Get In-Demand Finance Certifications

A type of stock option used by employers to compensate and incentivize employees

A non-qualified stock option (NSO) is a type of stock option used by employers to compensate and incentivize employees. It is also a type of stock-based compensation.

Unlike incentive stock options (ISOs), which come with special tax benefits, holders of non-qualified stock options are required to pay taxes based on the price of the stock at the time when the options are exercised.

Companies offer employees non-qualified stock options with the expectation that the underlying stock price will increase in the future. NSOs are preferred by employers because they serve as both a form of compensation, as well as an incentive for employees to work harder, as they benefit from higher stock prices.

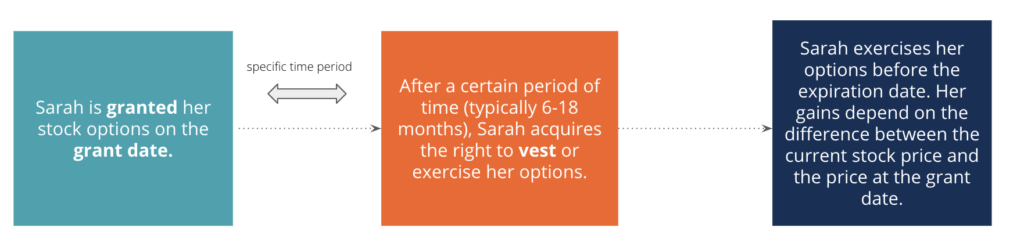

The diagram below shows what an approximate NSO timeline looks like, using the hypothetical case of Sarah, a new associate at a publicly-traded bank:

The section below covers further details and calculations on the value of NSOs and how they are taxed:

As mentioned earlier, employees are required to pay taxes on NSOs when they choose to exercise their options since exercising the options creates a reportable income. The amount that will be taxed is given by:

In Sarah’s case, let us assume that she’s been granted 1,000 shares with a grant price of $5 each. She exercises the options one year later and sells her shares immediately at the market price of $45.

The total taxable amount is equal to $40,000 [1000 x ($45 – $5)].

Suppose that the flat income tax rate for Sarah is 30%. Therefore, the total tax she needs to pay is equal to $12,000 ($40,000 x 0.30).

Sarah may choose to pay the amount by forgoing an equal amount of shares. The total number of shares she would need to give away is equal to $12,000/$45 = 266.67, or 267 shares.

Even after giving away 267 shares in taxes, Sarah sells 733 shares worth $45 each – giving her a total income of $32,895 after taxes.

An alternative to selling her shares immediately would be holding on to them in expectation of increases in the market value. There are two types of scenarios that can result from the above:

1. Sarah holds her shares for less than 12 months before selling them

In this case, Sarah would be required to pay the short-term capital gains tax rate on the profits she has made. The rates are typically pegged to tax brackets and are equal to ordinary income taxes. The amount is given by:

2. Sarah holds her shares for more than 12 months before selling them

In this case, Sarah would be required to pay the long-term capital gains tax rate on the profits she made. The rates typically range between 0%-20%, depending on her income. The amount is calculated by:

Therefore, by holding her shares for a longer period of time, Sarah may have the chance to save on tax payments through the capital gains tax rates. However, it carries uncertainty and risk since her gains depend on the price movements of the underlying stock.

If the stock falls in value, Sarah is likely to lose a lot of her income and vice versa.

Non-qualified stock options benefit employers in ways that are similar to all other stock options. By serving as an effective compensation method, it reduces the potential cash outflow and allows the company to retain higher cash and liquidity for other needs. It also acts as an incentive for employees – once they have a vested interest in the company, they are likely to be loyal and motivated to increase the value of the stock.

In addition to the above, the use of NSOs also allows employers to benefit from a tax deduction equal to the amount of income from stock options declared by the receiver (i.e., employee), which is why it is preferred by employers.

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.