Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The offer price in M&A is the per-share amount a buyer is willing to pay to acquire a target company. It represents the buyer’s view of the company’s value and is usually compared against the target’s current market price. When the offer price is higher than the market price, the difference is called the takeover (or control) premium.

In most deals, the offer price reflects not only the company’s standalone value but also the potential benefits the buyer expects to gain from the acquisition. Shareholders of the target look closely at the offer price when deciding whether to approve the transaction.

The offer price in M&A is influenced by valuation, synergies, market conditions, buyer type, and negotiation dynamics.

Buyers typically begin with standard valuation methods, including comparable company analysis, precedent transaction analysis, and discounted cash flow (DCF) modeling. These methods provide a reference range for the company’s worth, though the final offer often reflects adjustments beyond pure financial modeling and valuation.

Expected cost savings or revenue opportunities from combining businesses can justify a higher offer price. Strategic buyers, in particular, may account for efficiencies in operations, expanded customer reach, or cross-selling potential when determining what they are willing to pay.

The broader financing and economic environment plays a role. Strong equity markets and low interest rates make higher offers easier to justify, while tight credit conditions or market uncertainty often limit how aggressively buyers are willing to bid.

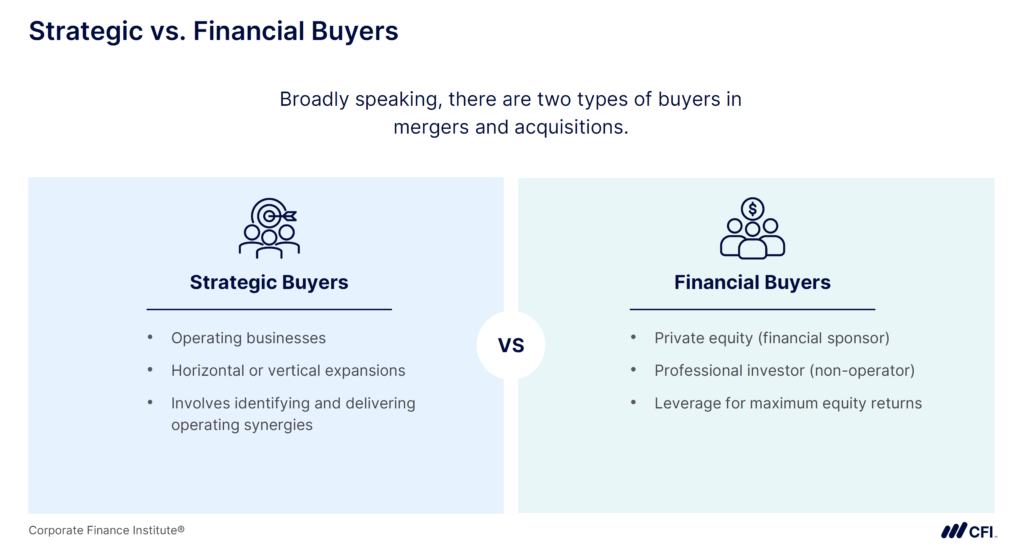

Strategic buyers are usually operating companies. They are often willing to make higher bids for acquisitions because they can integrate the target into existing operations and realize synergies. Strategic buyers are usually large and well-established companies with easier access to capital.

Financial buyers (private equity or investment firms) view acquisitions as investments. They are looking to invest up to a certain amount of money in acquiring the target company, and then expect that investment to generate a satisfactory return.

Buyers determine a final offer price after they secure financing and negotiate with the target company’s board of directors and shareholders. Competitive bidding can drive up offer prices, but even in single-buyer situations, sellers push for higher prices to provide more value to shareholders and gain their support for the deal.

To persuade shareholders to sell, buyers usually offer more than the company’s current share price. This control premium often falls in the 20% to 30% range above the unaffected share price, though it can be higher or lower depending on the company’s prospects, competitive tension, and market environment.

In mergers and acquisitions of public companies, the total equity purchase price (often just called the “offer price” or equity value of the deal) is calculated by multiplying the per-share offer price by the target’s fully diluted shares outstanding.

Offer Price = Offer Price per Share × Fully Diluted Shares Outstanding (FDSO)

Where:

Real-world M&A announcements regularly use this per-share method for offer prices. The offer is often quoted as a price per share along with the implied total equity value. For instance, in June 2024, Altaris agreed to acquire Sharecare for $1.43 per share in cash, “implying a total equity value of approximately $540 million.”

Another common way to arrive at an offer price is by applying a purchase multiple to the target’s financial metrics (rather than starting with an explicit per-share quote).

In practice, acquirers often determine a target price based on a multiple of EBITDA, earnings, or other metrics, derived from comparable deals or desired returns.

Offer Price = Purchase Multiple × LTM EBITDA

Where:

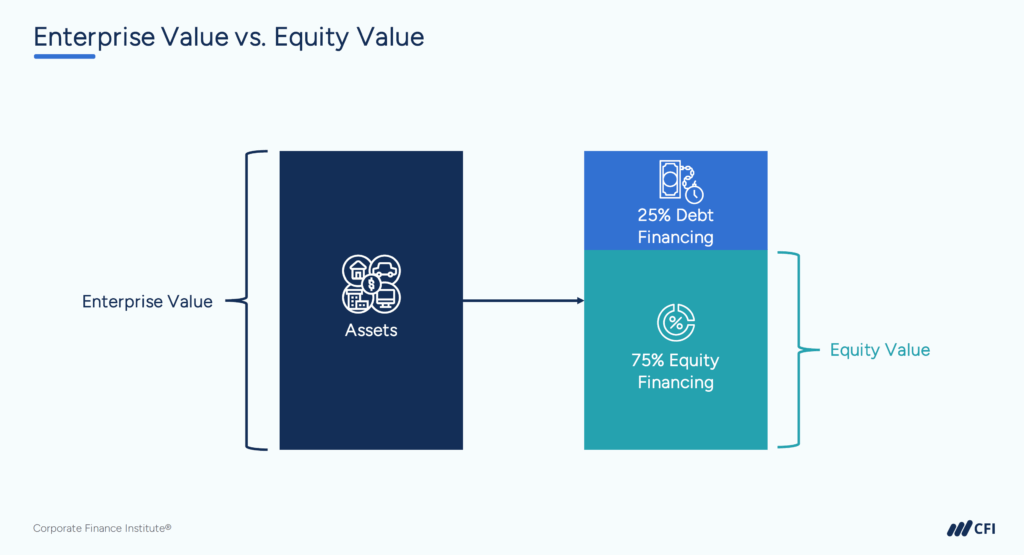

In this approach, the offer price is equal to the transaction value, or total enterprise value (EV). Enterprise value is a measure of the entire business, including all ownership interests and asset claims from both debt and equity.

For example, a buyer might decide to pay 10x LTM EBITDA for a company. If the target’s EBITDA is $100M, this implies an enterprise value of $1.0 billion. This figure would then be adjusted for debt, cash, etc., to arrive at the equity purchase price. This equity value is what’s left for shareholders after debts or other claims are accounted for.

An acquisition premium is the amount a buyer offers above the target company’s current market value. The current market value is also called the unaffected share price because it reflects the share price before any public announcement is made.

Acquisition premium is also known as the control premium or takeover premium because it represents the price of gaining control of the company.

The acquisition premium is calculated as a percentage:

Acquisition Premium (%) = (Offer Price per Share / Current “Unaffected” Share Price) − 1

Example: If a company’s stock trades at $40 per share and the acquirer offers $50 per share, the premium is 25% (50 / 40 – 1) = 25%.

Acquisition premiums vary widely depending on market conditions, industry competition, and expected synergies. In many public company deals, they often fall in the 20% to 30% range, though they can be higher when several bidders compete for the same target.

The acquisition premium matters because it:

The offer price in M&A is the per-share amount a buyer is willing to pay, usually set above market value with an acquisition premium. It reflects both financial analysis and strategic considerations, making it the central figure that determines whether a deal moves forward.

Offer price represents the value a buyer is willing to pay to acquire a company’s equity. The offer price can be expressed as a per-share amount multiplied by fully diluted shares outstanding, or as a total transaction value based on a purchase multiple (such as an EBITDA multiple).

Valuation methods, expected synergies, market conditions, buyer type, and negotiation dynamics all play a role in shaping the offer price.

The acquisition premium is calculated as the offer price per share divided by the unaffected share price, minus one.

Learning valuation means developing the ability to analyze financial data, build models, and interpret market trends to make informed business decisions.

The most effective way to build valuation expertise? Structured courses, hands-on case studies, and guided practice. Earning a CFI Financial Modeling & Valuation Analyst (FMVA®) Certification equips you with in-depth valuation skills, hands-on financial modeling experience, and practical case studies to enhance your expertise.

Fully Diluted Shares Outstanding (FDSO)