Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

A requirement in a callable bond where the issuer does not have the ability to exercise the call before the specified date in the agreement

Hard call protection, also known as absolute call protection, is a requirement in a callable bond where the issuer does not have the ability to exercise the call before the specified date in the agreement. A callable bond is a type of bond where the issuer is allowed to redeem the bond before the maturity date.

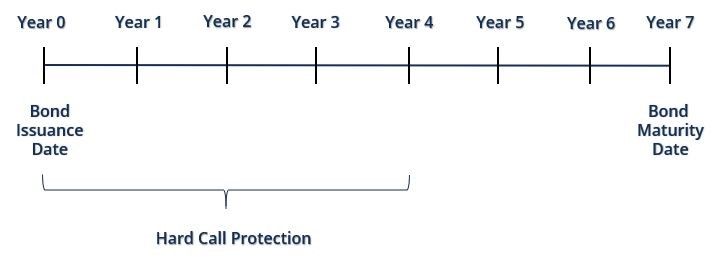

The issuer is not allowed to exercise the call for several years – usually between three to five years from the issuance date of the bond. For example, suppose a seven-year bond is callable after four years. Hard call protection refers to the four years the bond has before the issuer can exercise the bond any time before its maturity date.

Investors who purchase bonds get paid with the bond’s interest over the duration of the bond’s life until it matures. Since bond prices and interest rates have an inverse relationship, investors prefer to invest in bonds with higher interest rates and lower bond prices.

On the other hand, bond issuers prefer to sell bonds with lower interest rates and higher bond prices. Therefore, if interest rates decline, the issuer will want to redeem the bond before the maturity date, which affects the investor because they will no longer receive the relatively high interest payments if the bond is retired early. This is when having hard call protection can safeguard the investor from losing interest payments because the issuer will not be allowed to exercise the bond early.

As a result, there are limits on how and when a bond can be exercised, which reduces the risk of the bond for the investor and prevents the issuer from repaying the bonds earlier than the specified date. It offers a guarantee for the investor to receive the bond’s interest payments before the bond is free to be called by the issuer.

When valuing a bond, both the yield-to-maturity and yield-to-call figures are considered. However, a callable bond with hard call protection usually has a lower yield-to-call compared to its yield-to-maturity.

As a result, callable bonds with hard call protection are valued using the yield-to-call method in order to understand the bond’s return and investment potential.

After the time period for protecting a bond’s hard call has passed, there may also be soft call protection to continue to reduce the bond’s risk. If a bond has soft call protection, it will occur after the protection period when the hard call is over.

Soft call protection is a requirement that specifies how the bond issuer must pay a premium to the bond’s investor if the issuer wants to redeem the bond before maturity. A premium is a price that is higher than the bond’s current face value.

An example of a provision for soft call protection may require the bond issuer to pay a 4% premium if they want to redeem the bond one year after the hard call protection is over, a 3% premium if they want to redeem the bond two years after the hard call protection is over, and a 2% premium if they want to redeem the bond three years after the hard call protection is over.

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA)® certification program, designed to transform anyone into a world-class financial analyst.

To keep learning and developing your knowledge of financial analysis, we highly recommend the additional resources below: