Get Certified for

Commercial Banking (CBCA®)

Stand out and gain a competitive edge as a commercial banker, loan officer, or credit analyst with advanced knowledge, real-world analysis skills, and career confidence.

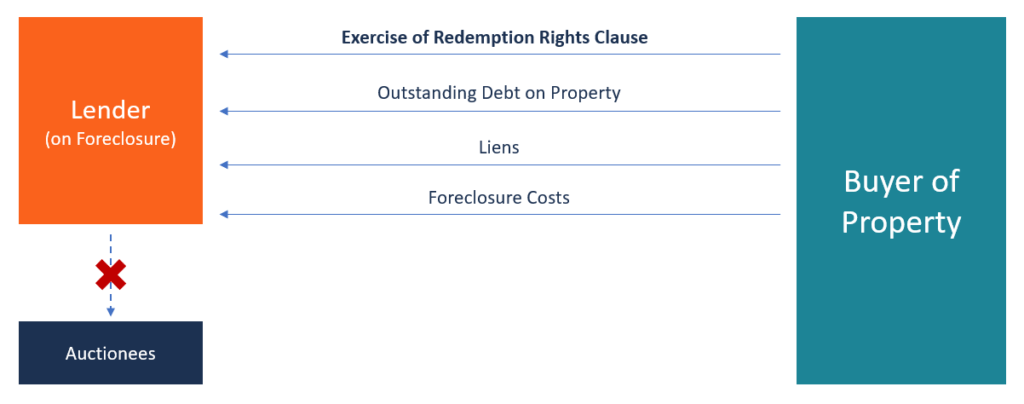

The redemption rights clause gives the owner of a property the right to reclaim his/her property during a foreclosure auction. The clause is often included in a mortgage agreement. Redemption rights allow the borrower to prevent foreclosure on the property by paying all liens or back taxes on the property. The amount paid by the borrower includes the costs of foreclosure and the entire amount of the outstanding mortgage, even after the auction.

The redemption rights clause can also be included in a motor vehicle purchase agreement. It allows the owner of the vehicle to reclaim the asset after repossession by paying the full amount of the remaining debt, repossession costs, and other related costs. Redemption rights can also apply when purchasing shares of a company. The provision gives the shareholders the right to force the company to repurchase the shares they (shareholders) own.

Most states in the United States have a statutory redemption provision to allow borrowers to reclaim their property. The right of redemption can be exercised before foreclosure or after the property has been foreclosed upon and offered for sale.

The borrower can exercise the right if they are able to source the money to repay the amount of debt owed to the state or a creditor. When exercising a statutory right of redemption, payment rules may vary since buyers may be required to pay a price that is below the fair market value of the property rather than the outstanding amount of debt.

Usually, most borrowers tend to take action after the property has been foreclosed upon. This is because borrowers who have enough money to pay the whole amount of outstanding debt can pay off the pending debt and other legal costs before the foreclosure occurs. Waiting until the foreclosure has occurred will mean paying higher fees than they would have paid before they were considered debt defaulters.

Some buyers may wait to exercise their redemption rights until a foreclosure sale in order to make a profit. For example, the foreclosed property may be put up for auction at a price that is below the market value. The buyer can pay the foreclosure sale price plus additional fees and then sell the property at an above-market value price and earn a profit in the process.

The right of redemption can be exercised by the owners of the foreclosed property. They can reclaim the property by paying a specified amount to the lender, depending on the rules included in the redemption rights clause. The homeowner can exercise the right before or after the foreclosure auction, as long as it is within the allowed redemption period. The two main types of redemption rights include:

The equitable right of redemption is available in all states, and homeowners are free to exercise the right. They can exercise the right to prevent a foreclosure upon their property by paying off the outstanding balance, plus other fees incurred during the foreclosure process. Most homeowners may find it difficult to source all the funds required to reclaim their property, and they may choose to sell the home to a third party or refinance the mortgage debt to retain the property.

The statutory right of redemption is available in a selected number of states in the United States and only residents of such states can exercise the right. It allows homeowners to reclaim ownership of their foreclosed property by paying the foreclosure price, interest, and other fees incurred in the foreclosure process.

If the buyer is unable to raise enough funds to pay the full foreclosure sale price during the allowed duration, the rights of redemption will expire and the property will be taken over by a third party. Where the foreclosure sale price of the property is below the fair market price, the homeowner can redeem the property at the foreclosure sale price. They can later sell it to a buyer at the fair market value and keep the difference as profits.

The redemption period may vary from weeks, months, or a year before or after the sale of the foreclosed property at an auction. The redemption period is usually set by the state. The homeowner should be aware of the allowed redemption period in order to reclaim their property. If the redemption period ends before or at the sale, the homeowner is at a higher risk in trying to reclaim ownership of the property if they can’t raise enough capital during the redemption period.

Depending on the state, the redemption period may last for several months up to a year after the auction. The homeowner can take advantage of it to source funds to pay the foreclosure sale price and all associated costs. Even if the property is sold before the redemption period expires, the homeowner still has an opportunity to reclaim the property. However, if they can’t raise enough funds to reclaim ownership of the property, they can sell the redemption rights to the buyer at a price that they can both agree on.

CFI is the official provider of the global Commercial Banking & Credit Analyst (CBCA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional CFI resources below will be useful: