Get Certified for

Capital Markets (CMSA®)

From equities and fixed income to derivatives, the CMSA certification bridges the gap from where you are now to where you want to be — a world-class capital markets analyst.

"The returns of bonds with different maturities should be the same over the short-term investment horizon"

In finance and economics, the Local Expectations Theory is a theory that suggests that the returns of bonds with different maturities should be the same over the short-term investment horizon. Essentially, the local expectations theory is one of the variations of the pure expectations theory, which assumes that the entire term structure of a bond reflects the expectations of the market regarding future short-term rates.

If an investor purchases two identical bonds where one bond comes with five years to maturity while another bond comes with 10 years to maturity, the local expectations theory implies that over the short-term investment period (e.g., six months), both bonds will deliver equivalent returns to the investor.

The rationale behind the theory is that the returns of bonds are primarily based on market expectations about forward rates. It also suggests that bonds with longer maturities do not compensate investors for interest rate risk or reinvestment rate risk.

Unlike other variations of the pure expectations theory, the local expectations theory addresses the restrictive holding period (short-term investment horizon) in which the returns of the bonds are expected to be equal.

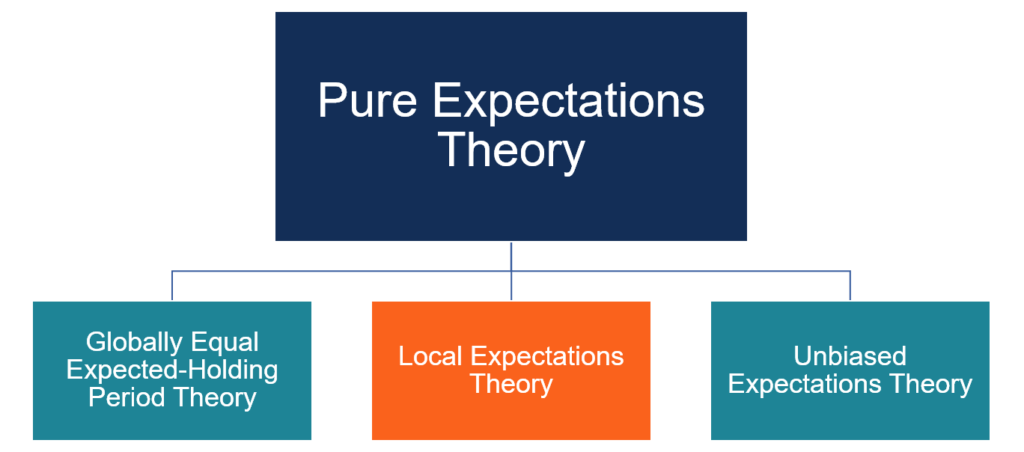

As mentioned above, the local expectations theory is a variation of the pure expectations theory. The pure expectations theory asserts that future short-term interest rates can be predicted using current long-term interest rates.

In addition to the local expectations theory, the pure expectations theory comes with several other variations. The most common variations of the theory include the following:

The first variation of the pure expectations theory assumes that the returns on bonds for a given holding period must be identical despite the time to maturity of the bonds.

For example, if an investor purchases one bond with the time to maturity of five years and another bond with the time to maturity of 10 years, the globally equal expected-holding period return theory suggests that for a certain holding period (no matter if the holding period is six months or three years), the returns on both bonds must be the same.

The local expectations theory is very similar to the globally equal expected-holding period return theory mentioned above. However, the main difference between the two is that the local expectations theory is restricted only to the short-term investment horizon.

In other words, if an investor buys one bond with a time to maturity of five years and another bond with a time to maturity of 10 years, the local expectations theory asserts that the returns on the bonds should be identical only during the short-term (e.g., six months).

The unbiased expectations theory is the most commonly encountered variation of the pure expectations theory. The unbiased expectations theory assumes that current long-term interest rates can be used to predict future short-term interest rates.

Instead of purchasing one two-year bond, an investor may buy a one-year bond now and another one-year bond later. According to the unbiased expectations theory, the returns should be identical in either case.

Although the pure expectations theory and its variations provide a simple and intuitive way to understand the term structure of interest rates, the theories do not usually hold in the real world. In reality, the current long-term interest rates also reflect the compensation for various risks such as interest rate risk.

Ultimately, the pure expectations theory requires the presence of perfectly efficient markets. The Preferred Habitat Theory provides a better option to understand the term structure of interest rates in the real world.

Thank you for reading CFI’s explanation of the local expectations theory. CFI is the official provider of the global Capital Markets & Securities Analyst (CMSA®) certification program, designed to help anyone become a world-class financial analyst. To keep advancing your career, the additional resources below will be useful: