Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

Net income — also called net profit or net earnings — is the amount of profit a company retains after deducting all expenses.

Net Income Definition: Net income is the amount of accounting profit a company has left over after subtracting all of its expenses. It connects directly to the balance sheet and cash flow statement and is a key measure of financial performance.

Also called net profit or net earnings, net income is calculated by taking total revenue and subtracting cost of goods sold (COGS), operating expenses, interest, taxes, depreciation, and amortization.

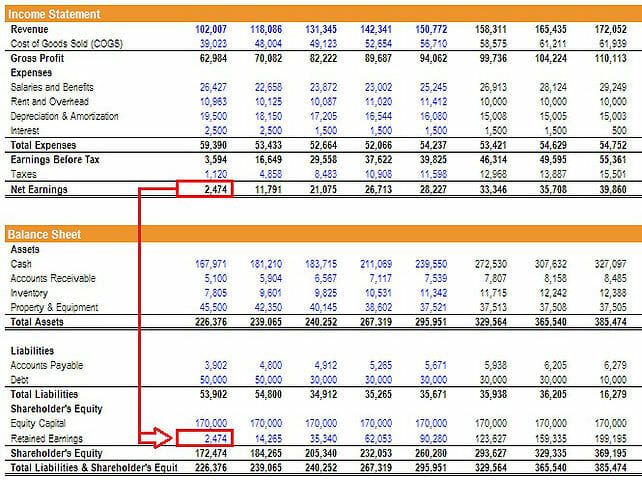

It’s often referred to as the “bottom line” because it appears at the end of the income statement. Some income statements have a separate section at the bottom that reconciles beginning retained earnings with ending retained earnings, through net income and dividends.

To calculate net income, subtract all expenses from your company’s total revenue.

Net Income Formula:

Here’s what this looks like in practice:

A business earns $500,000 in total revenue. It incurs $350,000 in total expenses, including payroll, operating costs, interest, and taxes.

Net Income = $500,000 – $350,000 = $150,000

This amount represents the company’s profit for the period and is recorded on the income statement.

The bottom line of a company’s income statement has three commonly used names, which include:

These terms are used interchangeably and all refer to the same concept — money left after covering all expenses. This can sometimes be confusing for people who are new to finance and accounting. In this article, we use all three terms interchangeably.

The net income is very important in that it is a central line item to all three financial statements:

Net income flows into the balance sheet through retained earnings, an equity account. This is the formula for finding ending retained earnings:

Assuming there are no dividends, the change in retained earnings between periods should equal the net earnings in those periods. If there is no mention of dividends in the financial statements, but the change in retained earnings does not equal net profit, then it’s safe to assume that the difference was paid out in dividends.

In the cash flow statement, net earnings are used to calculate operating cash flows using the indirect method. Here, the cash flow statement starts with net earnings and adds back any non-cash expenses that were deducted in the income statement. From there, the change in net working capital is added to find cash flow from operations.

Net earnings are also used to determine the net profit margin. This is a handy measure of how profitable the company is on a percentage basis, when compared to its past self or to other companies.

Net profit margin is also used in the DuPont method for decomposing return on equity (ROE). The basic DuPont formula splits ROE into three components:

Analyzing a company’s ROE through this method allows the analyst to determine the company’s operational strategy. A company with high ROE due to high net profit margins, for example, can be said to operate a product differentiation strategy.

Net income is often discussed alongside other financial terms like gross income and cash flow, but they serve different purposes and are calculated differently. Understanding how net income compares to these related metrics is key to interpreting a company’s overall financial performance.

Gross income is often confused with net income, but they represent different stages of a company’s profitability. Gross income shows revenue before expenses, while net income reflects the company’s true profitability after all deductions.

It’s important to remember that net income is not the same as cash flow.

Net income includes non-cash expenses such as:

Because of this, net income does not reflect the actual cash a company generated during the period.

Financial analysts often adjust net income when building financial models or performing valuations to calculate free cash flow, which is a more accurate measure of a business’s liquidity and operational performance.

To learn more, explore CFI’s financial modeling courses.

Click the button below to download our free Net Income template.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Net income refers to the profit a company has after subtracting all expenses from its revenue. It shows how much the company actually earned during a period.

Use this simple formula:

Net Income = Total Revenue – Total Expenses

Make sure to subtract all costs, including COGS, taxes, depreciation, and interest.

Yes, net income, net profit, and net earnings all mean the same thing. They describe the remaining income after all expenses have been deducted.

It appears on the last line of the income statement and ties into other financial statements like the balance sheet and cash flow statement.

Net income helps investors, analysts, and business owners evaluate a company’s financial health. It shows if the business is operating efficiently and generating value for shareholders.

Thank you for reading CFI’s guide to Net Income. The CFI resources below are designed to give you the tools and training you need to become a great financial analyst: