Get Certified for

Financial Planning & Wealth Management Professional (FPWMP®)

Learn financial analysis & planning, portfolio management, and risk assessment.

The sale or other disposition of stock shares that receive a favorable tax treatment for the individual disposing of the stock

Qualifying disposition is a tax term used in the U.S. that refers to a sale or other disposition of shares that receive favorable tax treatment for the individual disposal of the stock.

Qualifying dispositions are important for stockholders because there may be a wide disparity between the stockholder’s regular income tax rate and the significantly lower long-term capital gains tax rate. Therefore, qualifying dispositions can save stockholders a substantial amount of money in relation to taxes owed.

The qualifying disposition tax rules most commonly apply to stock that individuals acquire by virtue of being employed by the company issuing the stock. They may acquire stock shares through an employee stock purchase plan (known as an ESPP) or incentive stock option plans (referred to as ISOs).

ISOs are typically stock purchase options offered to employees who occupy an upper-level executive management position, such as the Chief Executive Officer (CEO), Chief Financial Officer (CFO), or Sales Manager.

Assume that you acquire 100 shares of your company’s stock through an ESPP that enables you to buy shares at a 10% discount to their current market price of $20 per share, so you only need to pay $18 per share for the stock. Your total purchase price for 100 shares is $1,800.

Further, assume that you can sell your stock shares for a price of $35 a share a few years later. Your total proceeds from the sale of your shares are $3,500. $3,500 minus your $1,800 purchase price gives you a tidy gross profit of $1,700.

Here is how the tax treatment of your stock profits would look if the sale of your shares is a qualifying disposition:

In contrast, if the sale of your stock shares was not a qualifying disposition, then you would be taxed at the 35% income tax rate on the whole profit realized from your stock – $1700. It would make your tax liability on your stock profits $595 ($1,700 multiplied by 35%) – nearly twice as much as your tax liability with a qualifying disposition.

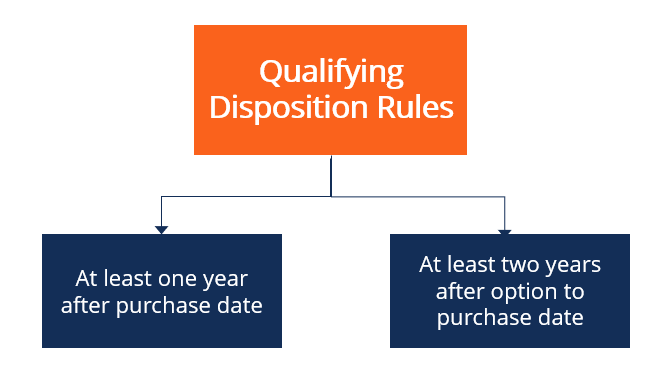

Since it can obviously make a big difference for you in terms of your tax liability, it is important to know the rules that govern whether the sale of your stock shares meets the requirements for being a qualifying disposition. Two basic rules that determine qualifying dispositions:

Thus, your company may have originally granted you the option to purchase shares at the 10% discount in May 2004, but you did not actually purchase your shares under the terms of the offer until June 2005).

The above conditions must be met for the sale of your stock shares to be deemed a qualifying disposition.

To keep learning and advancing your career, the following resources will be helpful: