Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

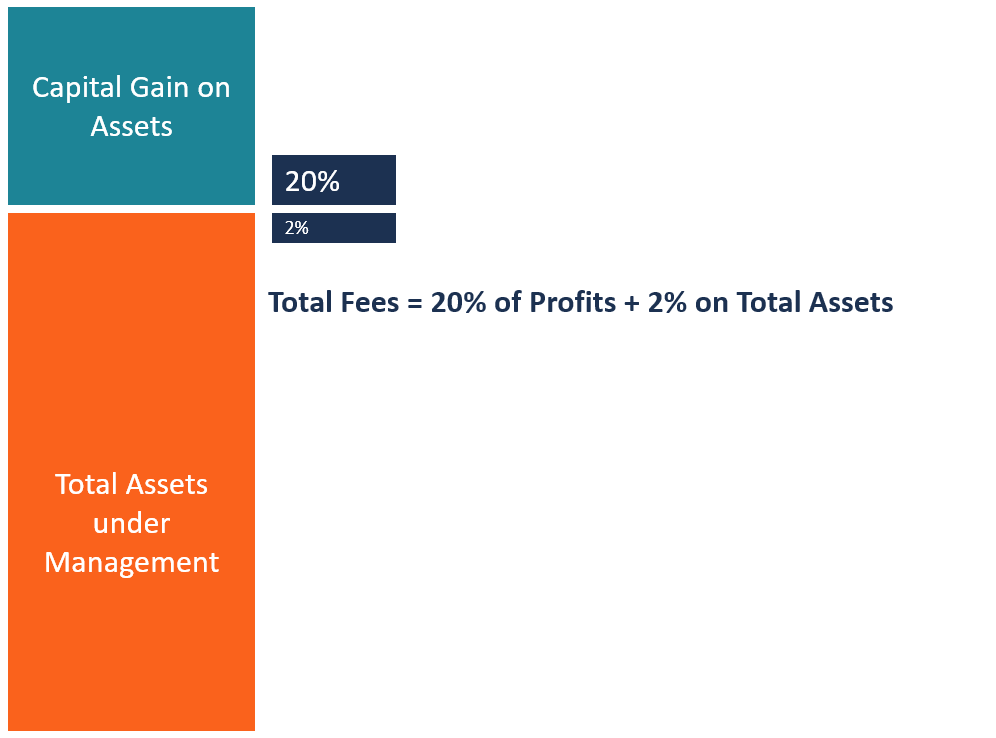

2% management fee + 20% performance fee

The 2 and 20 is a hedge fund compensation structure consisting of a management fee and a performance fee. 2% represents a management fee which is applied to the total assets under management. A 20% performance fee is charged on the profits that the hedge fund generates, beyond a specified minimum threshold.

Again, the 2% fee is charged on the assets under management regardless of the performance of the investments under the fund manager. However, the 20% fee is only charged when the fund achieves a certain level of profit.

The graphic below should make the compensation structure clear.

The 2 and 20 fee structure helps hedge funds finance their operations. The 2% flat rate charged on total assets under management (AUM) is used to pay staff salaries, administrative and office expenses, and other operational expenses. The 20% performance fee is used to reward the hedge fund’s key executives and portfolio managers. This bonus structure is what makes hedge fund managers some of the highest paid financial professionals.

The 20% performance fee is the biggest source of income for hedge funds. The performance fee is only charged when the fund’s profits exceed a prior agreed-upon level. A common threshold level used is 8%. That means that the hedge fund only charges the 20% performance fee if profits for the year surpass the 8% level.

For example, assume a fund with an 8% threshold level generates a return of 15% for the year. Then the 20% performance fee will be charged on the incremental 7% profit above the 8% threshold. If the hedge fund manages assets of 10 large investors and makes a sizeable profit, its income for the year may run into millions – sometimes billions – of dollars.

Some investors consider the common 2 and 20 hedge fund fee structure excessively high. Nonetheless, the industry has generally maintained this compensation structure over the years. It is able to do so primarily because hedge funds have consistently been able to generate high returns for their investors. Therefore, clients have been willing to put up with the fees, even if they consider them somewhat exorbitant, in order to obtain very favorable returns on investment. (ROI)

Renaissance Technologies, a hedge fund managed by Jim Simmons, maintained an average annual return of 71.8% between 1994 and 2015. Its worst year during the period still showed a 21% profit. Because of the high yields delivered to investors, they were willing to pay performance fees up to 44%.

Both investors and politicians have put hedge funds under pressure for their 2 and 20 compensation structure in recent years. This is largely due to the fact that, in the wake of the 2008 financial crisis, hedge funds – like many other investments – have struggled to perform at optimally high levels. As a result, an increasing number of investors have sought out hedge funds that charge fees lower than the traditional 2 and 20.

Politicians have sought a larger cut of hedge fund profits, seeking to have them taxed as ordinary income rather than at the lower capital gains rate. As of 2018, the hedge fund industry has been able to maintain the lower tax rate, arguing that their income is not a fixed salary and is based on performance.

Some of the alternative fee structures adopted by some hedge funds are as follows:

Startup and emerging hedge funds offer incentives to interested investors during the early stages of their business. These incentives are known as “founders shares”. The founders shares entitle investors to a lower fee structure, such as “1.5 and 10” rather than “2 and 20”. Another option is to use the 2 and 20 fee structure but with a promise to reduce the fee when the fund reaches a specific milestone. For example, the fund might charge 2 and 20 on profits up to 20%, but only charge “2 and 15” on profits beyond the 20% level.

A hedge fund may decide to offer a substantial discount to investors who are willing to lock up their investments with the company for a specified time period, such as five, seven, or 10 years. This practice is most common with hedge funds whose investments typically require longer time frames to generate a significant ROI. In exchange for the longer lockup period, clients benefit from a reduced fee structure.

Most hedge funds include a watermark clause that states that a hedge fund manager can only charge performance fees after the fund has generated new profits. If the fund incurs losses, it must recover the losses before charging performance fees.

Thank you for reading CFI’s guide on 2 and 20 (Hedge Fund Fees). To keep learning and advancing your career, the additional CFI resources below will be useful: