and using approximations of key metrics such as the Internal Rate of Return (IRR) and Multiple of Invested Capital (MOIC).

Paper LBO models may be used in a couple of different scenarios:

Regardless of the use, the goal of a paper LBO isn’t perfect accuracy but directional accuracy. In other words, is the simple analysis close enough to be generally correct?

There are obviously going to be quite a few differences between a paper LBO model and a full LBO model. Here are a few of the most significant differences:

While paper LBOs provide rough estimates, full LBO models offer the depth and accuracy necessary for final deal approval.

Learning how to quickly complete a paper LBO is pretty much a requirement for anyone pursuing a career in private equity (and investment banking). The paper LBO judges job candidates on their ability to think quickly and assess the viability of a deal in a high-stress, time-limited situation.

Successful completion of this task illustrates a solid understanding of LBO mechanics, key financial concepts, and the aptitude to work quickly under pressure. Because of the strict time constraint in completing a paper LBO, it also tests candidates on how quickly they can organize the analysis and use mental math to calculate crucial metrics.

When working through a paper LBO exercise, it’s important to remember the most important steps. The three main categories are discussed below:

This category includes all of the important transaction assumptions and financial model assumptions needed to complete the paper LBO prompt.

Transaction assumptions include the following:

a. Purchase price or purchase multiple (typically expressed as an EV/EBITDA multiple). The prompt should also specify the exit multiple, although this is often the same multiple as the purchase (or entry) multiple. There should also be an assumption about when the PE firm will exit the business, typically in five years for paper LBOs, which is what we will assume below.

b. How much debt will be used to purchase the target company (again, typically expressed as a multiple of EBITDA), as well as the interest rate on that debt.

Financial assumptions include the following:

a. Revenues and the projected revenue growth rate.

b. EBITDA margins (EBITDA as a percentage of revenue) and the income tax rate.

c. Depreciation, capital expenditures (CapEx), and net working capital requirements.

a. Sources and Uses: The sources and uses schedule illustrates where cash will come from (sources) and what the cash will be spent on (uses). The sources and uses accounts should equal each other. This schedule is also necessary to determine the amount of equity the PE firm will need to invest.

b. Income Statement: The candidate will need to complete a simplified income statement in order to properly calculate projected EBITDA and cash flows.

c. Free Cash Flow: The income statement, along with the other financial assumptions listed above, will allow candidates the ability to calculate free cash flow. The free cash flow calculation will impact the cash balance and the ultimate exit equity value. Note that the paper LBO does not include a full balance sheet: only the cash balance and debt balance is necessary for calculating the exit equity value.

d. Debt Balance Schedule: The candidate will likely also need to track the debt balance. In a full LBO, excess cash is used for debt paydown, but a paper LBO will usually simplify this. The debt balance is also important to properly calculate interest expense.

a. Exit Enterprise Value: Calculated using the final year EBITDA and the exit multiple.

b. Net Debt: The cumulative free cash flow is used to calculate the cash balance and is subtracted from the remaining debt balance to calculate net debt at exit.

c. Exit Equity Value: Calculated as the exit enterprise value minus the net debt.

Let’s now walk through a full paper LBO example, beginning with a prompt that contains the key transaction assumptions and financial model details. Even though the below screenshots are in Excel, this analysis is done with pen and paper only.

Given the assumptions below, let’s dive in.

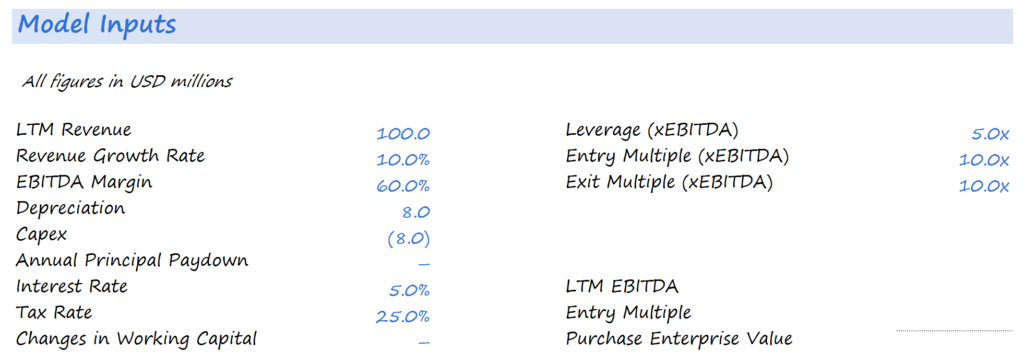

As shown below, the last twelve months (LTM) revenue is $100 million, the revenue growth rate is 10%, and the EBITDA margin is 60%. We’ve also included assumptions for depreciation, CapEx, interest rate, tax rate, and changes in working capital.

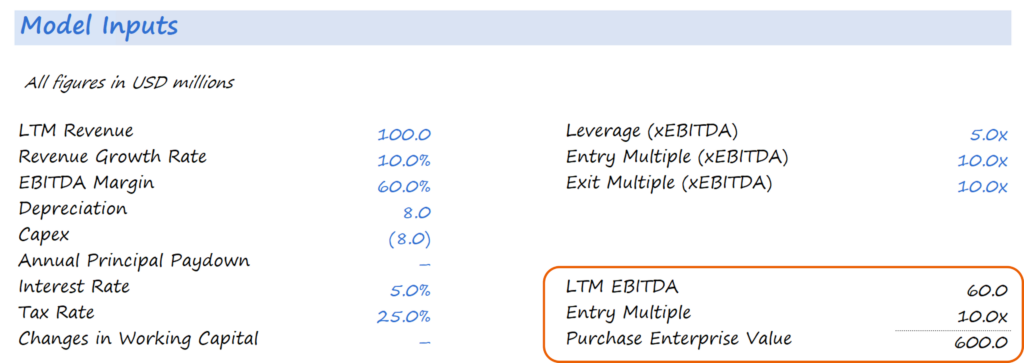

We have everything we need to calculate the purchase price (the purchase enterprise value). Since the LTM revenue is $100 million and the EBITDA margin is 60%, we can calculate the LTM EBITDA as $60 million ($100 million * 60%).

Since we are given the entry multiple of 10x EBITDA, we can then calculate the purchase enterprise value: $600 million (10 * $60 million of EBITDA), as shown below.

The purchase enterprise value is considered the actual purchase price since most acquisitions occur on what’s known as a cash-free, debt-free basis. Basically, a cash-free, debt-free deal assumes the target company has no debt (debt free) and no cash (cash free), which is effectively the same thing as the enterprise value.

When creating a Sources and Uses schedule, always begin with the uses. In this case the only use will be the purchase enterprise value. In a full LBO, there will be other uses, including transaction-related fees. However, it’s customary to exclude those in a paper LBO.

With uses complete, we can fill in the sources. Based on our financing assumptions above, the private equity firm will be able to raise debt equal to 5x EBITDA, or $300 million (5 * $60 million in EBITDA).

Since sources must equal uses, and we already know the total uses, we then backsolve for the amount of equity financing the PE firm will invest. With total uses of $600 million and $300 million in debt financing, this means the PE firm will need to invest $300 million in equity ($600 million minus $300 million in debt financing). The PE firm’s equity investment is often referred to as sponsor equity, since the PE firm is considered the “sponsor” of the LBO transaction.

It’s also customary to quote the various sources in terms of EBITDA. For example, with a $300 million equity investment, this represents 5x EBITDA ($300 million/$60 million).

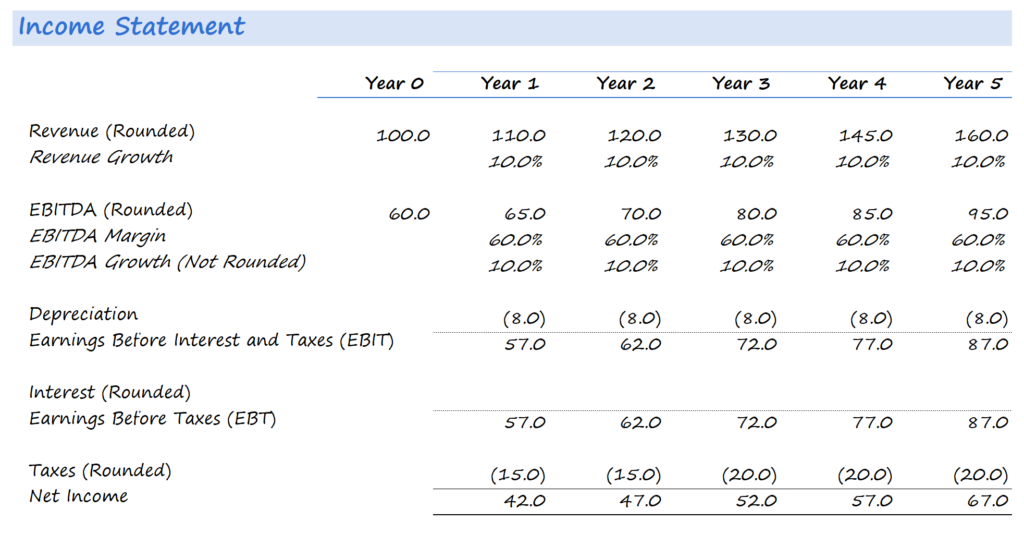

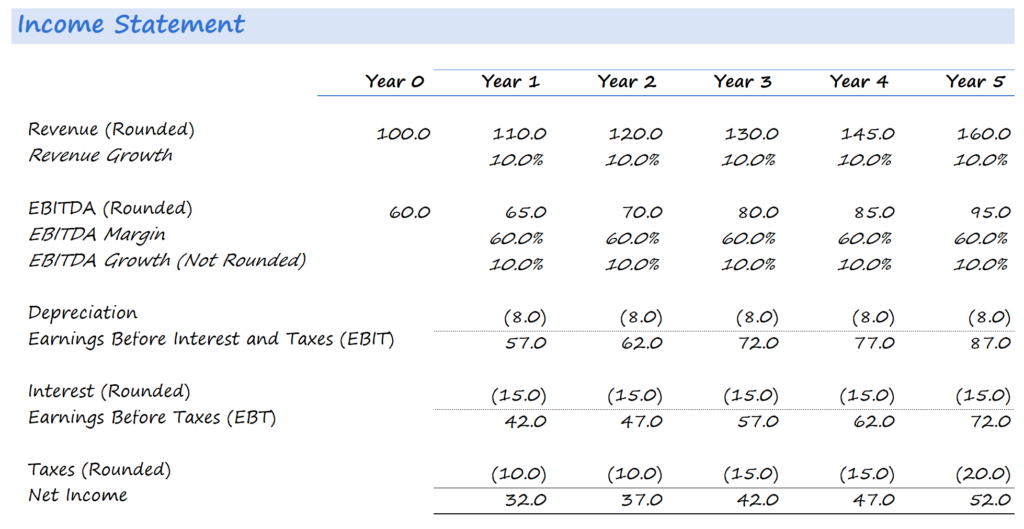

Now, we can move on and complete most of the income statement. As part of the prompt, we were given LTM revenue and the revenue growth rate. We were also given enough information to calculate the projected EBITDA.

We can then deduct depreciation of $8 million to derive EBIT. We could actually go ahead and complete interest expense, but we’ll come back to that later. Even if we leave interest expense blank at this point, we can still calculate everything else including taxes and net income.

Note that we are rounding revenue, EBITDA, and taxes… we’ll discuss this more later.

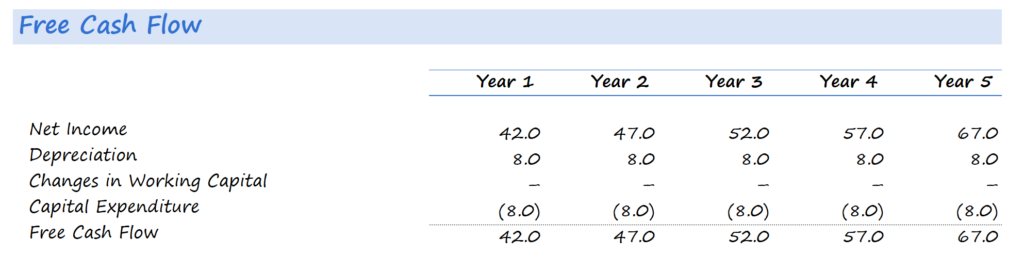

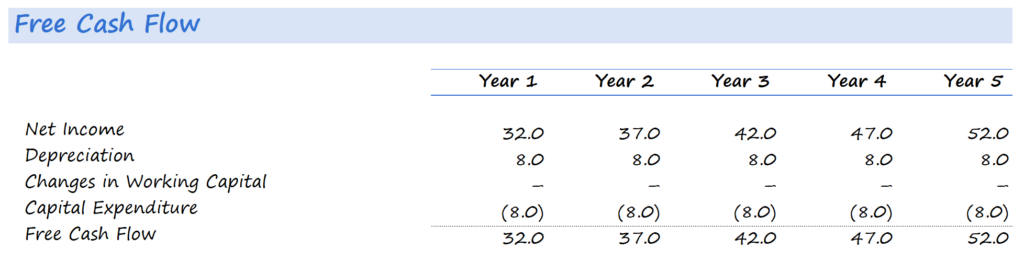

Next, we can fill in our cash flow statement or free cash flow calculation.

We begin with net income and then adjust it for any non-cash expense like depreciation. To derive cash flow, we then deduct out CapEx and factor in changes in working capital. Adding all of that together derives free cash flow. Please note that the above numbers will change when we complete the debt schedule and calculate interest expense.

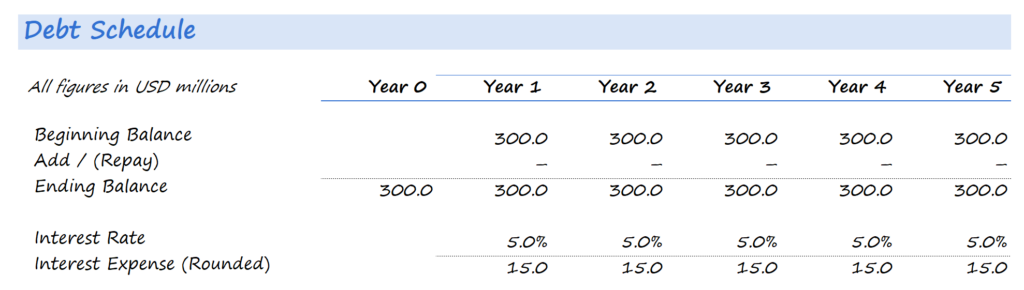

We know the paper LBO model will use $300 million in debt financing at a 5% interest rate. The prompt further assumes there will be no additional debt paydown amount (in comparison, a full LBO would assume excess cash flows would be used to pay down debt in what’s known as a cash sweep).

Since the debt balance won’t change over the forecast period, this simplifies the calculation of interest expense. At a 5% interest rate and $300 million in debt, the annual interest expense is $15 million. We can then reference the interest expense back up to the income statement, which will change our net income and cash flows to the figures shown below.

Finally, we can calculate the exit equity value and approximate the multiple of invested capital (MOIC) and the IRR. Since the prompt assumes a five-year exit, we don’t have to calculate the enterprise value, net debt, or equity value for Years 1 through 4, but we’ve gone ahead and done so for reference. Remember, it’s important to simplify this exercise and only calculate numbers you absolutely have to.

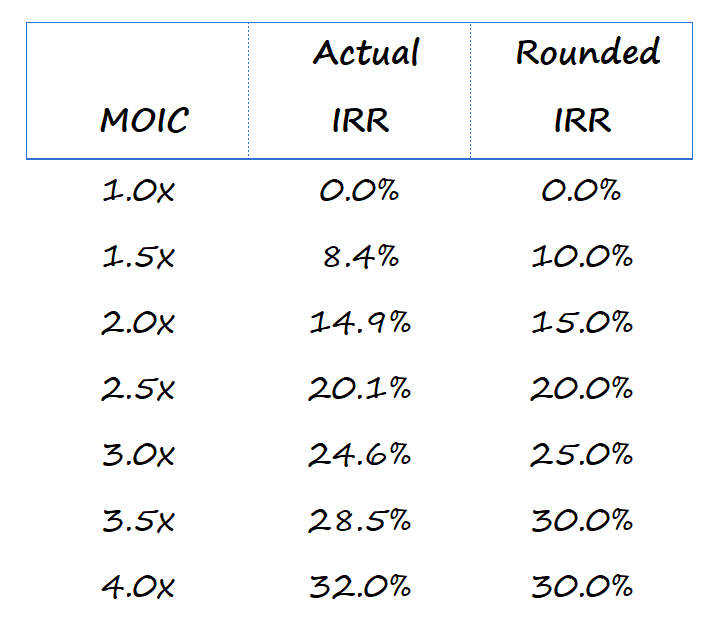

In five years, our analysis suggests an $860 million exit equity value. Since the sponsor equity investment was $300 million, this suggests an MOIC of 2.9x ($860 million/$300 million). However, the 2.9x should be rounded to 3.0x in a paper LBO.

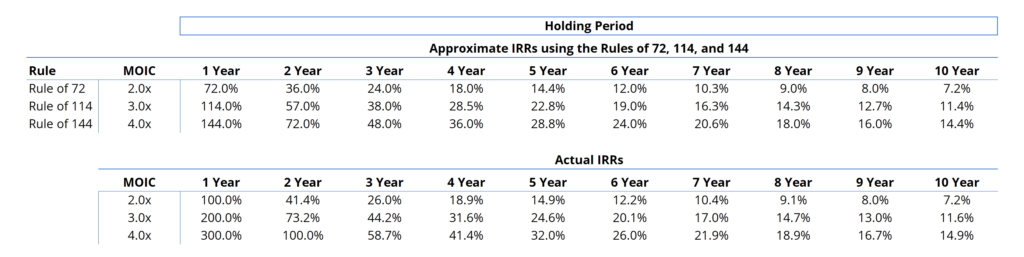

The hardest part comes with estimating the IRR that results in a 3.0x MOIC in five years. Fortunately, we can use some mental math to estimate the IRR. Since the investment triples, we can use the Rule of 114 to approximate the IRR. To do so, take 114 and divide by 5, and you get an IRR of roughly 23%, which is really close to what we calculated below. We’ll talk more about this quick math trick momentarily. For the purposes of the paper LBO, you can simply round to 25%.

Below are a few tips to successfully completing a paper LBO prompt:

To successfully and quickly complete a paper LBO, it’s important to be able to perform calculations in your head. We can use “mental math” to estimate things like revenue and EBITDA. We can then use the Rules of 72, 114, and 144 to estimate the MOIC and corresponding IRR.

When calculating financial numbers, we always want to use approximations. A key to that is being able to quickly calculate numbers based on the following increments: 10%, 5%, and 1%, since these are the most important increments for quick calculations.

For example, $100.0 million * 10% = $10.0 million (for 10%, we can shift the decimal one place to the left from $100.0 million to $10.0 million).

For a 5% calculation, we can calculate the 10% number and then divide by two: $100.0 million * 10% = $10.0 million, divide by two to get $5 million.

For a 1% calculation, we can shift the decimal two places to the left: $100.0 million * 1% = $1.0 million.

As discussed briefly above, there are a couple of tricks to solving the IRR given a MOIC. We use the following rules:

To complete the paper LBO even faster, it might not be a bad idea to memorize numbers from the below tables:

Below are a few common mistakes many applicants make when working on a paper LBO prompt:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on Paper LBOs. To keep advancing your career and skills, the following CFI resources will be useful: