Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The terms “cash” and “liquidity” are often used interchangeably even in some business meetings, investor calls, and financial communications. Treating these two distinct terms as the same thing can lead to costly misunderstandings.

This article breaks down cash vs. liquidity to explain the differences, show where each appears in financial statements, and how to use the right term in the right context.

In finance and accounting, cash refers to money (currency) that is readily available for a company to use. It may be kept in physical form or digital form held in a company’s cash banking accounts.

Cash is often paired with cash equivalents, which are usually short-term investments with original maturities of three months or less, such as money market funds and Treasury bills.

Cash is the lifeblood of a business. To pay its operating expenses, a company must have enough cash on hand to pay employees, contractors, vendors, and suppliers. A business also uses cash to fund capital expenditures and invest in long-term growth projects.

When companies lack adequate cash, they often raise capital, meaning they obtain funding by borrowing (debt) or issuing shares (equity). These financing methods give the company the cash it needs to move forward with those investments.

Cash plays a central role in a company’s financial statements. To track how a company’s cash position changes over time, accountants prepare a statement of cash flows, which shows all the cash coming in and going out of the business. The statement ends with the net change in cash during the period.

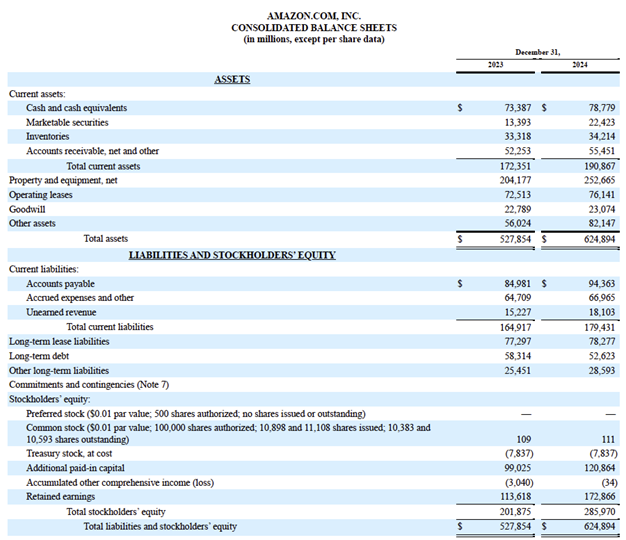

On the balance sheet, cash often appears as the first item in the current assets section because it’s available for immediate use. The image below shows Amazon’s 2024 balance sheet with cash and cash equivalents listed at the top.

Liquidity refers to a company’s ability to meet short-term financial obligations using assets that can quickly be converted into cash. The key distinction in the cash vs. liquidity conversation is that cash is just one part of a broader liquidity picture.

In accounting, cash and other liquid assets are called current assets, which are resources expected to be converted to cash or used within one year. Current assets include:

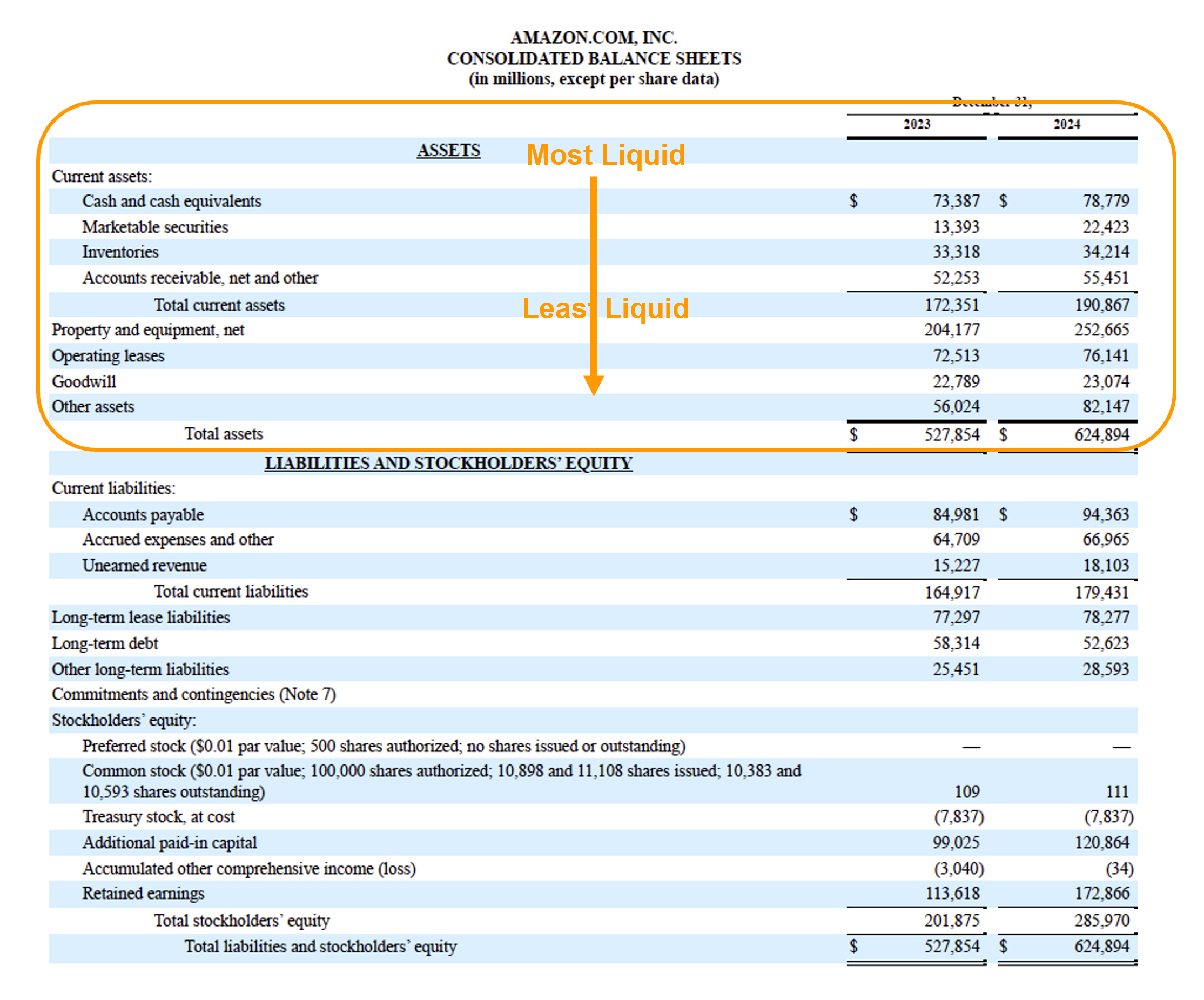

On a company’s balance sheet, current assets usually appear at the top of the asset section, listed in order of liquidity with cash first and less liquid items like inventories last.

Assets that are not expected to convert into cash within a year, such as Property, Plant & Equipment (PP&E), are categorized as non-current assets and listed further down in the balance sheet.

The image below shows Amazon’s 2024 balance sheet with assets and liabilities in order of their liquidity.

Cash is a specific asset: the money a company holds in physical form or in the bank. Liquidity refers to how easily a company can access enough cash to meet short-term obligations. The terms are closely related, which is why they’re often confused.

Think of it this way: cash is the money in your wallet. Liquidity is your ability to pay for something quickly with cash or by converting other assets into cash. For example, selling securities, such as stocks or bonds, gives you access to cash within a few days.

Here’s a quick comparison:

| Description | Ability to pay now with actual money (currency). | Ability to meet short-term financial obligations. |

| What It Includes | Physical currency and cash held in bank accounts. | Cash and other assets (e.g., accounts receivable, marketable securities). |

| Relevant Financial Statements | Cash flow statement; line item on the balance sheet. | Balance sheet in the current assets section. |

| Focus | Actual cash balance in the present. | Ability to access cash to pay near-term expenses. |

| Interpretation | A strong cash balance supports liquidity but isn’t the full picture. | A company may be liquid with minimal cash if other assets are accessible and obligations are low. |

A company with limited cash may still be liquid if it holds other assets that can be readily converted into cash. Conversely, a company may have some cash on hand. But if most of its other assets are difficult to quickly convert into cash, it could face liquidity issues.

Cash and liquidity are often used interchangeably, even though they refer to different things. Their close connection in financial reporting and analysis contributes to the confusion, even by some experienced professionals.

Part of the confusion comes from how closely the two terms appear in financial contexts:

This misunderstanding can lead to miscommunication or poor decision making. For example, a finance student might focus only on how much cash a company has, without considering other current assets.

Or an early career analyst might assume a company is liquid simply because it has some cash. That assumption could be misleading if the company doesn’t have other assets that can be quickly converted into cash to cover operations and debt expenses.

Knowing how cash and liquidity differ helps you interpret financial information with more context and accuracy. It also gives you the language to communicate financial health in a way that aligns with how analysts, investors, and business leaders think.

This kind of core knowledge strengthens your analysis and builds confidence when you’re working with balance sheets, cash flow data, or real-world financial scenarios.

If you’re looking to grow your finance skills, this is exactly where it starts.

Breaking into finance requires the right skills and a clear career strategy. CFI’s courses provide step-by-step learning paths to help you:

Whether you’re just starting out or looking to specialize, CFI offers the training and resources you need to take the next step.

Ready to launch your finance career? Explore CFI’s dynamic course catalog and professional certifications and start building the skills that will set you apart.