Get Certified for Financial Modeling (FMVA)®

Gain in-demand industry knowledge and hands-on practice that will help you stand out from the competition and become a world-class financial analyst.

The part of one’s contribution that is withheld and paid at a future date

Deferred compensation refers to that part of one’s contribution that is withheld and paid at a future date. Retirement plans and employee pensions are examples of deferred compensation. Employers usually withhold a fraction of employees’ compensation every month, accumulate it over time, and pay the lump sum amount on a date previously agreed upon in the employment contract.

Since the compensation is paid at a later date, the amount deferred for payment is not included while computing tax. Therefore, it reduces the amount of taxable income in the current year. However, the requisite amount of tax is deducted at the time the employee receives this payment.

In some cases, employers invest the amount of deferred income into stock options or mutual funds. It increases the value of the payment due to the addition of interest payments and the possibility of capital gains.

Deferred compensations can be broadly classified into Qualified Deferred Compensation and Non-Qualified Deferred Compensation.

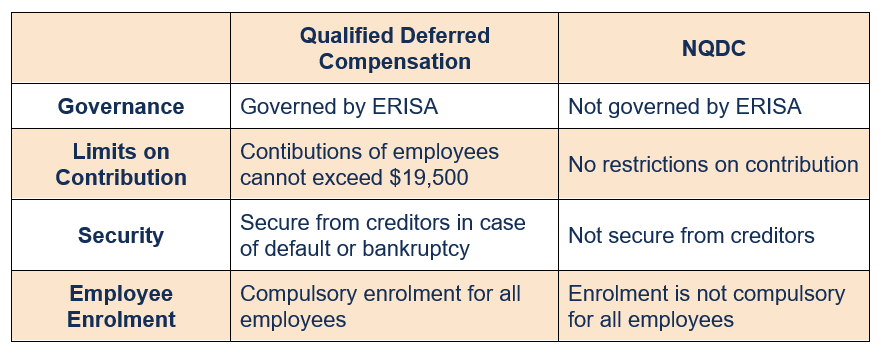

The Employee Retirement Income Security Act (ERISA), which was introduced to ensure protection to retirement assets, sets the rules for qualified deferred compensation. Under such rules, employees have a right to full information about their retirement plans free of cost. The law requires employee retirement assets to be held in a trust account.

The plans must be offered to all employees, and they are for the sole benefit of an employee. It means that creditors cannot claim the funds in case the company fails to pay its debts. Some examples of qualified deferred compensation include 401(k) and 403(b) plans.

ERISA also restricts the amount of money that can be deposited into a qualified plan. For example, the 401(k) plan limits the contribution of employees into the pension account at $19,500.

In general, qualified deferred compensation plans are governed by stricter rules, since the ERISA also specifies the minimum criteria that an employee must fulfill to qualify for the plan and includes extensive rules on how employers should provide sufficient funding for it.

Non-qualified deferred compensation plans (NQDC) evolved in response to the restrictions imposed on qualified deferred compensation plans by ERISA. The most distinguishing factor is that NQDCs have no maximum cap on the amount of employees’ contribution to their retirement savings account.

NQDCs are offered by companies to employees who earn high levels of income and wish to defer a greater portion of their income. The plans allow people to avoid taxes on a greater proportion of their earnings and enjoy higher tax-deferred investment returns.

Such plans are riskier compared to qualified deferred compensation plans since they are not protected under the rules of ERISA. NQDCs are not secured accounts, and the funds deposited in the plans can be taken over by the company’s creditors in case of default or bankruptcy.

The major points of difference between qualified deferred compensation and NQDC are as follows:

Deferred compensation plans offer the following benefits to beneficiaries:

Deferred compensation plans provide a stable income to people after they retire. The money received through retirement plans provides financial stability. Beneficiaries can also invest their money in mutual funds or other investment options later so that they can earn interest income.

The portion of one’s income deferred for payment on a future date reduces current income and is not taxed until the beneficiary receives the payment. Individuals who expect to come under a lower income tax bracket in the future greatly benefit from the scheme. Moreover, in case future tax rates fall in the country, beneficiaries of deferred compensation plans will eventually pay less in taxes.

Many employers invest the funds deposited in deferred compensation accounts in mutual funds or other safe investment options that offer steady interest payments. Regular interest payments add to the value of the post-retirement payment. Moreover, if the value of the investment rises over time, the beneficiary stands to make capital gains as well.

CFI offers the Financial Modeling & Valuation Analyst (FMVA®) certification program for those looking to take their careers to the next level. To keep learning and developing your knowledge base, please explore the additional relevant resources below: