Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

Debt financing to support a predetermined business purpose or expenditure

A commercial loan is a form of credit that is extended to support business activity. Examples include operating lines of credit and term loans for property, plant, and equipment (PP&E).

While a few exceptions exist (including commercial property owned by an individual), the overwhelming majority of commercial loans are extended to business entities like corporations and partnerships.

Private businesses with financing needs generally borrow from a commercial bank or credit union; however, they may also seek credit from equipment finance (leasing) firms or other private, non-bank lenders (like factoring companies).

Every commercial loan provider assesses timing, risk, and how a business generates and moves money before approving a loan. Factors that go into the loan include repayment, collateral, and whether the terms fit the company’s cash flow cycle. What makes sense for one borrower might fall apart for another.

A coffee shop preparing for the holiday rush might use a business line of credit that adjusts with seasonal swings. A logistics company buying trucks could take out a five-year term loan, matched to the vehicles’ lifespan and the company’s income stream. Both are examples of commercial loans, but the structure is tailored to each borrower’s reality.

Revolving Credit: This is best for variable needs, such as retail stock, receivables gaps, and payroll cycles. Borrowers use what they need and pay it back in cycles, often tied to working capital accounts.

Term Loans: These fund longer-term investments like equipment or commercial property. Amortization schedules might include balloon payments or early interest-only periods to ease initial strain on cash flow.

Example: A brewery expanding its taproom might secure a 7-year term loan with a 15-year amortization schedule, easing pressure in year one while revenue scales.

Commercial loans require collateral in most cases. Lenders want assurance that there’s something tangible to claim if the loan isn’t repaid. Common assets used as collateral include real estate, equipment, or receivables and inventory:

Unsecured options exist but are rare — usually offered only to businesses with pristine credit or federal backing, such as through the Small Business Administration (SBA).

Loan-to-value (LTV) ratios limit how much a lender will issue relative to the asset’s worth. For example:

Amortization terms also follow the asset’s life:

The idea is to keep repayments realistic and proportional to how the asset generates income or depreciates over time.

Rates reflect risk. Lenders consider:

Riskier profiles may face more restrictive covenants, like maintaining a set liquidity reserve or prohibiting dividends until the loan is repaid.

No two banks price risk the same, but most have policy boundaries:

In the end, structuring a commercial loan is about alignment: matching the borrower’s needs to the lender’s confidence. When those two pieces fit, the deal moves.

There are many forms of credit available to support businesses, but we’ll look at some of the most common types:

An LOC (often referred to as a “revolver”) supports the working capital cycle for firms that sell on credit terms. There is no set repayment schedule; it’s structured to revolve up and down as balances change in the company’s working capital accounts.

Term loans are used to acquire non-current assets, such as equipment, vehicles, and furniture. They are typically amortizing, meaning they reduce with periodic payments (often monthly). At the time of loan advance, both the borrower and the lender will have already agreed upon a repayment schedule. The loan repayment period is generally aligned with the useful life of the underlying asset being financed.

Capital leases — sometimes referred to as “finance leases” — serve a similar purpose to term loans (meaning they’re used to finance non-current, capital assets like equipment). The main difference between a term loan and a capital lease is that the equipment finance firm funding the lease retains the legal title of the physical asset (as opposed to registering a lien over it).

Commercial mortgages are another type of term lending, but they’re used exclusively to finance (or refinance) commercial real estate. The analysis and underwriting techniques vary depending on whether the property is owner-occupied or if it’s an income-producing investment property; however, both tend to have more flexible terms (longer amortization, more favorable LTVs, very competitive pricing, etc.) than other types of commercial loans.

Acquisition loans are another category of commercial loans. They are used by businesses that are buying other businesses (or other business divisions) rather than physical assets like property or equipment. While not universally true, acquisition loans tend to have shorter amortization periods and lower loan-to-values than other types of commercial loans.

Commercial lending decisions weigh risk from financial performance, legal structure, and day-to-day operations. Whether you’re assembling a loan package or reviewing one for approval, knowing what lenders look for helps ensure the deal holds up under scrutiny.

Business Financials:

Most lenders request three years of income statements, balance sheets, and cash flow statements. They evaluate trends in revenue, liquidity (e.g., current ratio >1.2x), and leverage (debt-to-equity ratio).

Credit History:

Lenders often require a personal FICO score above 680 and a business credit score over 75 (e.g., PAYDEX). Past defaults or tax liens can raise red flags, but may be mitigated with documentation.

Loan-to-Value (LTV):

Expect ranges like:

Higher LTVs require more substantial cash flow or guarantees.

Debt Service Coverage Ratio (DSCR):

A typical minimum is 1.25x. Borrowers with volatile earnings or seasonal revenue may need to show even higher ratios to qualify.

Loan Purpose & Plan:

Lenders expect a clear breakdown of how funds will be used, including amounts, timelines, and expected ROI. Vague terms like “working capital” should be backed by details (e.g., “inventory restock for Q4”).

Entity Structure:

Legal documentation must confirm the company’s structure, ownership, and signing authority.

Common assets put up as collateral typically include real estate, equipment, and receivables. For riskier profiles, lenders may require:

Interest Type:

Duration:

Longer terms often include covenants (e.g., minimum DSCR or limits on dividends).

KYC/AML Requirements:

Lenders verify business identity (EIN, BOI forms) and monitor sources of funds. Industries with high cash turnover face stricter scrutiny.

Supporting Documents:

Licenses, tax returns, insurance coverage, and, in some cases, executive resumes may be required.

Strengths:

Red Flags:

A manufacturer might secure a $2M equipment loan at 60% LTV with a 1.30x DSCR, while a startup could pursue an SBA-backed loan with a personal guarantee and business credit cards to support working capital.

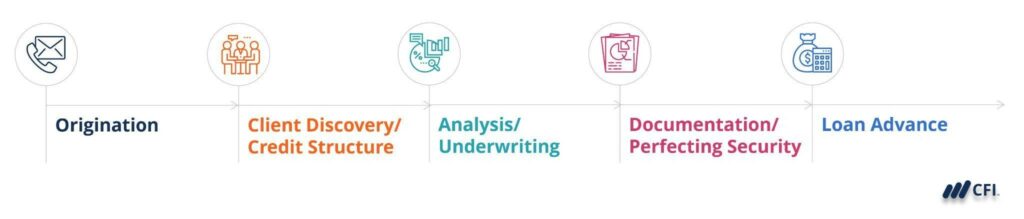

At CFI, we teach the credit process as comprising five distinct steps. These are:

These are the most common questions borrowers and finance professionals ask about commercial loans:

Yes, commercial and business loans are the same type of loan and serve the same business needs. The terms are often used interchangeably.

Traditional lenders usually look for a personal FICO score of 680 or higher and a business credit score above 75. Lower scores — down to 600 — may be accepted by alternative lenders if the borrower has strong cash flow, valuable collateral, or SBA backing.

Down payments typically range from 10% to 30%, depending on risk, collateral, and loan type. While the specifics may vary, these are generally the required down payments for commercial loans:

Borrowers with weaker financials may be asked to contribute more equity upfront.

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers in banking to the next level. To keep learning and advancing your career, the following resources will be helpful: