Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The payment of cash or incurrence of liability in exchange for goods or services

An expenditure represents a payment with either cash or credit to purchase goods or services. It is recorded at a single point in time (the time of purchase), compared to an expense that is recorded in a period where it has been used up or expired. This guide will review the different types of expenditures used in accounting and finance.

To record the occurrence of an expenditure, an accountant must show evidence of the transaction occurring. For instance, a sales receipt will show proof of an over-the-counter sale, while an invoice will indicate a request for payment for goods and services. The documents exist to enable organizations to maintain tight control over their transactions. Usually, the goal is to anticipate profits and losses while still keeping track of revenues.

It’s important to understand the difference between an expenditure and an expense. Though related, they’re actually different and have some important nuances you must know about.

Expenditure – This is the total purchase price of a good or service. For example, a company buys a $10 million piece of equipment that it estimates to have a useful life of 5 years. This would be classified as a $10 million capital expenditure.

Expense – This is the amount that is recorded as an offset to revenues or income on a company’s income statement. For example, the same $10 million piece of equipment with a 5-year life has a depreciation expense of $2 million each year.

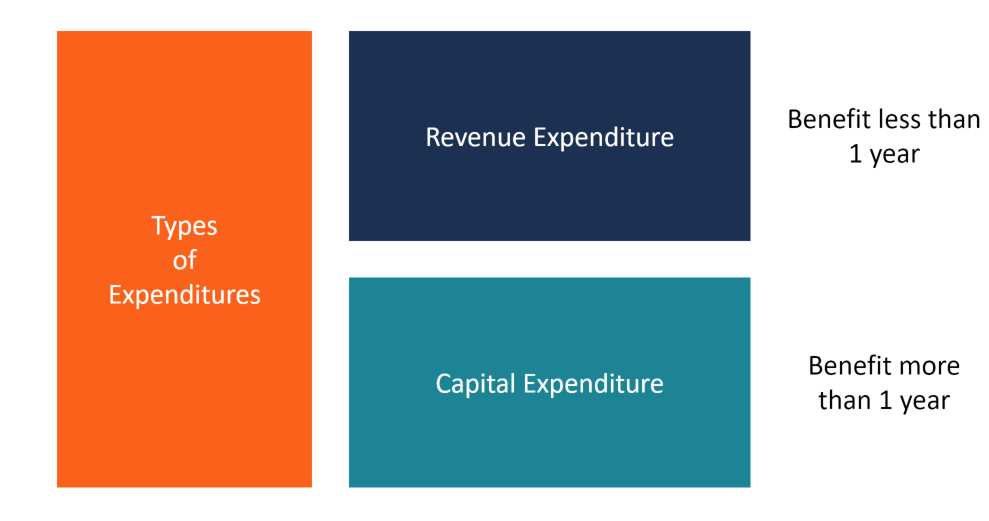

Expenditures in accounting comprise two broad categories: capital expenditures and revenue expenditures.

A company incurs a capital expenditure (CapEx) when it purchases an asset with a useful life of more than one year (a non-current asset).

In many cases, it may be a significant business expansion or an acquisition of a new asset with the hope of generating more revenues in the long run. Such an asset, therefore, requires a substantial amount of initial investment and continuous maintenance after that to keep it fully functional. As a result, many companies often finance the project using either debt financing or equity financing.

Because the investment is a capital expenditure, the benefits to the business will come over several years. As a consequence, it cannot deduct the full cost of the asset in the same financial year. Therefore, it spreads these deductions over the useful life of the asset. The value of this asset will be shown on the balance sheet, under non-current assets, as part of plant, property, and equipment (PP&E).

Example

Let’s say Company Y deals with iron sheet manufacturing. Due to the increase in demand for its high-profiled iron sheets, the company executives decide to buy a new minting machine to revamp production. They estimate the new machine will be able to improve production by 35%, thus closing the gap in the demanding market. Company Y decides to acquire the equipment at the cost of $100 million. The useful life of the machine is expected to be 10 years.

In this case, it is evident that the benefit of acquiring the machine will be greater than one year, so a capital expenditure is incurred. Over time, the company will depreciate the machine as an expense (depreciation).

A revenue expenditure occurs when a company spends money on a short-term benefit (i.e., less than one year). Typically, these expenditures are used to fund ongoing operations – which, when they are expensed, are known as operating expenses. It is not until the expenditure is recorded as an expense that income is impacted.

CapEx is related to long-term spending – a major investment – while revenue expenditure is related to short-term operating expenses. They are both recorded in the same financial year as they are incurred and cannot be forwarded to the next financial year.

Example

After the purchase of the minting machine, the company may decide to hire a new lead engineer together with seven other technicians to run the new machine. A fundamental role of this team will be keeping the equipment running throughout the production cycle. Other secondary tasks may include the installation of new parts, monitoring production, and continuous maintenance.

The salary costs of the engineer and technicians is considered a revenue expenditure.

Deferred revenue expenditure, or deferred expense, refer to an advance payment for goods or services. This is an advanced form of prepaid expenses. The arrangement is usually an agreement that the company will receive a service or goods in the future – but it pays for the goods or services in advance.

As a result, the company treats the transaction as an asset until it receives all the benefits of the purchase. In the books of accounts, the arrangement doesn’t affect the business’ profitability because the company is yet to acquire the asset and does not yet receive the benefits of the asset. The company charges the outcome of the transaction to the profit or loss account over a given timeframe.

Example

Let’s assume that Joe specializes in the manufacturing of refrigerators. A part of his production inputs ship from overseas. Due to the sensitive nature of the production, Joe needs a consistent, high-quality, dependable supplier of raw materials. So, he reaches out to his distributor X, who supplies him with condensers and compressors. However, Joe needs to pre-pay for the goods. Also, according to the terms, he must wait for his supplies for three years.

In such a case, Joe pays for his supply in advance. In his books of accounts, he will declare the arrangement as a deferred payment until he receives his shipment. Clearly, in accounting, the financial settlement is recorded as an asset.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide to Expenditure. To keep advancing your career, these additional CFI resources will be useful: