Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

ROCE (Return on Capital Employed) represents how much profit a company makes for each dollar of capital employed in the business. ROA (Return on Assets) indicates how well a company uses its total assets to drive profit.

ROCE and ROA are both profitability ratios that provide different perspectives on how well a company uses its resources to generate earnings.

Return on Capital Employed (ROCE) is a financial ratio that measures how effectively a business is driving operating profit from the capital invested in it. A firm’s ROCE should ideally exceed its cost of capital to create value over the long term.

For example, a ROCE of 20% means the company generated $0.20 in operating profit for every $1 of capital used. Higher percentages indicate the company is doing a better job turning its capital into profits. It’s essentially the percentage return the company earns on all the money at its disposal (both equity and debt).

A high ROCE (relative to industry peers or to the company’s own history) means the business generates a strong profit for each dollar of capital employed. A low or declining ROCE can be a red flag. If ROCE is volatile or trending downward over time, it suggests the company’s profitability on its capital is worsening.

A company’s ROCE is calculated by dividing its operating profit, or EBIT, by capital employed.

ROCE = EBIT / Capital Employed

Where:

The ROCE formula uses EBIT (Earnings Before Interest and Taxes) instead of net income, since EBIT reflects operating performance without being affected by capital structure.

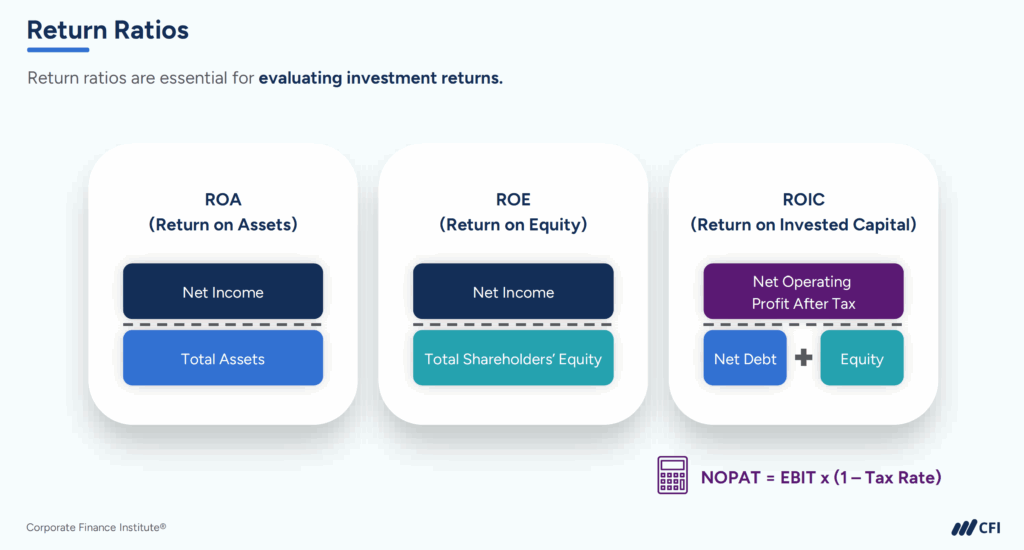

Return on assets (ROA) is a profitability ratio that indicates how profitable a company is relative to its total assets. In other words, it measures how well a company uses what it owns to drive profit. ROA answers the question: “For every dollar of assets the company has, how much profit does it generate?”

Suppose a lemonade stand and a café both earn $1,000 profit. If the café owns far more assets (building, equipment, etc.), the lemonade stand would have a much higher ROA because it earned the same profit with fewer resources.

A high ROA is generally a sign that a company is generating strong profits relative to its asset base, implying that management is using the company’s resources effectively to produce earnings.

A low ROA suggests that a company’s assets are not being put to productive use, or the company might have significant investments in assets that are yielding only modest returns. This could be due to inefficiencies or problems, such as a cost structure that is too high or over-investment in facilities or equipment that isn’t generating enough revenue.

A company’s ROA is calculated by dividing its net income by total assets.

ROA = Net Income / Total Assets

Where:

Take your analysis skills to the next level with CFI’s free guide to financial ratios and strengthen your ability to assess a company’s financial health. Download now!

The difference between ROCE and ROA comes down to capital vs. assets. ROCE tells you how well a company is using all the money invested in the business to generate operating profit, whereas ROA tells you how well a company is using everything the company owns to generate net profit.

ROCE considers all sources of capital (shareholders’ equity and borrowed funds), making it especially useful for companies that use a lot of debt financing. ROA, by contrast, ignores whether assets are funded by debt or equity and simply looks at how profitable the company is relative to its total assets.

| Ratio Type | Profitability and financial efficiency | Profitability and financial efficiency |

| What It Measures | How well a company employs its capital to generate operating profit | How well a company uses its total assets to generate net income |

| How It’s Calculated | Divide EBIT by capital employed | Divide net income by total assets |

| Interpretation | Amount of operating profit generated per $1 of capital employed | Amount of net income earned for every $1 invested in assets |

Both metrics ultimately complement each other: ROCE gives a more comprehensive view of profitability by including debt funding, and ROA provides a clear view of asset efficiency. An analyst will often examine both to get a fuller picture of a company’s performance.

Both ROCE and ROA are useful for comparing a company to its peers, as long as the comparisons are made on a like-for-like basis. In practice, this means these ratios are most insightful when comparing companies in the same industry (or sector) and with similar business models or asset profiles.

Within a peer group, such as a set of competing retailers, ROCE and ROA can highlight which company is managing its capital and assets more effectively to generate profits.

ROCE is particularly useful for comparing companies within the same industry, especially in capital-intensive sectors (like utilities, telecoms, or manufacturing). ROA can highlight how asset-intensive a business is.

However, it’s important to note that ROCE and ROA are not well-suited for cross-industry comparisons. Different industries have inherently different capital requirements and asset turnovers, so a “good” ROA or ROCE in one sector might be poor in another. Stick to peer groups and industry-specific analysis to get meaningful insights from these ratios.

Profitability ratios help investors assess a company’s ability to generate returns relative to the resources it uses. As with any financial ratio, calculating only the ROCE or ROA of a company is not enough to fully understand its profitability. Other profitability ratios should be used in conjunction with ROCE and ROA, such as:

Used alongside ROCE and ROA, these ratios give investors a more complete view of a company’s profitability — and its ability to sustain it.

Return on Capital Employed (ROCE) and Return on Assets (ROA) are both profitability ratios that help investors and analysts understand how efficiently a company uses its resources to generate earnings. ROCE evaluates how effectively a company generates operating profit from equity and debt used in the business. In contrast, ROA looks at how efficiently a company uses its total assets to produce net income.

CFI’s Financial Analysis Fundamentals course covers financial ratios in depth, including ratios for profitability, asset utilization, leverage, and liquidity. You’ll learn how to conduct a comprehensive financial evaluation of any organization and best practices for presenting your findings in Excel.

Explore Financial Analysis Fundamentals!

No. ROCE and ROA measure different things. ROCE measures profitability relative to capital employed, while ROA measures profitability relative to total assets.

Use ROCE when you’re evaluating returns on all capital invested, not just assets. Use ROA when you’re assessing how well a company uses its total assets to produce bottom-line profit.

ROCE includes both equity and debt (capital employed), whereas ROA does not include financing, whether through equity or debt. ROA focuses strictly on how efficiently a company uses all its assets to generate profit after interest and taxes.

Financial Ratios Definitive Guide

Analysis of Financial Statements