Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A pricing model used to determine the fair prices of stock options based on six variables

The Black-Scholes-Merton (BSM) model is a pricing model for financial instruments. It is used for the valuation of stock options. The BSM model is used to determine the fair prices of stock options based on six variables: volatility, type, underlying stock price, strike price, time, and risk-free rate. It is based on the principle of hedging and focuses on eliminating risks associated with the volatility of underlying assets and stock options.

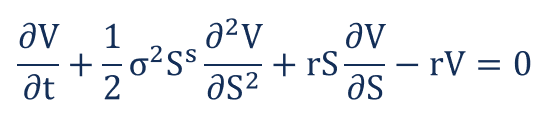

The Black-Scholes-Merton model can be described as a second order partial differential equation.

The equation describes the price of stock options over time.

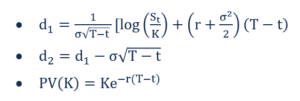

The price of a call option C is given by the following formula:

Where:

The price of a put option P is given by the following formula:

Where:

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

Thank you for reading CFI’s guide on the Black-Scholes-Merton Model. To keep learning and advancing your career, the following resources will be helpful: