Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

The interest rate that applies to personal loans

The applicable federal rate (AFR) is the interest rate that applies to personal loans. It is the minimum rate applicable to such loans under U.S. law. The AFR is implemented in the form of federal tax regulations that are enforced by the Internal Revenue Service (IRS).

The applicable federal rate applies to loans where the interest rate is lower than the tax rate if the loan were to otherwise be income. The AFR varies between short, medium, and long-term loans and is subject to flexibility due to market conditions and other macroeconomic factors. The U.S. Internal Revenue Service (IRS) publishes the rates monthly, and they are made public to serve as a benchmark for lenders throughout the country.

The purpose of the applicable federal rate is to avoid tax incidence on a personal loan. A personal loan may be thought of as a taxable gift by the IRS. Hence, the borrower would be taxed as if the loan was a part of their income. So, such a loan cannot be interest-free.

One way to satisfy the interest rate requirement might be to offer a really low interest rate. It will make the loan practically interest-free. It is where the minimum rate requirement comes in. Any loan with a lower interest rate than the corresponding AFR is called a below-market loan.

The difference between the interest rate on the lower rate and the AFR is called the imputed interest. If a lender decides to advance a loan at a lower rate, then they must pay tax on the imputed interest, as it is as income even though there is no actual cash flow.

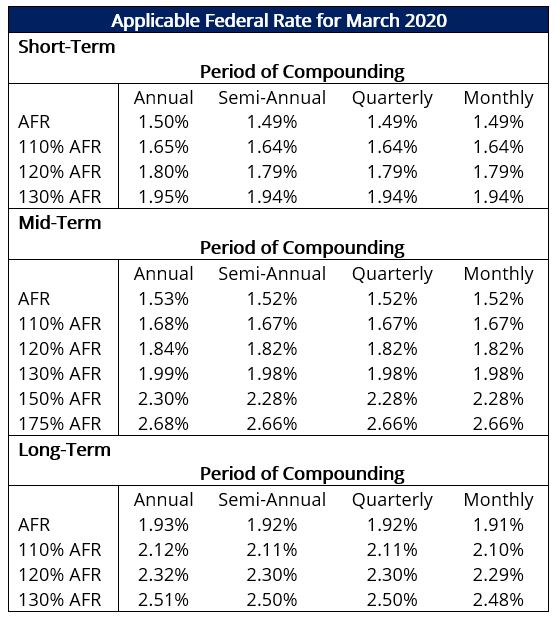

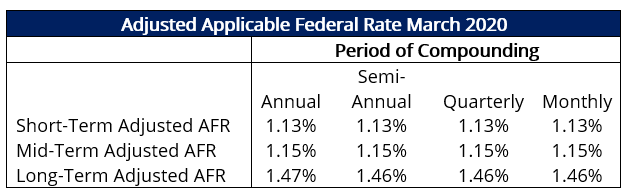

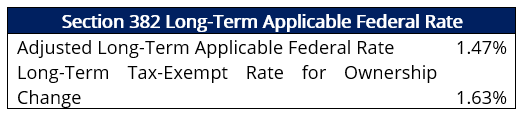

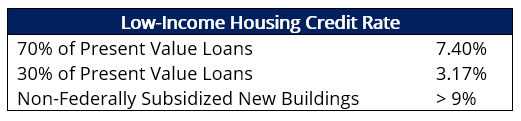

The IRS releases a document every month that enlists the applicable federal rate for different conditions. The key rates are listed based on the term and compounding frequency. Other rates usually are derived from these key rates or are determined by the Department of Treasury. The following tables are part of the IRS document.

The rates are determined using historical key rates. The long-term rate is the same as the adjusted long-term AFR, while in case of ownership change, the rate is the maximum adjusted long-term AFR of the current and past two months.

The rates are determined by the Department of Treasury.

The rate is 120% of the annual mid-term AFR.

The AFR is calculated and set for each month. The IRS puts out a document every month with the listing of the relevant rates for different terms of the loans described below.

There are three types of rates depending on the term of the loan, and rates are determined based on the term:

The law governing the determination of the rates is 26 U.S.C. § 1274(d), which is part of the Internal Revenue Code. The corresponding part of the law is reproduced below:

Put simply, the short-term rate is determined as the average of yield on the marketable debt of the United States with a maturity of three years or less over the month preceding the month for which the rate needs to be calculated. Longer-term rates are calculated in a similar way.

A leaseback or sale-leaseback transaction is where one sells an asset then leases it back for use. For such transactions, the rule is that 110% of the applicable federal rate shall apply.

There are also exceptions to the application of the AFR in certain transactions. Some of the transactions are listed below:

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: