Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

An American economist and creator of the influential Modern Portfolio Theory (MPT)

Harry Markowitz is an American economist and creator of the influential Modern Portfolio Theory (MPT) still widely used today.

Harry Markowitz was born in Chicago, Illinois, on August 24, 1927. After completing his bachelor’s in philosophy at the University of Chicago, Markowitz returned to the university for a master’s in economics, studying under influential economists such as Milton Friedman.

While writing his dissertation on the application of mathematics to stock market analysis, Markowitz took great interest in John Burr Williams’ “Theory of Investment Value.” Williams emphasized investors’ consideration of the expected value of assets within the portfolio, but Markowitz realized the argument lacked considerations of risk.

Markowitz identified the risk as variance – the measurement of volatility from the mean. Furthermore, he determined that investors could benefit from diversifying their portfolio due to idiosyncratic risk. Idiosyncratic risk is the risk inherent in specific assets. By incorporating different assets into a portfolio, diversification removes such a risk if the assets show low covariance (correlation of movement between assets).

Using risk and return as the primary considerations of investors, Markowitz pioneered the modern portfolio theory (MPT), published in 1952 by the Journal of Finance. He continued his work with colleague George Dantzig, where he refined his research on optimal portfolio allocation. His resulting work on graphing the Modern Portfolio Theory (MPT) would later be named the efficient frontier. He went on to receive a Ph.D. in economics and published his new findings on portfolio allocation.

His work earned him the John von Neumann Theory Prize in 1989 and the Nobel Memorial Prize in Economic Sciences in 1990. Almost a decade after Markowitz’s initial publication on MPT, the famous capital asset pricing model (CAPM) was introduced, based on Markowitz’s theory of risk and diversification.

Currently, Harry Markowitz spends his time teaching at the University of California San Diego and consulting at Harry Markowitz Company.

The Modern Portfolio Theory (also known as mean-variance analysis) is a portfolio allocation theory based on two factors – risk and return. The theory states that a portfolio’s risk can be reduced through diversification. Diversification works by holding many different assets with low or negative covariance. The low/negative covariance reduces the volatility (risk) of the portfolio by eliminating the idiosyncratic risk inherent in individual securities. The MPT takes an aggregate view in that each asset is less important than its impact on the portfolio as a whole.

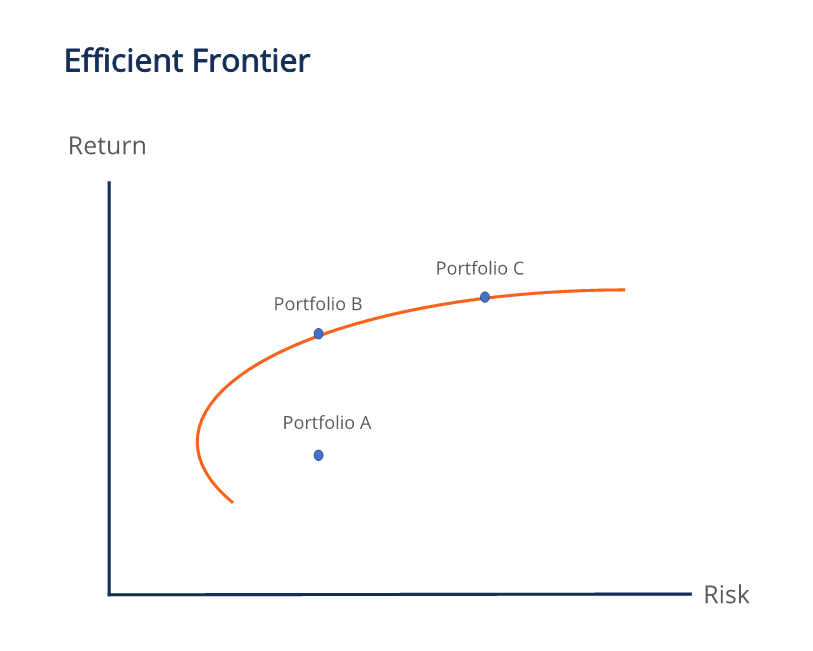

The theory assumes that investors are risk-averse, meaning that between two portfolios with the same risk, investors prefer the one with a higher return. Because individual investors have different risk tolerances, Markowitz developed the efficient frontier, where each point along the curve represents the optimal asset weightings in a portfolio that gives the highest expected return for the amount of risk. The graph depicts expected return as a function of risk.

Portfolios towards the right are weighted heavier on risky assets such as stocks and private equity. Portfolios towards the left are weighted heavier on less risky assets such as bonds. The upward slope of the efficient frontier demonstrates the concept that higher risk comes with a higher return.

Any portfolios on the efficient frontier are better than those under it. In the illustration above, portfolio B is objectively better than portfolio A because it has a higher expected return than portfolio A for the same risk. Such portfolios on the efficient frontier are called the Markowitz efficient set.

The best portfolio allocation on the efficient frontier depends on the level of risk tolerance of the investor. Both portfolio B and portfolio C have the highest return for their given risk. Therefore, we cannot say one is better than the other; investors with higher risk tolerance will like C better, while more conservative investors will like B better.

Connect what you just learned to a clear career path with CFI’s role‑based courses and certification programs.

CFI is the official provider of the Capital Markets & Securities Analyst (CMSA)® certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful: