Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

An estate planning tool used in the United States that is structured as a trust

A grantor retained annuity trust (GRAT) is an estate planning tool used in the United States that is structured as a trust. A trust is a fiduciary agreement for one party (trustor) to maintain the rights to hold property or assets for another party (trustee) and is commonly used when transferring assets from one party to another. GRATs, in particular, are typically used when family members wish to give large financial gifts to each other in a tax-efficient manner.

To implement a GRAT, an irrevocable trust is established. The trustor will place the assets that they wish to send to the beneficiary under the trust, and an annuity is paid out on a fixed term. When the term of the trust expires, the assets are transferred to the beneficiary tax-free.

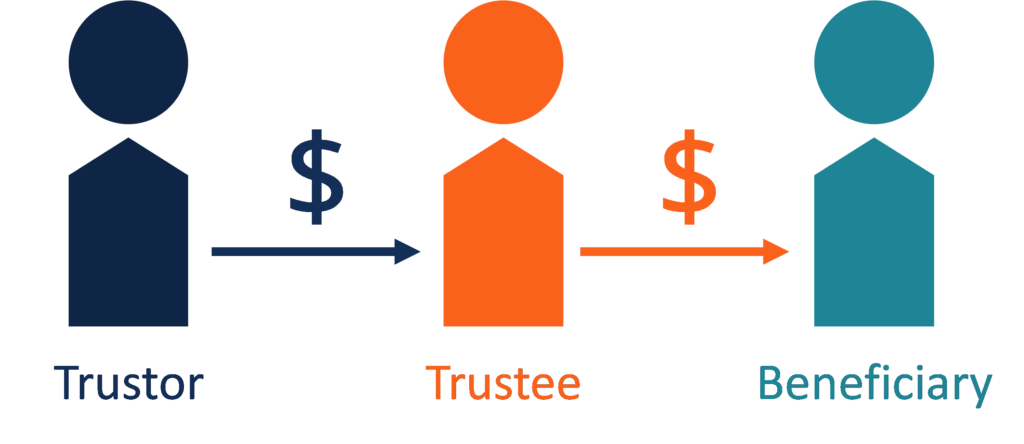

In order to understand GRATs, it is important to understand the basic concept behind a trust. As mentioned above, a trust is simply a financial instrument used to transfer assets from one party to another.

The key parties involved are:

There are many different types and structures of trusts. However, very broadly speaking, they can be categorized into two different types:

As mentioned earlier, a grantor retained annuity trust (GRAT) is a form of irrevocable trust for gifts that allow the trustor to transfer wealth to recipients (usually family members such as children and grandchildren) in a tax-advantaged manner. They are highly advantageous since there are little to no gift tax costs associated with transferring assets using this financial instrument.

The way the GRAT is set up is with the trustor or grantor, transferring their assets to an irrevocable trust with an agreement to receive fixed payments annually based on the fair market value at the time of the transfer. The payments continue until the end of the specified term of the trust. At the end of the term, the remaining value of the assets within the trust may be passed on to the beneficiary as a gift.

Grantor retained annuity trusts are generally used by wealthy individuals in order to pass their assets to the next generation. Especially if these assets are expected to grow at a high rate, such as shares in a startup or other growth companies.

Benefits of using GRATs include:

Drawbacks of using GRATs include:

The benefit of GRATs can be explained through a simple example:

Consider Max, who is 70 years old and is a recent retiree. He owns shares in a high-growth tech startup with the current value of the position valued at $10,000,000.

Max wants to transfer the shares to his child, Sam, in a tax-advantaged manner and has decided to utilize a GRAT. The shares are placed into an irrevocable trust, with a term of ten years. Each year, a $500,000 payment is paid out to Max.

After ten years, the value of the shares has increased to $20,000,000. A total of $5,000,000 has been paid out to Max, with the remaining value of the trust at $15,000,000.

We can see that the trust’s value has increased by $5,000,000, from $10,000,000 to $15,000,000.

Sam is able to receive the $5,000,000 gain free of tax.

In the above example, very simplified figures are used. However, it should be noted that the structure of the trust and the payment amount are much more complex in practice. The $500,000 payment would normally be calculated with the assumed return rate of the U.S. Internal Revenue Service, which is derived from market interest rates. Therefore, the interest rate environment is also a consideration in utilizing GRATs.

Thank you for reading CFI’s guide to Grantor Retained Annuity Trust (GRAT). To keep learning and developing your knowledge base, please explore the additional relevant resources below: