Distributable Net Income (DNI)

The portion of a trust’s income allotted to the beneficiaries

What is Distributable Net Income (DNI)?

Distributable Net Income (DNI) is a term that describes the portion of a trust’s income allotted to the beneficiaries. The calculation of DNI is performed to distribute the income of the trust between itself and its beneficiaries. It provides beneficiaries with a dependable income source.

The distributable net income is the income amount taxed to the beneficiaries, who can receive a maximum taxable amount equal to the DNI. The amount is capped to prevent double taxation on the money the trust generates. Any amount above the distributable net income will be tax-free, as it will include the principal.

Summary

- The amount of a trust’s income allotted to the beneficiaries is called the distributable net income (DNI).

- Any amount distributed to the beneficiaries or unitholders above the DNI is tax exempted.

- The distributable net income is calculated to determine the amount of deduction a trust can take on its income tax return.

How to Calculate the DNI

The formula for calculating the distributable net income is given below:

Distributable Net Income (DNI) = Taxable Income – Capital Gain (+ Capital Loss) + Tax Exemption

Where:

Taxable Income = Interest Income + Capital Gain (-Capital Loss) + Dividends – Tax Exemption – Fees

For example, a trust’s asset generated an income of $35,000, of which $22,000 was related to dividends, and $15,000 was the interest income. The trust’s asset realized $33,000 in capital gains, and the trustees charged $5,000 as administrative fees. The trust was allowed a tax exemption of $150.

The taxable income is calculated as:

Taxable income = $15,000 + $33,000 + $22,000 – $150 – $5,000 = $64,850

The taxable income calculated above can be used to compute the DNI as below:

DNI = $64,850 – $33,000 + $150 = $32,000

Significance of the DNI

The distributable net income is considered by the Internal Revenue Service (IRS) as an estimation of economic value acquired from distribution to the beneficiaries. The payment made to beneficiaries from a fund such as an income trust is called distribution. The distributable net income minimizes the tax amount that the trust needs to pay.

The non-grantor trusts and estates file income tax returns just as individuals do. In a non-grantor trust, the grantor who created and donated assets to the trust is not taxed. The control of the assets is given to the trust, and the trust functions independently from the grantor.

The reported income of the trusts is taxed either at the beneficiary or entity level. Depending on whether the levels are allocated to the principal amount or the distributable income and whether the beneficiaries have received the amount, the level to tax is determined.

The distributable net income is recognized by the income trust as an amount that is allocated to unitholders. In an estate trust, it is recognized as the amount to be allocated to beneficiaries. According to the U.S. tax code, trusts and estates are permitted to deduct the following from the income to avoid double taxation:

- Minimum of the distributable net income and aggregate trust income to be distributed to beneficiaries

- Any other amount properly credited or paid or needed to be distributed to the beneficiaries

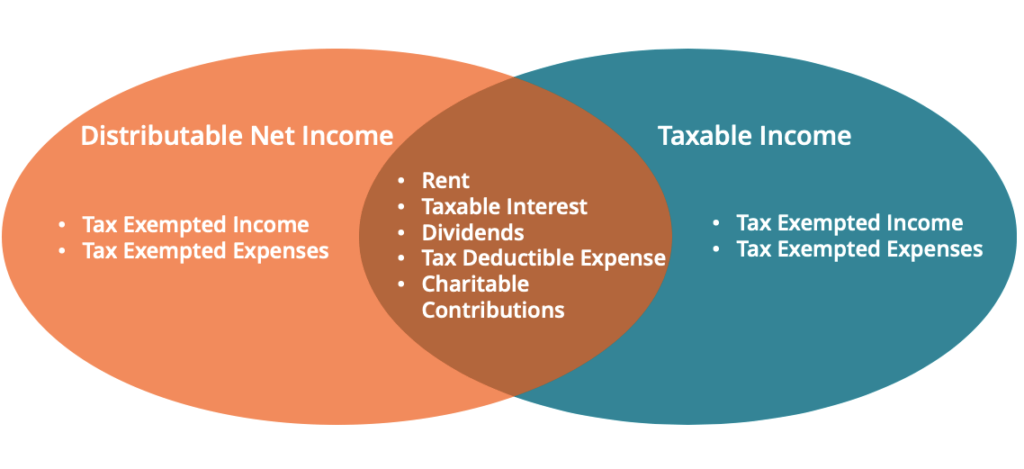

Distributable Net Income and Trust Accounting Income

While the distributable net income is the aggregate income that is taxed to the beneficiaries, the trust accounting income is the income available to pay only the trust income beneficiaries. The trust accounting income includes interests, ordinary income, and dividends. The capital gain and principal are usually distributed to the remaining beneficiaries. However, the trust accounting income can be redefined for including capital gain.

On the contrary, the DNI can include the capital gain to pass to the beneficiaries only if they are included as an accounting income or are required to be distributed. The distributable net income determines the deduction that the trust can take on the tax return. The trust deducts the DNI regardless of whether the amount is distributed to its beneficiaries or not.

Related Readings

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below:

Accounting Crash Courses

Learn accounting fundamentals and how to read financial statements with CFI’s online accounting classes.

These courses will give you the confidence to perform world-class financial analyst work. Start now!

Boost your confidence and master accounting skills effortlessly with CFI’s expert-led courses! Choose CFI for unparalleled industry expertise and hands-on learning that prepares you for real-world success.