Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The identification, analysis and response to risk factors affecting a business

Risk isn’t just an abstract concept — it’s the hidden variable shaping every financial decision. Some businesses incorporate risk management to adapt and grow stronger. Others ignore it and collapse under pressure.

Consider the 2008 Global Financial Crisis: firms that failed to manage their exposure to high-risk mortgage-backed securities suffered catastrophic losses. Meanwhile, those who hedged their positions, diversified assets, and monitored liquidity emerged in a position of strength.

The lesson? Don’t wait and react; control risk before it controls you.

But what is risk management in business? More than a defensive strategy, it’s a financial discipline that determines whether a company thrives in uncertainty or becomes a cautionary tale. True financial risk management goes beyond preventing losses, creating stability, protecting investments, and unlocking opportunities others fail to see.

Risk management structures do more than point out existing risks. A good risk management structure should also calculate the uncertainties and predict their influence on a business. Consequently, the result is a choice between accepting risks or rejecting them. Acceptance or rejection of risks is dependent on the tolerance levels a business has already defined for itself.

If a business sets up risk management as a disciplined and continuous process for the purpose of identifying and resolving risks, then the risk management structures can be used to support other risk mitigation systems. They include planning, organization, cost control, and budgeting. In such a case, the business will not usually experience many surprises, because the focus is on proactive risk management.

Response to risks usually takes one of the following forms:

When creating contingencies, a business needs to engage in a problem-solving approach. The result is a well-detailed plan that can be executed as soon as the need arises. Such a plan will enable a business organization to handle barriers or blockages to success by dealing with risks as soon as they arise.

Risk management is essential because it empowers a business with the tools to adequately identify and deal with potential risks. Once a risk is identified, it is easy to mitigate. In addition, risk management provides a business with a basis upon which it can undertake sound decision-making.

Assessment and management of risks are the best ways for a business to prepare for eventualities that may hinder progress and growth. When a business evaluates its plan for handling potential threats and then develops structures to address them, it improves its odds of becoming a successful entity.

In addition, progressive risk management ensures that high priorities are dealt with as aggressively as possible. Moreover, management will have the necessary information to make informed decisions and ensure the business remains profitable.

Every business must answer one fundamental question: Are we prepared for the risks ahead?

Risk is measurable, quantifiable, and deeply embedded in financial decision-making. Companies that fail to establish a corporate finance risk management framework expose themselves to financial risks beyond monetary losses. Market instability, investor distrust, and regulatory penalties can cripple operations if these risks go unaddressed.

Key financial risks every business must navigate include:

Without risk assessment, businesses move blindly, reacting to financial shocks instead of preparing for them. The difference between resilient companies and those that fail isn’t luck — it’s strategic risk management.

Every major financial failure can be prevented with the right risk controls in place. Risk isn’t an afterthought; it’s the foundation of financial stability. Here’s how businesses build it:

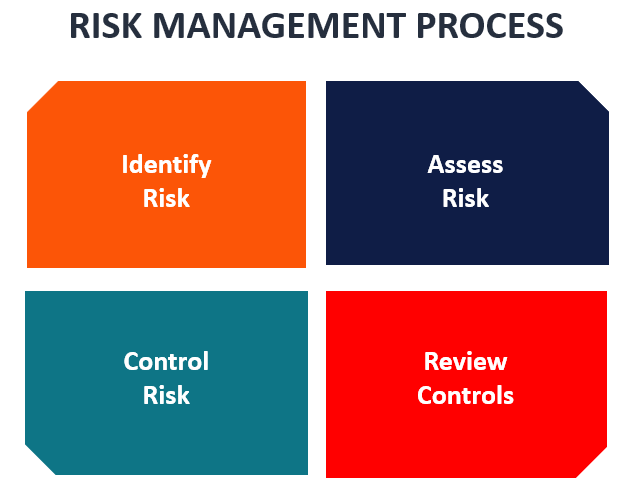

Risk identification mainly involves brainstorming. A business gathers its employees to review various sources of risk. The next step is to arrange the identified risks in order of priority. Because it is impossible to mitigate all existing risks, prioritization ensures that those risks that can significantly affect a business are dealt with more urgently.

In many cases, resolution involves identifying the problem and then finding an appropriate solution. However, before figuring out how best to handle risks, a business should locate the source by asking, “What caused such a risk and how could it influence the business?”

Not all risks are equal. An unexpected lawsuit isn’t the same as missing a loan payment. High-priority risks (a sudden credit downgrade or regulatory violation) require immediate action, while lower-priority risks can be monitored.

Once a business entity is set on assessing likely remedies to mitigate identified risks and prevent their recurrence, it needs to ask the following questions: What measures can prevent the identified risk from recurring? And what is the best thing to do if it does recur?

Here, the ideas found to be useful in mitigating risks are divided into tasks and then into contingency plans to deploy in the future. If risks occur, the plans can be put into action.

A clear risk management definition goes beyond textbook theory: it’s about real-world execution. It’s a pillar of risk management, meaning companies must proactively mitigate uncertainty rather than react to crises. In finance, the cost of poor risk management isn’t just monetary; it’s reputational. The ability to anticipate and control risk separates elite financial professionals from the rest.

As a result, it is crucial to understand the principles of risk management and how they mitigate the effects of risks on business entities. That’s why industry leaders turn to CFI. Our courses aren’t built on theory alone. They’re structured around the same corporate finance and risk management principles used by investment firms and global financial institutions.

If you’re serious about mastering financial risk management and ensuring long-term financial stability, start with our Risk Management Specialization, then expand your expertise by exploring our full collection of risk management strategies courses.

Thank you for reading CFI’s guide to Risk Management. To keep learning and advancing your career, the following CFI resources will be helpful: