Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Accrued expenses and accounts payable are both liabilities, meaning money a company owes. The key difference is whether the company has received a bill.

Accrued expenses are costs a company has already incurred but they haven’t received an invoice for those costs yet. Once the company receives the invoice, those costs become accounts payable, meaning the invoice arrived and was recorded, but the company hasn’t paid it yet.

This guide breaks down how each concept works in practice.

Accrued expenses are costs a company has already incurred but hasn’t yet paid for because the bill hasn’t arrived. Under the accrual method of accounting, these expenses are recorded when a company receives goods or services, not when it pays for them.

Companies typically accrue expenses for utilities, wages, interest, and taxes. Here are two practical examples that show how the process works.

A company uses electricity to power its office throughout the month of June, but the utility bill doesn’t arrive by the time it closes its books on June 30. Based on past usage, the company expects the bill to be $1,200.

Since the electricity has already been used, the company records the cost in June, even without the invoice.

Journal Entry on June 30:

| Account | Debit | Credit |

| Utilities Expense | $1,200 | |

| Accrued Expense | $1,200 |

This entry records the estimated expense and creates a liability (accrued expense) for the amount the company expects to pay.

When the utility bill arrives on July 10, the company confirms the amount. If it pays the bill on July 25, the payment is recorded as:

Journal Entry on July 25:

| Account | Debit | Credit |

| Accrued Expense | $1,200 | |

| Cash | $1,200 |

This clears the accrued expense liability and reflects the payment.

Consider a company that pays employees bi-weekly. The pay period ends on June 28, but payday isn’t until July 5. The company has incurred $15,000 in wages for work performed during this period.

Since employees have already earned these wages, the company must record the expense in June even though the payment won’t happen until July.

Journal Entry on June 30:

| Account | Debit | Credit |

| Wages Expense | $15,000 | |

| Accrued Expense | $15,000 |

This entry records the wages expense for work already performed and creates a liability for the amount the company owes to employees.

When the company pays employees on July 5, the payment is recorded as:

Journal Entry on July 5:

| Account | Debit | Credit |

| Accrued Expense | $15,000 | |

| Cash | $15,000 |

This clears the liability and reflects the cash payment to employees.

Accounts payable represents the money a company owes after receiving an invoice for goods or services. It’s the formal record of bills the company has received but hasn’t paid yet.

Unlike accrued expenses, there’s no estimation involved. The company has the invoice in hand, confirming the exact amount owed.

A company orders and receives a shipment of office supplies on June 25. The supplier includes an invoice for $500, due in 30 days.

Because the supplies have been received and the invoice confirms the cost, the company records the expense and the liability right away.

Journal Entry on June 25:

| Account | Debit | Credit |

| Office Supplies Expense | $500 | |

| Accounts Payable | $500 |

When the company pays the bill 25 days later on July 20, the journal entry is:

Journal Entry on July 20:

| Account | Debit | Credit |

| Accounts Payable | $500 | |

| Cash | $500 |

This reflects the full process: the company received the invoice, recorded the liability, and then paid it. The expense appears in June when the supplies were received, and the cash flows out in July when the payment is made.

Both accrued expenses and accounts payable impact a company’s financial statements in similar ways, since they’re both current liabilities representing unpaid costs.

In the current liabilities section of the balance sheet, accrued expenses may appear as their own line item or they might appear under “Accrued Liabilities.” Accounts payable usually appears as its own line item. The key difference is documentation: accounts payable has invoice backup, while accrued expenses are based on estimates.

Both record expenses in the period when goods or services are received. Whether it’s electricity used (accrued) or office supplies delivered (accounts payable), the expense hits the income statement right away, not when it’s paid.

On the cash flow statement, increases in both accrued liabilities and accounts payable are added back to net income in the operating activities section. This adjustment reflects expenses that reduced net income but haven’t yet required a cash payment.

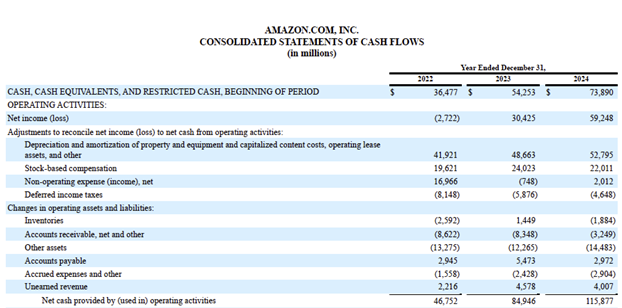

Amazon’s 2024 cash flow statement (which Amazon formally titles ‘Consolidated Statements of Cash Flows’) is provided below. Notice how they’ve organized accounts payable and accrued expenses as separate line items in the operating activities section. Both were added back to net income, so that net cash from operations reflects these expenses.

Here’s a simple comparison of the timing and process behind accrued expenses and accounts payable.

| Invoice received? | No | Yes |

| Expense status | Already incurred (used the service) | Already incurred and billed |

| Common examples | Utilities used but not billed, interest owed, unpaid taxes | Supplier invoices, rent bills, consulting fees |

| When it’s recorded | At the end of the period, based on estimate or expectation | When an invoice is received |

| Balance sheet account | Accrued liabilities or accrued expenses | Accounts payable |

The timing of expense recognition directly affects the accuracy of financial statements. If a company fails to record an accrued expense, its profits may appear higher than they actually are. That’s because the cost was incurred during the period but was never included in the reported expenses.

On the other hand, if accounts payable aren’t recorded properly, the company may appear to have more cash on hand than it truly does since the obligation to pay hasn’t been reflected.

Distinguishing between these two liabilities is part of applying accrual accounting correctly. It also ensures that the balance sheet, income statement, and cash flow statement work together to reflect the company’s financial position at the end of the reporting period.

Accrued expenses and accounts payable are both current liabilities recorded on the balance sheet, but they differ in timing and documentation. Accrued expenses are costs that have been incurred but not yet invoiced, while accounts payable are obligations for which an invoice has been received.

Recognizing the distinction between these two is crucial for accurate financial reporting and effective cash flow management. Misclassifying them can lead to inaccurate financial statements and faulty decision-making.

Ready to deepen your understanding of financial accounting? Explore CFI’s Accounting for Financial Analysts Specialization to strengthen your expertise in the accounting behind financial statements and level up your financial analyses.