Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

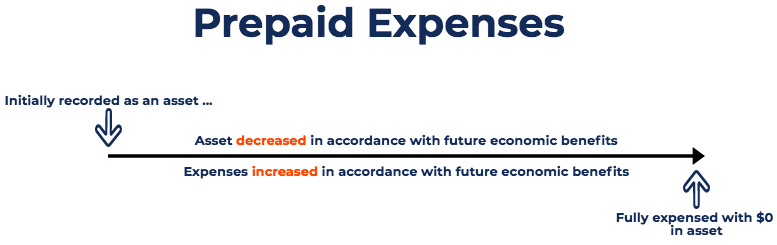

Future expenses that are paid in advance

Prepaid expenses represent expenditures that have not yet been recorded by a company as an expense, but have been paid for in advance. In other words, prepaid expenses are expenditures paid in one accounting period, but will not be recognized until a later accounting period.

Prepaid expenses are initially recorded as assets because they have future economic benefits and are expensed when those benefits are realized (the matching principle).

The two most common uses of prepaid expenses are rent and insurance.

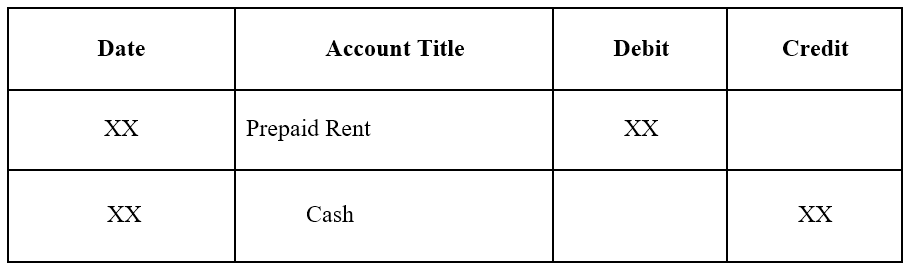

1. Prepaid rent is rent paid in advance of the rental period. The journal entries for prepaid rent are as follows:

Initial journal entry for prepaid rent:

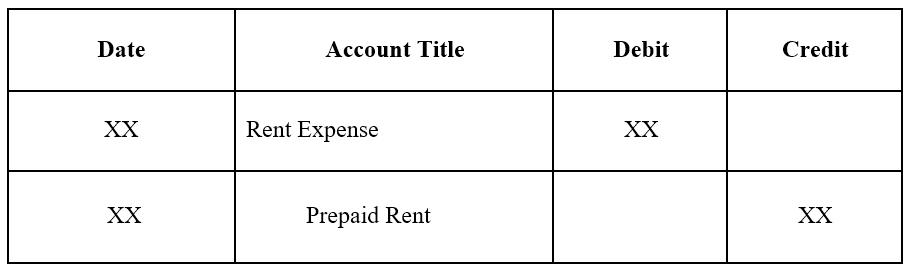

Adjusting journal entry as the prepaid rent expires:

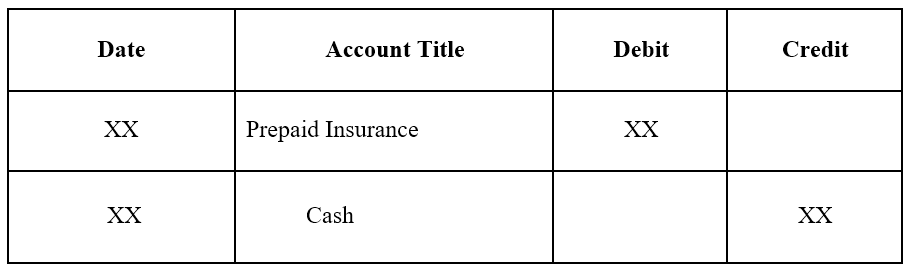

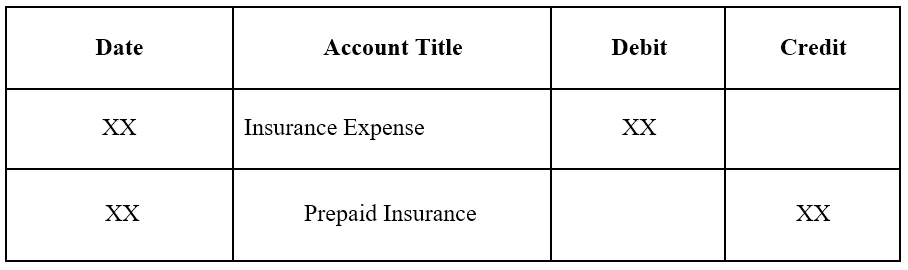

2. Prepaid insurance is insurance paid in advance and that has not yet expired on the date of the balance sheet.

Initial journal entry for prepaid insurance:

Adjusting journal entry as the prepaid insurance expires:

We will look at two examples of prepaid expenses:

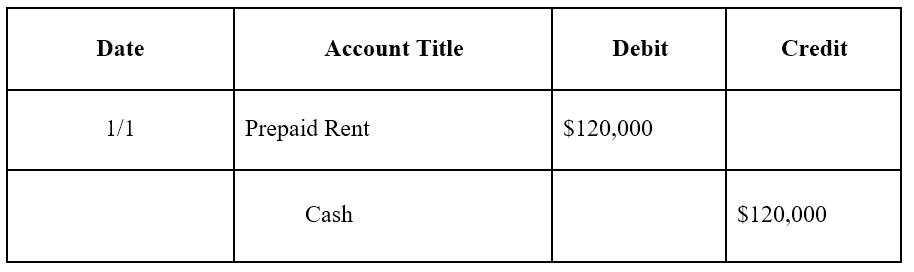

Company A signs a one-year lease on a warehouse for $10,000 a month. The landlord requires that Company A pays the annual amount ($120,000) upfront at the beginning of the year.

The initial journal entry for Company A would be as follows:

At the end of one month, Company A would’ve used up one month of its lease agreement. Therefore, prepaid rent must be adjusted:

Note: One month corresponds to $10,000 ($120,000 x 1/12) in rent.

The adjusting journal entry is done each month, and at the end of the year, when the lease agreement has no future economic benefits, the prepaid rent balance would be 0.

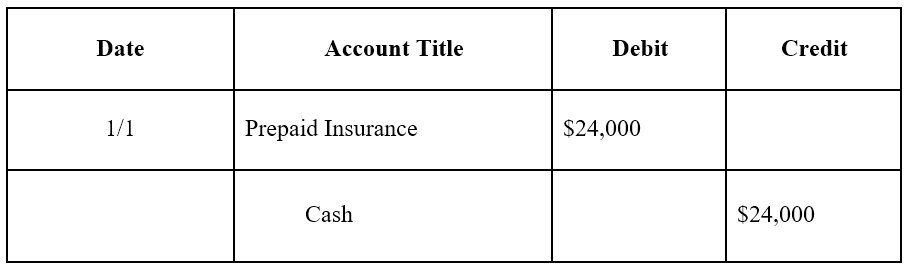

Upon signing the one-year lease agreement for the warehouse, the company also purchases insurance for the warehouse. The company pays $24,000 in cash upfront for a 12-month insurance policy for the warehouse.

The initial journal entry for Company A would be as follows:

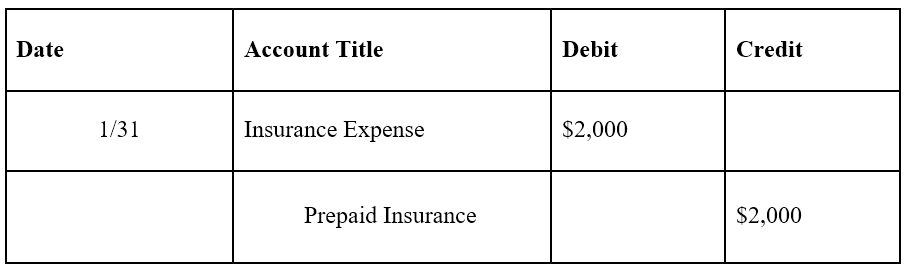

At the end of one month, Company A would have used up one month of its insurance policy. Therefore, prepaid insurance must be adjusted:

Note: One month corresponds to $2,000 ($24,000 x 1/12) in insurance policy.

The adjusting journal entry is done each month, and at the end of the year, when the insurance policy has no future economic benefits, the prepaid insurance balance would be 0.

The initial journal entry for a prepaid expense does not affect a company’s financial statements. For example, refer to the first example of prepaid rent. The initial journal entry for prepaid rent is a debit to prepaid rent and a credit to cash.

These are both asset accounts and do not increase or decrease a company’s balance sheet. Recall that prepaid expenses are considered an asset because they provide future economic benefits to the company.

The adjusting journal entry for a prepaid expense, however, does affect both a company’s income statement and balance sheet. Refer to the first example of prepaid rent. The adjusting entry on January 31 would result in an expense of $10,000 (rent expense) and a decrease in assets of $10,000 (prepaid rent).

The expense would show up on the income statement, while the decrease in prepaid rent of $10,000 would reduce the assets on the balance sheet by $10,000.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.