Basel Accords

A set of banking supervision regulations set by the Basel Committee on Banking Supervision (BCBS)

What are the Basel Accords?

The Basel Accords refers to a set of banking supervision regulations set by the Basel Committee on Banking Supervision (BCBS). They were developed over several years between 1980 and 2011, undergoing several modifications over the years.

The Basel Accords were formed with the goal of creating an international regulatory framework for managing credit risk and market risk. Their key function is to ensure that banks hold enough cash reserves to meet their financial obligations and survive in financial and economic distress. They also aim to strengthen corporate governance, risk management, and transparency.

The regulations are considered to be the most comprehensive set of regulations governing the international banking system. The Basel Accords can be broken down into Basel I, Basel II, and Basel III.

Basel I

Basel I, also known as the Basel Capital Accord, was formed in 1988. It was created in response to the growing number of international banks and the increasing integration and interdependence of financial markets. Regulators in several countries were concerned that international banks were not carrying enough cash reserves. Since international financial markets were deeply integrated at that time, the failure of one large bank could cause a crisis in multiple countries.

Basel I was enforced by law in G10 countries in 1992, but more than 100 countries implemented the regulations with minor customizations. The regulations aimed to improve the stability of the financial system by setting minimum reserve requirements for international banks.

It also provided a framework for managing credit risk through the risk-weighting of different assets. According to Basel I, assets were classified into four categories based on risk weights:

- 0% for risk-free assets (cash, treasury bonds)

- 20% for loans to other banks or securities with the highest credit rating

- 50% for residential mortgages

- 100% for corporate debt

Banks with a significant international presence were required to hold 8% of their risk-weighted assets as cash reserves. International banks were guided to allocate capital to lower-risk investments. Banks were also given incentives for investing in sovereign debt and residential mortgages in preference to corporate debt.

Basel II

Basel II, an extension of Basel I, was introduced in 2004. Basel II included new regulatory additions and was centered around improving three key issues – minimum capital requirements, supervisory mechanisms and transparency, and market discipline.

Basel II created a more comprehensive risk management framework. It did so by creating standardized measures for credit, operational, and market risk. It was mandatory for banks to use these measures to determine their minimum capital requirements.

A key limitation of Basel I was that the minimum capital requirements were determined by looking at credit risk only. It provided a partial risk management system, as both operational and market risks were ignored.

Basel II created standardized measures for measuring operational risk. It also focused on market values, instead of book values, when looking at credit exposure. Additionally, it strengthened supervisory mechanisms and market transparency by developing disclosure requirements to oversee regulations. Finally, it ensured that market participants obtained better access to information.

Basel III

The Global Financial Crisis of 2008 exposed the weaknesses of the international financial system and led to the creation of Basel III. The Basel III regulations were created in November 2010 after the financial crisis; however, they are yet to be implemented. Their implementation’s constantly been delayed in recent years and is expected to occur in January 2022.

Basel III identified the key reasons that caused the financial crisis. They include poor corporate governance and liquidity management, over-levered capital structures due to lack of regulatory restrictions, and misaligned incentives in Basel I and II.

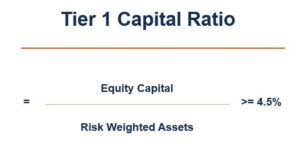

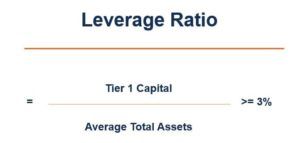

Basel III strengthened the minimum capital requirements outlined in Basel I and II. In addition, it introduced various capital, leverage, and liquidity ratio requirements. According to regulations in Basel III, banks were required to maintain the following financial ratios:

Also, Basel III included new capital reserve requirements and countercyclical measures to increase reserves in periods of credit expansion and to relax requirements during periods of reduced lending. Under the new guideline, banks were categorized into different groups based on their size and overall importance to the economy. Larger banks were subjected to higher reserve requirements due to their greater importance to the economy.

The Basel Accords are extremely important for the functioning of international financial markets. They can never be constant and need to continuously be updated based on present market conditions and lessons learned from the past.

Related Readings

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: