Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A situation where an expansionary monetary policy fails to raise interest rates and subsequently promote economic growth

A liquidity trap is a situation where an expansionary monetary policy (an increase in the money supply) is not able to increase interest rates and hence does not result in economic growth (increase in output). In the case of deflation or recession, individuals hold on to the money in their possession at the given interest rates because they fear such negative events.

A liquidity trap exists in three main situations:

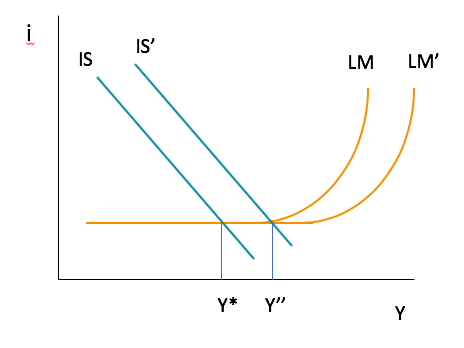

A liquidity trap usually exists when the short-term interest rate is at zero percent. The demand curve becomes elastic, and the rate of interest is too low and cannot fall further. Any steps taken by the government to boost expansion will not work, as the money supply will be held in the form of cash balances, thus making it impossible for the government to use interest rates as an economic stimulus. The concept is illustrated in the figure below:

Usually, a decrease in interest rates encourages spending, but in a liquidity trap, the change in the money supply does not change spending habits. Therefore the use of monetary policy is ineffective (as seen above).

When there is a liquidity trap, the economy is in a recession, which can result in deflation. When deflation is persistent, it can cause the real interest rate to rise. It harms investment and widens the output gap – the economy goes into a vicious cycle. If the recession is persistent as well, the deflation further reduces output, and the monetary policy is ineffective.

During the Great Depression in the U.S., the rate of inflation in the economy was –6.7%, and it was not until 1943 that the prices went back to their normal pre-crisis levels. Also, during the Japanese slump of 1995, deflation continued through 2005 with the average inflation rate at –0.2%.

The main reason for deflation in an economy is failures in the financial system. Financial slumps can intensify the liquidity trap because deflation increases the real value of debt. Borrowers are no longer able to repay their debt, and banks and other financial institutions suffer a decline as the loans are not paid back.

Both the Great Depression and the Japanese slump resulted from financial failures. In such cases, the government adopted a credit crunch policy. In order to improve existing economic conditions, the banks tried to limit new loans and write off existing ones.

However, the credit crunch policy led to a vicious cycle as it reduced investment and output as banks were also more cautious about extending credit to investors. A liquidity trap can exist when the nominal interest rate does not reach zero because the risk of holding the assets increases the chances of losing the asset once the risk is incorporated.

As traditional monetary policy is ineffective when there is a liquidity trap in the economy, governments look towards more unconventional methods to bring the economy out of the trap. One of the more effective remedies is quantitative easing. It is where central banks buy financial assets from commercial banks and other institutions, which raises prices for those assets, lowers yields, and increases liquidity in the economy.

Many researchers argue that the main reason for the Great Depression was the monetary contraction implemented by the Federal Reserve Bank in 1927. According to economist Milton Friedman, a more appropriate response to the Depression would be monetary easing or “money gifting,” as he called it. Between 1933 and 1941, the US stock market rose by 140%, mainly due to the expansionary monetary policy.

Also, in 1999, Japan used quantitative easing policies after the policy target rate was set to zero. The goal of quantitative easing was to make reserves readily available to domestic banks.

Keynesian economists would argue that the best way to mitigate the effects of a liquidity trap is through an expansionary fiscal policy. President Franklin Roosevelt used such a fiscal policy during the New Deal in 1933. The government increased spending through a public works program (e.g., the Tennessee Valley Authority). The Japanese government also spent 100 trillion yen on public programs over a ten-year period.

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA®) certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional CFI resources below: