Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A mathematical model that tracks and models the evolution of interest rates

The Vasicek Interest Rate Model is a mathematical model that tracks and models the evolution of interest rates. It is a one-factor short-rate model and assumes that the movement of interest rates can be modeled based on a single stochastic (or random) factor – the market risk factor.

According to the Vasicek model, the interest rate (denoted as drt) is determined by solving the following stochastic equation:

Where:

The Vasicek model makes use of the assumption that interest rates do not increase or decrease to extreme levels. High levels of interest rates can discourage borrowing and investment, potentially harming economic activity and prompting policies to suppress the interest rate.

Similarly, it is highly unlikely that interest rates drop below zero unless there is an economic crisis that calls for such policies. Based on the information, the Vasicek model assumes that the interest rate revolves around the long term-mean level, “b.”

The drift factor, which is defined as a(b-rt), is an important part of the model and describes the expected change in the interest rate at time t. It is also the part of the model that considers the speed of mean reversion, indicating how quickly the interest rate reverts back to the long-term mean level.

Another key component of the Vasicek model is highlighted by the equation – the volatility of the market, captured by the market risk factor dWt – which is the “single factor” (and only factor) that affects changes in interest rates in the model. Therefore, when dWt = 0, there are no market shocks and the interest is equal to the long-term mean level.

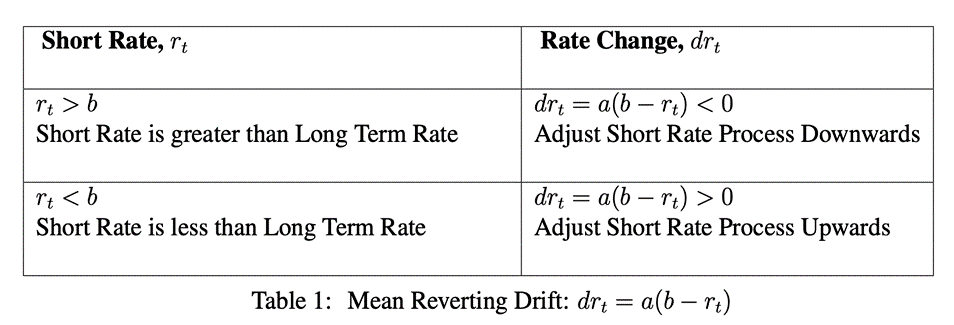

The Vasicek model exhibits a mean-reversion, which helps predict future interest rate movements. As shown in the table below, when market shocks cause the interest rate (or “short rate”) to be higher than the long term mean, the drift factor (drt = a(b-rt)) is lower than 0 – indicating that the interest rate is likely to decrease.

Similarly, when market shocks cause the interest rate to be lower than the long-term mean, the drift factor (drt = a(b-rt)) is higher than 0, which indicates that the interest rate is likely to increase. For the model to function in a stable way, the parameter a (i.e., the speed of mean reversion) must always be positive.

The Vasicek model states that the interest rate fluctuates around the long-term mean level. Therefore, an increase in the interest rate followed by a mean reversal to its long-term level b forms a resistance level.

Similarly, a decrease in the interest rate followed by a “bounce” back to its long-term mean level b forms a support level.

Although the Vasicek model was an important step forward in developing predictive interest rate models, it exhibits two key limitations:

The volatility of the market (or market risk) is the only factor that affects interest rate changes in the Vasicek model. However, multiple factors may affect the interest rate in the real world, which makes the model less practical.

The Vasicek model allows for negative interest rates, which is a highly undesirable scenario for any economy. Negative interest rates are employed by central banks in times of extreme financial crises and are considered highly improbable. However, in recent times, it’s become evident that negative interest rates are used as a monetary policy tool by central banks.

CFI offers the Capital Markets & Securities Analyst (CMSA®) certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: