Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A methodology that determines the number of days that interest accrues between coupon payment days

A day-count convention is a methodology that determines the number of days that interest accrues between coupon payment days. It is used in a variety of debt securities such as bonds, mortgages, swaps, and forward rate agreements (FRAs).

For interest-earning investments, if transactions are not made on the coupon payment dates, the accrued interest should be taken into consideration. A day-count convention can be used to calculate an accrual factor by specifying how to count the days of an entire coupon period and the days of an accrual period.

A day-count convention comprises two components. The first component determines the number of days in a month. It gives the instruction to count the days in an accrual period, which is the numerator of an accrual factor.

The second component defines the , which determines the denominator of an accrual factor by counting the days in a year or a full coupon period.

A day-count convention is presented in the form of “number of days in the accrual period/number of days in the year.” For example, if a bond has a 30/360 basis, it means that the number of accrued days is counted on the basis of 360 days per year and 30 days per month.

The day-count convention varies for different types of securities, depending on the issuers, country of issuance, whether the interest rate is fixed or floating, and other factors.

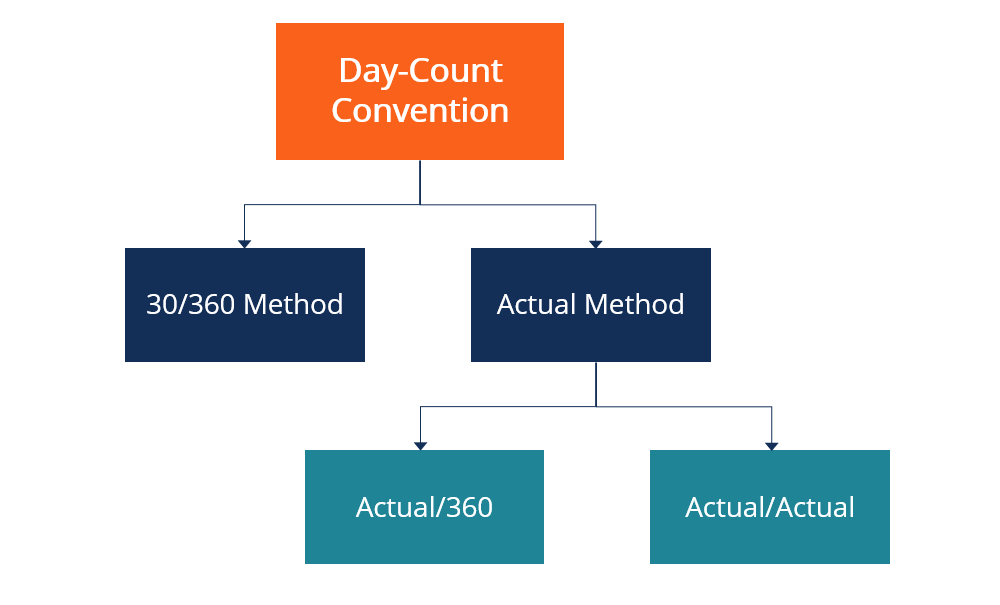

There are two major types of day-count conventions – the actual method and the 30/360 method.

In the actual method, the actual number of days should be counted in the accrual period or the coupon period.

The Actual/Actual method uses the actual number of days in each month and year, which requires the accrual period to be counted day-by-day from the effective date to the terminating date, and the coupon period should be counted from one specific coupon date to the next. Typically, U.S. Treasury bonds use the Actual/Actual method.

In the Actual/360 method, the actual number of days from the effective date to the terminating date is used for the accrual period, but the number of days in the year is assumed to be 360. This method is commonly used by money-market instruments.

The Actual/365 and Actual/365L are some of the less common examples of the actual method. The Actual/365 basis divides the actual number of accrual days by 365. The Actual/365L considers leap years, giving a year basis of 366 for leap years and 365 for non-leap years.

Different from the Actual/Actual method, there is no need to count the actual days under the 30/360 method. The 30/360 basis determines the denominator of an accrual factor (days in the year) as 360, which is composed of 12 30-day months.

If the start day or end day of an accrual period falls on the 31st of a month, the date will be moved to the 30th of that month. Corporate bonds usually have a 30/360 basis.

Other examples of the 30/360 method include the 30E/360, 30E+/360, and so on. Under the 30E/360 basis, if the end day of an accrual period falls in February, the actual number of days in February will be counted instead of extending the month to 30 days.

Under the 30E+/360 basis, if the first day of the accrual period falls on the 31st, it will still be moved to the 30th, but if the last day falls on the 31st, it will be moved to the 1st of the next month.

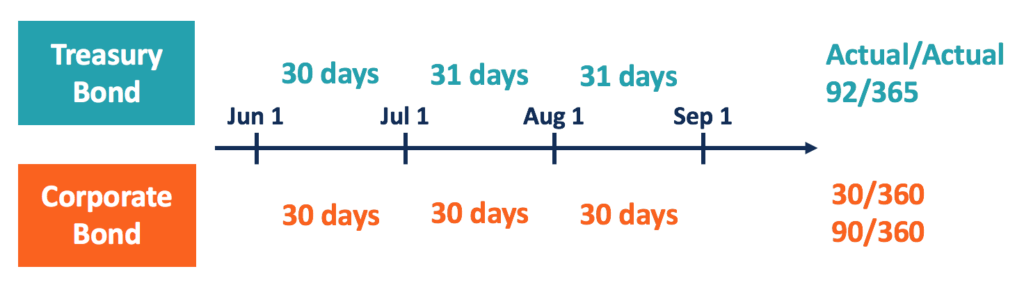

Assuming a Treasury bond and a corporate bond both have the same annual coupon payment dates, their last coupon payment date is September 1, 2018, and the next coupon date is September 1, 2019.

The question is to find the accrual factors for the period from June 1, 2019 to September 1, 2019, for the two bonds, respectively.

Treasury bonds usually have an Actual/Actual basis, and corporate bonds have a 30/360 basis. Under the 30/360 basis, there are 90 days in the three-month accrual period, so the accrual factor for the corporate bond is 0.25 (90/360).

The actual number of days in the accrual period and the entire year should be counted under the Actual/Actual basis. June has 30 days and both July and August have 31 days, so the accrual period contains 92 days. As 2019 is not a leap year and has 365 days, the accrual factor for the Treasury bond is thus 0.252 (92/365).

To keep learning and developing your knowledge base, please explore the additional relevant resources below: