Get In-Demand Finance Certifications

A type of deferred employee compensation plan where plan participants benefit from the upside of a company’s share price without actually receiving company shares

A phantom stock plan, also called a shadow stock plan, is a type of deferred employee compensation plan where the type of shares issued to plan participants are phantom shares instead of company shares. Phantom shares provide benefits similar to stock ownership but without actually issuing company shares.

Phantom shares are a contractual agreement between the phantom stock plan participant and the employer. The agreement gives the participant the right to cash payments at (1) specified times or (2) specified conditions based on the market value of equivalent shares of the company.

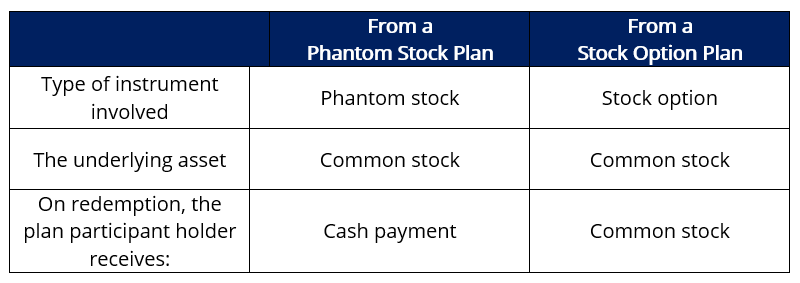

The concept is better understood below, where we contrast phantom shares (from a phantom stock plan) with stock options (from a stock option plan).

For example, assume John was issued 500 phantom shares of Company A in January that are worth $50 per share and are redeemable in March. In March, the common share price of Company A is $70. If John redeems the 500 phantom shares in March, he will receive:

The choice between the two options depends on whether the phantom stock plan is “appreciation only” or “full value,” as discussed below.

The two main types of phantom stock plans are:

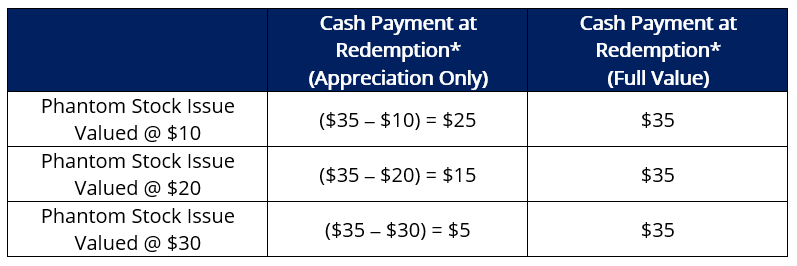

In an “appreciation only” phantom stock plan, the plan participant receives a cash payment equal to the difference between the company’s stock price at redemption and the issuing price of the phantom stock. For example, assume the issuing price of the phantom stock is $10. At redemption, the company’s common share price was $30. The cash payment per phantom stock would be $20.

In a “full value” phantom stock plan, the plan participant receives a cash payment equal to the value of the underlying asset (common stock) of the phantom stock at redemption. For example, assume the issuing price of the phantom stock is $10. At redemption, the company’s common share price was $30. The cash payment per phantom stock would be $30.

A phantom stock plan and stock option plan both award employees from the share appreciation of the company’s stock price.

However, there is one key difference between the two plans. On redemption, in a phantom stock plan, the plan participant receives a cash payment. This is in comparison to a stock option plan, where the plan participant receives common stock. As a result, a phantom stock plan allows the participant to reap the benefits of an increasing share price without shareholder dilution.

The issuing price of phantom shares in a phantom stock plan is set by the company and not necessarily tied to the value of the company’s stock at that time. With that said, the company typically follows a valuation policy for the issuing price of phantom shares.

For example, a company can set the issuing price of their phantom shares at $10, $20, or $30 without regard to its share price at the time. With that said, the value of the phantom stock at redemption is tied to the company’s stock price. Understandably, a lower issue phantom share value provides greater upside for the plan participant upon redemption:

In general, if at redemption, the company’s stock price is below the issuing price of the company’s phantom stock, the plan participant is not entitled to a cash payment.

For example, if the issuing price of the phantom shares is $50 and the company’s share price at redemption is $20, the plan participant would not reap any benefits.

A phantom stock plan constitutes a deferred compensation plan. Such plans must conform to IRS Section 409A and be vetted by an attorney with plan details specified in writing.

A phantom stock plan could be a potential, uncapped liability for the issuing company due to the fact that the payment is tied to the share price at redemption. The issuing company generally remedies the matter through:

For example, an issuing phantom stock price of $50 when the company’s current share price is $40.

For example, capping the cash payment to a company share price limit of $50. If the issuing phantom stock price is $30, and the company’s share price at redemption is $100, the cash payment per phantom stock would be capped at $50 – $30 = $20.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: