Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

A measure of cash flow used in real estate

Funds from operations (FFO) is the actual amount of cash flow generated from a company’s business operations.

To calculate the net FFO, one must add the non-cash expenses or losses that are not actually incurred from the operations, such as depreciation, amortization, and any losses on the sale of assets, to net income. Then subtract any gains on the sale of assets and interest income.

FFO is commonly used by companies that engage in Real Estate Investment Trusts (REITs), a business that primarily operates on income-generating real estate transactions. REIT companies are involved in commercial real estate – selling, leasing, and financing office space and apartment buildings, warehouses, hospitals, shopping centers, hotels, and timberlands.

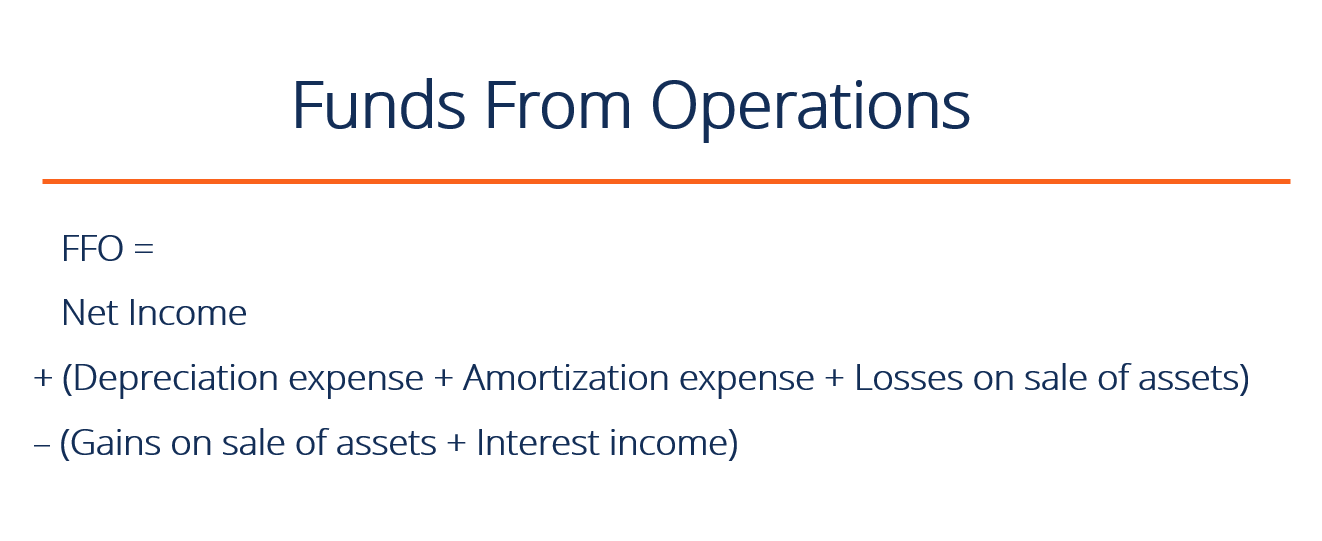

Here is the formula to calculate FFO:

FFO = Net Income + (Depreciation Expense + Amortization Expense + Losses on Sale of Assets) – (Gains on Sale of Assets + Interest Income)

For example:

Big Time Real Estate Company declared a net income of $10M last year, a depreciation expense of $2M, an interest amortization expense of $1M, an interest income of $500,000, and a gain on the sale of various assets of $1M. The actual cash flow from business operations (FFO) for Big Time Real Estate Company comes out to $11.5M.

These finance terms are costs that need to be added back to net income to determine the actual earnings generated from the company’s core business operations. Non-operating expenses are excluded from the main business functions and, therefore, should be added back to net income.

Depreciation – Depreciation is an expense allocated to cover capital expenditures (the acquisition of Property Plant and Equipment PP&E, or any fixed assets). Depreciation is a non-cash expense because it is only created for accounting purposes and does not match the timing of when cash was used to buy the asset.

Amortization – Loan and capital expense payments spread out over a specific period of time.

Losses on the sale of assets – Loss is incurred when an asset is eliminated, and the selling price is lower than the net book value of the asset sold. This is another non-cash expense.

Gains on the sale of an asset and interest income are deducted from net income to calculate the actual cash flow from operations. The earnings are not from the main operations of the business.

Gains on the sale of assets – Gain obtained when an asset is sold, and the selling price is higher than the net book value of the asset.

Interest income – Earnings from the interest of marketable securities, long-term investments, or cash maintained in interest-paying checking accounts.

FFO measures the business’s operational efficiency or performance, especially for most REIT companies. The reason for this is that real estate values are proven to rise and fall with macroeconomic conditions. Any operating results computed when using the cost accounting method do not usually serve as an accurate measurement of performance.

Real estate companies use FFO as a more accurate operating performance benchmark. Investors also use this metric to determine the financial performance of a real estate company.

We hope this CFI guide to FFO has been helpful in your understanding of how investors look at the financial performance of REITs. To keep expanding your knowledge, we highly recommend these additional CFI resources: