Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A measure of how efficiently a company uses its capital

Return on Capital Employed (ROCE), a profitability ratio, measures how efficiently a company is using its capital to generate profits. The return on capital employed metric is considered one of the best profitability ratios and is commonly used by investors to determine whether a company is suitable to invest in or not.

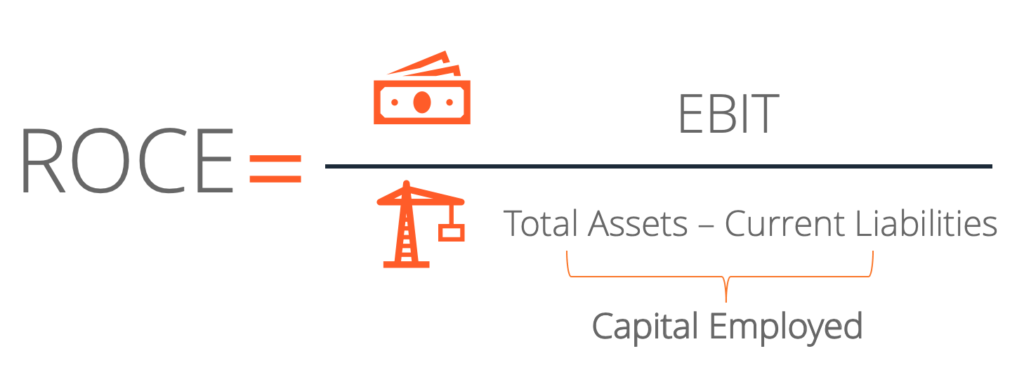

The formula for computing ROCE is as follows:

Where:

Some analysts use net operating profit instead of earnings before interest and taxes when calculating return on capital employed.

Let us compute the return on capital employed for Apple Inc. We will look at the financial statements of Apple for 2016 and 2017 and calculate the ROCE for each year.

The following information is taken from Apple’s financial statements:

Apple’s capital employed is calculated as total assets minus total current liabilities:

Therefore:

The returns on capital employed for Apple Inc. for 2016 and 2017 are as follows:

Click the button below to download CFI’s free ROCE template!

The return on capital employed shows how much operating income is generated for each dollar of capital invested. A higher ROCE is always more favorable, as it indicates that more profits are generated per dollar of capital employed.

However, as with any other financial ratios, calculating just the ROCE of a company is not enough. Other profitability ratios, such as return on assets, return on invested capital, and return on equity, should be used in conjunction with ROCE to determine whether a company is likely a good investment or not.

In the example of Apple Inc., a 23% ROCE in 2017 means that for every dollar invested in capital, the company generated 23 cents in operating income. To determine whether Apple’s ROCE is good, it is important to compare it against its competitors and not across different industries.

When comparing ROCE among companies, there are key things to keep in mind:

Here are the key takeaways on return on capital employed:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Return on Capital Employed (ROCE). To keep learning and advancing your career, the following CFI resources will be helpful: