Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Two companies report the same net income. But one has cash to grow, and the other is borrowing to stay afloat. Why?

If you’ve ever assessed financial health using just the income statement, you’ve likely seen this disconnect. Cash flow and net income both measure performance, but they tell very different stories. Understanding how they differ — and connect — is key to analyzing profitability, sustainability, and value.

This guide unpacks the differences between cash flow vs net income and how analysts use both metrics to evaluate a company’s financial health.

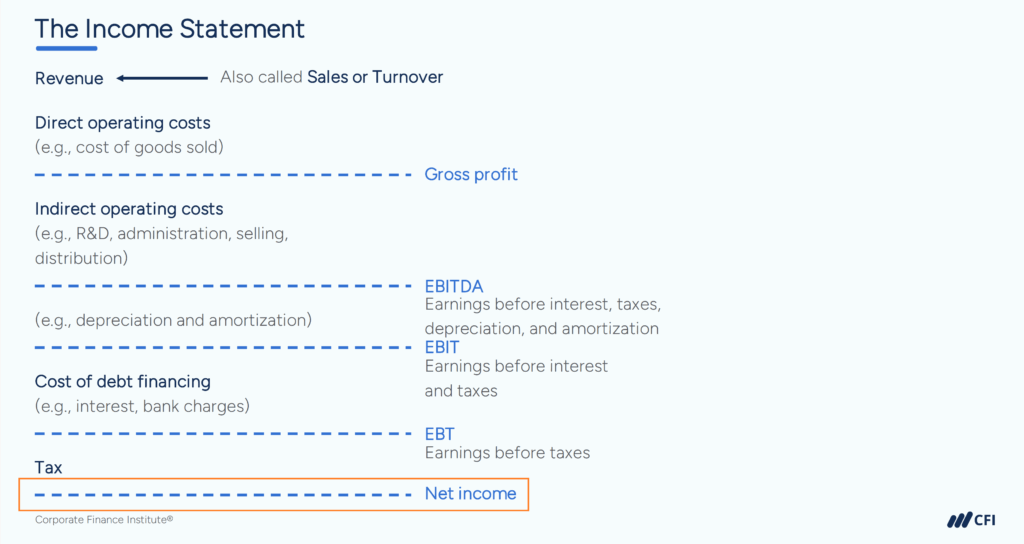

Net income is profit after all expenses — the “bottom line” of the income statement. It’s calculated by subtracting costs of goods sold (COGS), selling, general & administrative expenses (SG&A), depreciation and amortization, interest expense, taxes, and any other expenses from total revenue.

Cash flow tracks cash going in and out of a business. It’s reported in the cash flow statement, broken into three categories:

To compare cash flow vs net income, analysts focus on operating cash flow, which reflects whether a company’s daily operations generate enough cash to sustain the business.

Net income and cash flow both measure performance, but they are calculated differently, appear in separate statements, and serve different purposes.

Here’s a quick side-by-side comparison:

| What It Measures | Profit | Cash inflows and outflows |

| Where to Find It | Income Statement | Cash Flow Statement |

| Accounting Basis | Accrual-based | Cash-based |

| Starting Point | Revenue | Net income |

| Ending Point | Net income | Cash balance (for the period)* |

*Note: The cash balance becomes the starting point of the balance sheet.

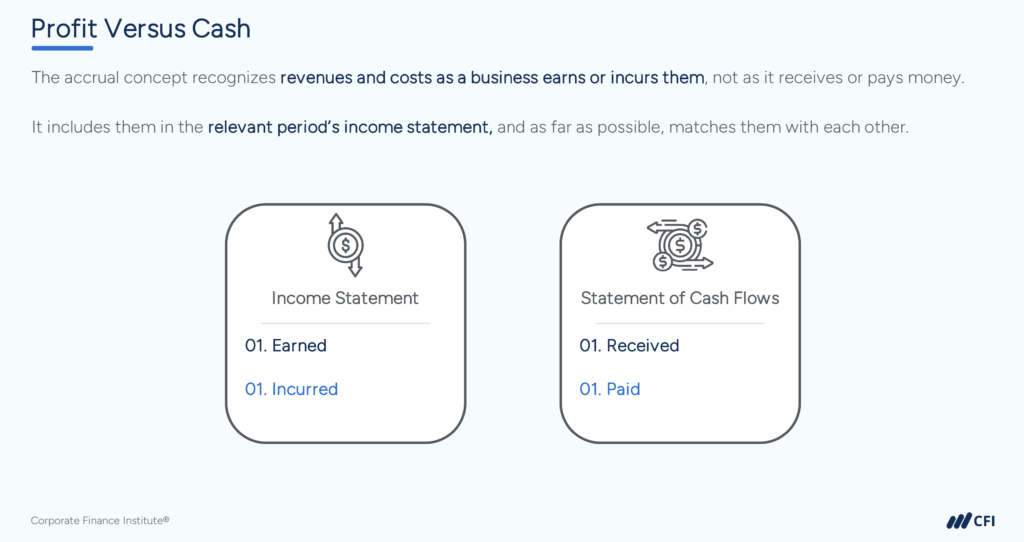

Net income follows accrual accounting — revenue is recorded when earned, not when cash is received. Likewise, expenses are recorded when incurred, not when paid. This means a company can report profits without having received payment or show a loss while still collecting cash.

Cash flow adjusts net income by removing non-cash items and factoring in changes in various accounts on the balance sheet (e.g., working capital). It shows how much actual cash was generated or used during the period.

Non-Cash Expenses and Timing

Some expenses, like depreciation or stock-based compensation, reduce net income but don’t involve cash leaving the business. When calculating operating cash flow, companies add these back to net income to reflect actual cash generated.

Timing differences also matter. If a company sells on credit, revenue is recorded immediately, even if cash arrives weeks later. That sale boosts net income — but doesn’t appear in cash flow until collected.

Cash flow also adjusts for changes in working capital — like accounts receivable, accounts payable, and inventory. These shifts explain many of the differences between net income and cash flow and are part of the reconciliation process between net income and cash flow.

Net income and cash flow aren’t just two separate metrics. They’re directly linked through the operating section of the cash flow statement.

Most companies use the indirect accounting method to calculate operating cash flow. This approach starts with net income and then adjusts it for items that impacted profit but didn’t involve actual cash, along with changes in working capital.

A company reports $100,000 in net income. During the same period, it records:

Here’s how to calculate operating cash flow:

| Net Income: | $100,000 |

| + Depreciation: | +$15,000 |

| – Increase in accounts receivable: | –$10,000 |

| + Increase in accounts payable: | +$5,000 |

| = Operating Cash Flow: | $110,000 |

The company generated more cash ($110K) than it reported in net income ($100K). This reconciliation helps analysts evaluate earnings quality. If net income is consistently higher than operating cash flow, that can be a red flag.

Use both net income and cash flow to gain comprehensive insights into a company’s health.

Net income measures profitability and operational efficiency. It shows:

Operating cash flow reflects liquidity and sustainability. It answers the following questions about the company’s ability to turn profit into actual cash:

What if a company shows profit but lacks cash? This gap may signal deeper issues, such as delayed customer payments, inventory problems, or aggressive revenue recognition.

Financial analysts integrate both metrics across various analytical frameworks:

Companies with strong results in profits and cash flows generally demonstrate the most sustainable financial health and long-term growth potential.

Net income and cash flow act as two lenses on financial performance. In financial analysis, the real value comes from understanding how these metrics interact. Together, they reveal how much profit a company reports and how much cash it actually collects and spends.

When both are strong, it’s a sign of a well-managed business. When they diverge, it’s a prompt to dig deeper.

Want to build this kind of financial insight? CFI’s Financial Analysis Fundamentals course is a great next step — it’s also part of our Financial Modeling & Valuation Analyst (FMVA®) Certification, designed to equip you with the practical skills analysts need to stand out.

Ready to become a world-class financial analyst?

CFI’s FMVA® Certification teaches you to build advanced financial models in Excel, perform valuation, and deliver insights that drive decisions. Learn at your own pace through structured courses and hands-on practice — and earn an industry-recognized credential.