Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

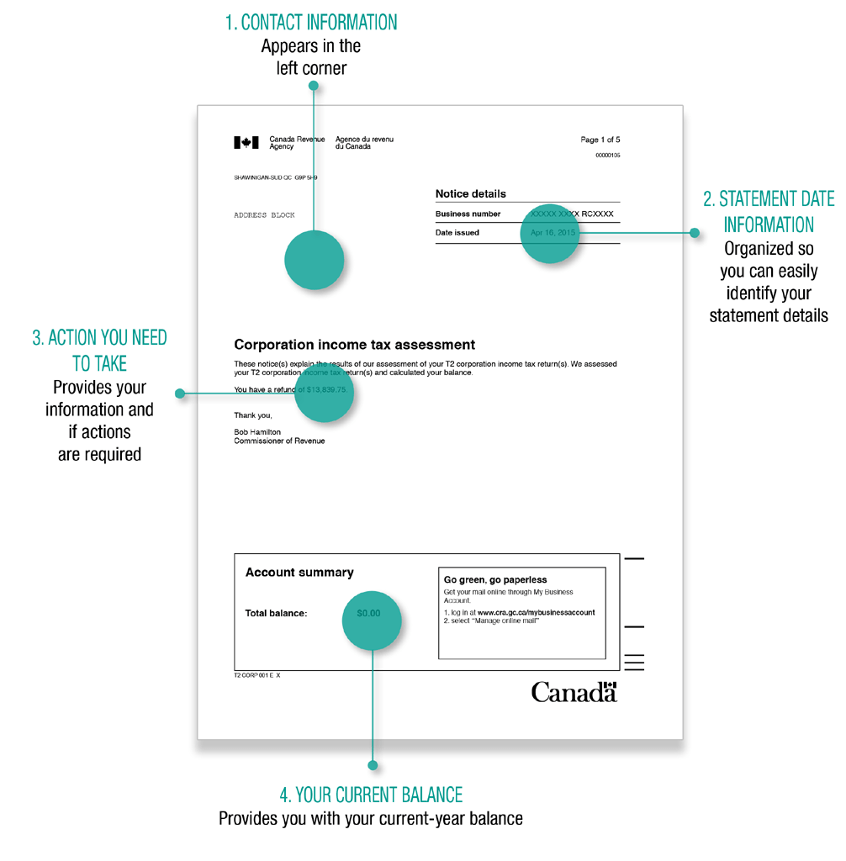

A statement issued by the Canada Revenue Agency (CRA) to Canadian taxpayers at the end of a tax year

A Notice of Assessment (NOA) is a statement issued by the Canada Revenue Agency (CRA) to Canadian taxpayers at the end of a tax year. The statement details the amount of income tax that the taxpayer owes the CRA, the amount of tax refund, tax credits, tax deductions, and income tax already paid.

The NOA also includes corrections to the income tax form, important updates for the following tax year, reminders about installment payments, and other issues relevant to a taxpayer’s tax report.

The Notice of Assessment is calculated based on the tax returns submitted by a taxpayer. It is a two-page document, and it indicates the name of the taxpayer, insurance number, the tax year, and the tax center.

If a taxpayer finds errors in the NOA, they are allowed to submit an adjustment request, highlighting the errors to be fixed. The Canada Revenue Agency allows up to 90 days from the date the NOA is issued to appeal the information if there is information they do not agree with.

For example, if a taxpayer expects to receive tax refunds of $8,000, but the NOA indicates that the taxpayer owes the CRA $3,000, a taxpayer can appeal the error within 90 days. When appealing, the taxpayer is required to attach any supporting documentation that explains their objection to the assessed income tax.

After submitting an appeal, the taxpayer is not required to pay the amount in dispute until the review is completed. Any appeals after the 90 days have elapsed are not considered, and the taxpayer information will be sent to collections.

One of the important items included in the Notice of Assessment is the Registered Retirement Savings Plan (RRSP). The section lists the RRSP contributions that a taxpayer made during the tax year, any unused contributions during the tax year, and the contribution limits for the following tax year. The CRA uses the information included in the tax returns for the relevant tax year to determine the maximum contributions that individuals can contribute towards their RRSP for the following year.

Taxpayers can claim the RRSP contributions as a deduction from the taxable income. The taxpayer is not required to claim the deductions during the tax year, and the deductions are carried forward to the following tax year if they expect to receive increased incomes. It allows them to claim a bigger deduction from the tax bill for the following year.

However, if a taxpayer accumulates unused contributions where previous contributions and the current year’s contributions exceed the RRSP deduction limit, a taxpayer may be penalized by the CRA. The taxpayer will be required to pay a penalty at the rate of 1% per month for the excess RRSP contribution amount.

After submitting tax returns for the year, a taxpayer can expect to receive the Notice of Assessment in two to eight weeks, depending on whether they submitted the tax return electronically or through paper-based returns. A taxpayer can receive the NOA in the following two ways:

If a person has not registered for online mail, the NOA is sent through regular mail.

Taxpayers can register to receive the NOA through online mail when filing tax returns electronically. The option is enabled under the CRA “My Account” service. Taxpayers can also check their return status and the NOA under the “My Account” tab. If the NOA is available, you can download the statement as a PDF.

The Canada Revenue Agency may conduct an audit of the business or personal income of taxpayers, especially when the agency suspects that a taxpayer has under-reported the annual income or over-reported the annual expenses to reduce the tax liability.

The tax audit involves cross-examination of all revenues and expenses incurred during the tax year by the taxpayer, and sometimes the spouse. A tax audit may also be conducted randomly for a select number of taxpayers or members of a tax group.

Once an auditor has sent a request for a tax audit, a taxpayer is required to furnish the auditor with all the requested information, such as evidence of expenses incurred during the year, financial statements for the current and previous tax years, etc.

For tax purposes, taxpayers are required to maintain a record of the tax records and relevant documents for the past six years, including the current year. If the outcome of the audit reveals discrepancies in the incomes and expenses reported, the CRA may order a reassessment of the current and previous years’ income taxes.

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: