Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment to become a successful financial planner or wealth advisor.

Occurs when employees own stock in the company and there is a difference between the average cost basis and the current market value of the shares owned

Net unrealized appreciation (NUA) occurs when employees own stock in the company where they are employed, and there is a difference between the average cost basis and the current market value of the shares owned.

Several companies give employees stock ownership in the company as a form of compensation or incentive.

When employees retire or exit a company, they can deal with the company stock they’ve accumulated over time from the employer in two ways:

The first way is to roll the assets over to an IRA (individual retirement account), which is a tax-advantaged tool for those who want to set aside funds for retirement.

The second way is called the net unrealized appreciation method, which allows employees to distribute the stock in a taxable account under distinct tax policies, leading to significant tax savings relative to the first approach.

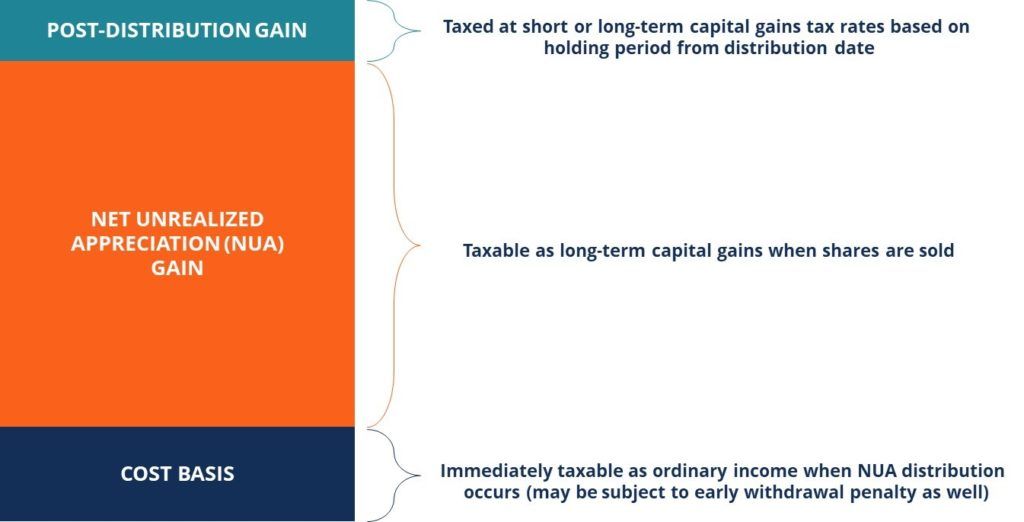

The employees pay income tax on the cost basis of the stock they own and pay a lower capital gains tax on the remaining distribution (only when the stock is sold, and gains are realized).

If the shares are held after the distribution, subsequent gains will be taxed at the short or long-term capital gains tax rate, based on the period from the distribution date to the date of sale.

In such a scenario, if a loss occurs, the amount of net unrealized appreciation gain will be reduced by the corresponding amount.

The age of the investor is an important aspect to consider regarding the effectiveness of the tax treatment of NUA. The older a person is, the shorter their retirement time horizon, and therefore, the NUA is more beneficial.

For a younger person, there is a lot of time for the assets to roll over to an IRA and grow on a deferred tax basis. This may result in the lower capital gains tax rate benefit being offset by the growth in your account.

The figure below illustrates the taxation treatment for different components of an NUA stock. There is a possibility that NUA gains may be deferred for a significant period of time, as there is no requirement that the NUA stock is to be sold immediately.

According to the Internal Revenue Code (IRC), a stock needs to meet three criteria in order for the above mentioned NUA tax treatment to hold:

For the above condition to hold, the stock owned by the employee must be transferred directly to a taxable investment account. They are not allowed to sell shares and transfer the cash or use stock options or repurchases, and the NUA tax treatment will not hold for the options.

Under such a condition, the complete account balance of the retirement plan must be distributed over a single tax year. No amount can stay in the plan after the distribution.

For the above two conditions to hold, the distribution must be made after a triggering event.

A triggering event can be characterized by death, disability, ending of service, or reaching retirement age. Therefore, a stock will not qualify for NUA treatment if a person is working, and a triggering event has not occurred.

A person owns $500,000 worth of company stock. We assume that they fall in the 20% marginal tax rate bracket. They assign a cost basis of $50,000 to the stock.

Suppose the person uses the NUA strategy and distributes their cost basis out to their non-retirement account. They will need to pay a 20% tax on the cost basis of $50,000 ($10,000). When the person sells the stock, they pay capital gains tax amounting to $25,000. Therefore, their total taxes are equal to $35,000.

Let’s consider the same example without using the NUA strategy. When the person withdraws the amount invested in the stock, they pay the income tax on the entire value of the stock and not only the cost basis.

Therefore, they will pay a 20% tax on $500,000 ($100,000). It is their total taxes for the year. We can see that using the NUA strategy, the person was able to save $65,000 in taxes on an annual basis.

CFI offers the Commercial Banking & Credit Analyst (CBCA)™ certification program for those looking to take their careers to the next level. To keep learning and advancing your career, the following resources will be helpful: